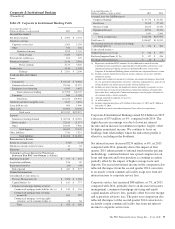

PNC Bank 2015 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

management judgment to assess how mortgage rates and

prepayment speeds could affect the future values of MSRs.

Hedging results can frequently be less predictable in the short

term, but over longer periods of time are expected to protect

the economic value of the MSRs.

The following sections of this Report provide further

information on residential and commercial MSRs:

• Note 7 Fair Value included in the Notes To

Consolidated Financial Statements in Item 8 of this

Report.

• Note 8 Goodwill and Intangible Assets included in

the Notes To Consolidated Financial Statements in

Item 8 of this Report.

Income Taxes

In the normal course of business, we and our subsidiaries enter

into transactions for which the tax treatment is unclear or

subject to varying interpretations. In addition, filing

requirements, methods of filing and the calculation of taxable

income in various state and local jurisdictions are subject to

differing interpretations.

We evaluate and assess the relative risks and merits of the tax

treatment of transactions, filing positions, filing methods and

taxable income calculations after considering statutes,

regulations, judicial precedent, and other information, and

maintain tax accruals consistent with our evaluation of these

relative risks and merits. The result of our evaluation and

assessment is by its nature an estimate. We and our subsidiaries

are routinely subject to audit and challenges from taxing

authorities. In the event we resolve a challenge for an amount

different than amounts previously accrued, we will account for

the difference in the period in which we resolve the matter.

Recently Issued Accounting Standards

In May 2014, the Financial Accounting Standard Board

(FASB) issued ASU 2014-09, Revenue from Contracts with

Customers (Topic 606). This ASU clarifies the principles for

recognizing revenue and replaces nearly all existing revenue

recognition guidance in U.S. GAAP with one accounting

model. The core principle of the guidance is that an entity

should recognize revenue to depict the satisfaction of a

performance obligation by transfer of promised goods or

services to customers. The ASU also requires additional

qualitative and quantitative disclosures relating to the nature,

amount, timing, and uncertainty of revenue and cash flows

arising from contracts with customers. In August 2015, the

FASB issued guidance deferring the mandatory effective date

of the ASU for one year, to annual reporting periods

beginning after December 15, 2017. The requirements within

ASU 2014-09 should be applied retrospectively to each prior

period presented (with several practical expedients for certain

completed contracts) or retrospectively with the cumulative

effect of initially applying ASU 2014-09 recognized at the

date of initial application. We plan to adopt the ASU

consistent with the deferred mandatory effective date. Based

on our evaluation to date, we do not expect the adoption of

this standard to have a significant impact on our consolidated

results of operations or our consolidated financial position.

Additionally, we will continue to evaluate this standard’s

impact as standard-setting, regulatory views and

interpretations evolve.

In February 2015, the FASB issued ASU 2015-02,

Consolidation (Topic 810): Amendments to the Consolidation

Analysis. All legal entities are subject to re-evaluation under

this ASU, including investment companies and certain other

entities measured in a manner consistent with ASC 946

Financial Services – Investment Companies which were

previously excluded. The ASU will change the analysis that a

reporting entity must perform to determine whether it should

consolidate certain types of legal entities. Specifically, the

ASU modifies the evaluation of whether limited partnerships

and similar legal entities are variable interest entities (VIEs)

or voting interest entities; eliminates the presumption that a

general partner should consolidate a limited partnership;

potentially changes the consolidation conclusions of reporting

entities that are involved with VIEs, in particular those that

have fee arrangements and related party arrangements, and

provides a scope exception for reporting entities with interests

held in certain money market funds. The ASU is effective for

public business entities for annual periods, and interim periods

within those annual periods, beginning after December 15,

2015 and may be applied through a retrospective or modified

retrospective approach. We adopted this standard as of

January 1, 2016 under a modified retrospective approach. The

impact of adoption did not have a significant impact on our

consolidated results of operations or our consolidated financial

position.

In January 2016, the FASB issued ASU 2016-01, Financial

Instruments – Overall (Subtopic 825-10): Recognition and

Measurement of Financial Assets and Financial Liabilities.

This ASU changes the accounting for certain equity

investments, financial liabilities under the fair value option

and presentation and disclosure requirements for financial

instruments. Equity investments not accounted for under the

equity method of accounting will be measured at fair value

with any changes in fair value recognized in net income.

Equity investments without readily determinable fair values

may be measured at cost, adjusted for impairment and other

changes resulting from observable price changes in orderly

transactions for a similar investment of the same issuer. A

qualitative assessment may be utilized to evaluate equity

investments without readily determinable fair values for

impairment. If impairment exists, the investment is required to

be measured at fair value. In addition to the changes for

certain equity investments, the ASU also 1) requires that

instrument-specific credit risk changes in the fair value of a

financial liability accounted for under the fair value option be

The PNC Financial Services Group, Inc. – Form 10-K 65