PNC Bank 2015 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

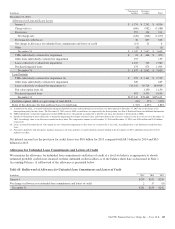

During 2015, $82 million of provision recapture was recorded

for purchased impaired loans compared to $91 million of

provision recapture during 2014. Charge-offs (which were

specifically for commercial loans greater than a defined

threshold) during 2015 were $12 million compared to $42

million during 2014. At December 31, 2015 and December 31,

2014, the ALLL on total purchased impaired loans was $.3

billion and $.9 billion, respectively. The decline in ALLL was

primarily due to the change in our derecognition policy. For

purchased impaired loan pools where an allowance has been

recognized, subsequent increases in the net present value of

cash flows will result in a provision recapture of any

previously recorded ALLL to the extent applicable, and/or a

reclassification from non-accretable difference to accretable

yield, which will be recognized prospectively. Individual loan

transactions where final dispositions have occurred (as noted

above) result in removal of the loans from their applicable

pools for cash flow estimation purposes. The cash flow re-

estimation process is completed quarterly to evaluate the

appropriateness of the ALLL associated with the purchased

impaired loans.

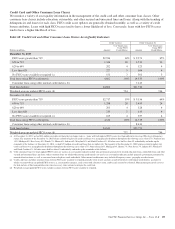

Activity for the accretable yield during 2015 and 2014

follows:

Table 66: Purchased Impaired Loans – Accretable Yield

In millions 2015 2014

January 1 $1,558 $2,055

Accretion (including excess cash recoveries) (466) (587)

Net reclassifications to accretable from non-

accretable 226 208

Disposals (68) (118)

December 31 $1,250 $1,558

N

OTE

5A

LLOWANCES FOR

L

OAN AND

L

EASE

L

OSSES AND

U

NFUNDED

L

OAN

C

OMMITMENTS

AND

L

ETTERS OF

C

REDIT

Allowance for Loan and Lease Losses

We maintain the ALLL at levels that we believe to be

appropriate to absorb estimated probable credit losses incurred

in the portfolios as of the balance sheet date. We use the two

main portfolio segments – Commercial Lending and

Consumer Lending – and develop and document the ALLL

under separate methodologies for each of these segments as

discussed in Note 1 Accounting Policies. A rollforward of the

ALLL and associated loan data follows.

The PNC Financial Services Group, Inc. – Form 10-K 141