PNC Bank 2015 Annual Report Download - page 214

Download and view the complete annual report

Please find page 214 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

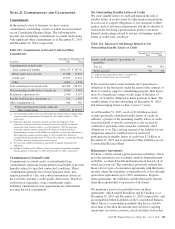

varying based on the type of assets serving as collateral. In

certain circumstances, federal regulatory authorities may

impose more restrictive limitations.

Federal Reserve Board regulations require depository

institutions to maintain cash reserves with a Federal Reserve

Bank (FRB). At December 31, 2015, the balance outstanding

at the FRB was $30.0 billion.

N

OTE

20 L

EGAL

P

ROCEEDINGS

We establish accruals for legal proceedings, including

litigation and regulatory and governmental investigations and

inquiries, when information related to the loss contingencies

represented by those matters indicates both that a loss is

probable and that the amount of loss can be reasonably

estimated. Any such accruals are adjusted thereafter as

appropriate to reflect changed circumstances. When we are

able to do so, we also determine estimates of possible losses

or ranges of possible losses, whether in excess of any related

accrued liability or where there is no accrued liability, for

disclosed legal proceedings (“Disclosed Matters,” which are

those matters disclosed in this Note 20). For Disclosed

Matters where we are able to estimate such possible losses or

ranges of possible losses, as of December 31, 2015, we

estimate that it is reasonably possible that we could incur

losses in excess of related accrued liabilities, if any, in an

aggregate amount of up to approximately $550 million. The

estimates included in this amount are based on our analysis of

currently available information and are subject to significant

judgment and a variety of assumptions and uncertainties. As

new information is obtained we may change our estimates.

Due to the inherent subjectivity of the assessments and

unpredictability of outcomes of legal proceedings, any

amounts accrued or included in this aggregate amount may not

represent the ultimate loss to us from the legal proceedings in

question. Thus, our exposure and ultimate losses may be

higher, and possibly significantly so, than the amounts

accrued or this aggregate amount.

In our experience, legal proceedings are inherently

unpredictable. One or more of the following factors frequently

contribute to this inherent unpredictability: the proceeding is

in its early stages; the damages sought are unspecified,

unsupported or uncertain; it is unclear whether a case brought

as a class action will be allowed to proceed on that basis or, if

permitted to proceed as a class action, how the class will be

defined; the other party is seeking relief other than or in

addition to compensatory damages (including, in the case of

regulatory and governmental investigations and inquiries, the

possibility of fines and penalties); the matter presents

meaningful legal uncertainties, including novel issues of law;

we have not engaged in meaningful settlement discussions;

discovery has not started or is not complete; there are

significant facts in dispute; the possible outcomes may not be

amenable to the use of statistical or quantitative analytical

tools; predicting possible outcomes depends on making

assumptions about future decisions of courts or regulatory

bodies or the behavior of other parties; and there are a large

number of parties named as defendants (including where it is

uncertain how damages or liability, if any, will be shared

among multiple defendants). Generally, the less progress that

has been made in the proceedings or the broader the range of

potential results, the harder it is for us to estimate losses or

ranges of losses that it is reasonably possible we could incur.

As a result of these types of factors, we are unable, at this

time, to estimate the losses that are reasonably possible to be

incurred or ranges of such losses with respect to some of the

matters disclosed, and the aggregate estimated amount

provided above does not include an estimate for every

Disclosed Matter. Therefore, as the estimated aggregate

amount disclosed above does not include all of the Disclosed

Matters, the amount disclosed above does not represent our

maximum reasonably possible loss exposure for all of the

Disclosed Matters. The estimated aggregate amount also does

not reflect any of our exposure to matters not so disclosed, as

discussed below under “Other.”

We include in some of the descriptions of individual

Disclosed Matters certain quantitative information related to

the plaintiff’s claim against us as alleged in the plaintiff’s

pleadings or other public filings or otherwise publicly

available information. While information of this type may

provide insight into the potential magnitude of a matter, it

does not necessarily represent our estimate of reasonably

possible loss or our judgment as to any currently appropriate

accrual.

Some of our exposure in Disclosed Matters may be offset by

applicable insurance coverage. We do not consider the

possible availability of insurance coverage in determining the

amounts of any accruals (although we record the amount of

related insurance recoveries that are deemed probable up to

the amount of the accrual) or in determining any estimates of

possible losses or ranges of possible losses.

Interchange Litigation

Beginning in June 2005, a series of antitrust lawsuits were

filed against Visa®, MasterCard®, and several major financial

institutions, including cases naming National City (since

merged into PNC) and its subsidiary, National City Bank of

Kentucky (since merged into National City Bank which in

turn was merged into PNC Bank, N.A.). The cases have been

consolidated for pretrial proceedings in the U.S. District Court

for the Eastern District of New York under the caption In re

Payment Card Interchange Fee and Merchant-Discount

Antitrust Litigation (Master File No. 1:05-md-1720-JG-JO).

Those cases naming National City were brought as class

actions on behalf of all persons or business entities who have

accepted Visa®or MasterCard®. The plaintiffs, merchants

operating commercial businesses throughout the U.S. and

trade associations, allege, among other things, that the

196 The PNC Financial Services Group, Inc. – Form 10-K