PNC Bank 2015 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

The Basel II framework, which was adopted by the Basel

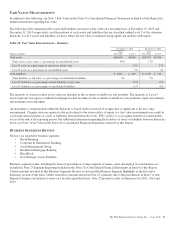

Committee on Banking Supervision in 2004, seeks to provide

more risk-sensitive regulatory capital calculations and

promote enhanced risk management practices among large,

internationally active banking organizations. The U.S. banking

agencies initially adopted rules to implement the Basel II

capital framework in 2004. In July 2013, the U.S. banking

agencies adopted final rules (referred to as the advanced

approaches) that modified the Basel II framework effective

January 1, 2014. See the Supervision and Regulation section

in Item 1 Business and Item 1A Risk Factors of this Report for

additional information. Prior to fully implementing the

advanced approaches to calculate risk-weighted assets, PNC

and PNC Bank must successfully complete a “parallel run”

qualification phase. Both PNC and PNC Bank entered this

parallel run phase on January 1, 2013. Although the minimum

parallel run qualification period is four quarters, the parallel

run period for PNC and PNC Bank, now in its third year, is

consistent with the experience of other U.S. advanced

approaches banks that have all had multi-year parallel run

periods. After PNC exits parallel run, its regulatory risk-based

capital ratio for each measure (e.g., Common equity Tier 1

capital ratio) will be the lower of the ratios as calculated under

the standardized approach and the advanced approaches.

As a result of the staggered effective dates of the final U.S.

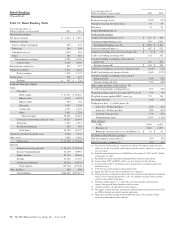

Basel III regulatory capital rules (Basel III rules), as well as

the fact that PNC remains in the parallel run qualification

phase for the advanced approaches, PNC’s regulatory risk-

based ratios in 2015 were calculated using the standardized

approach, effective January 1, 2015, for determining risk-

weighted assets, and the definitions of, and deductions from,

regulatory capital under the Basel III rules (as such definitions

and deductions are phased-in for 2015). We refer to the capital

ratios calculated using the phased-in Basel III provisions in

effect for 2015 and, for the risk-based ratios, standardized

approach risk-weighted assets as the 2015 Transitional Basel

III ratios. Under the standardized approach for determining

credit risk-weighted assets, exposures are generally assigned a

pre-defined risk weight. Exposures to high volatility

commercial real estate, past due exposures, equity exposures

and securitization exposures are generally subject to higher

risk weights than other types of exposures.

Under the Basel III rules adopted by the U.S. banking

agencies, significant common stock investments in

unconsolidated financial institutions, mortgage servicing

rights and deferred tax assets must be deducted from capital

(subject to a phase-in schedule) to the extent they individually

exceed 10%, or in the aggregate exceed 15%, of the

institution’s adjusted common equity Tier 1 capital. Also,

Basel III regulatory capital includes (subject to a phase-in

schedule) accumulated other comprehensive income related to

securities currently and previously held as available for sale,

as well as pension and other postretirement plans.

Federal banking regulators have stated that they expect the

largest U.S. bank holding companies, including PNC, to have

a level of regulatory capital well in excess of the regulatory

minimum and have required the largest U.S. bank holding

companies, including PNC, to have a capital buffer sufficient

to withstand losses and allow them to meet the credit needs of

their customers through estimated stress scenarios. We seek to

manage our capital consistent with these regulatory principles,

and believe that our December 31, 2015 capital levels were

aligned with them.

At December 31, 2015, PNC and PNC Bank, our sole bank

subsidiary, were both considered “well capitalized,” based on

applicable U.S. regulatory capital ratio requirements.

Beginning in 2015, to qualify as “well capitalized”, PNC must

have Transitional Basel III capital ratios of at least 6% for

Tier 1 risk-based capital and 10% for Total risk-based capital,

and PNC Bank must have Transitional Basel III capital ratios

of at least 6.5% for Common equity Tier 1 risk-based capital,

8% for Tier 1 risk-based capital, 10% for Total risk-based

capital, and a Leverage ratio of at least 5%. To qualify as

“well capitalized” in 2014, regulators required insured

depository institutions, such as PNC Bank, to maintain

Transitional Basel III capital ratios of at least 6% for Tier 1

risk-based, 10% for Total risk-based and 5% for Leverage,

and required bank holding companies, such as PNC, to

maintain Transitional Basel III regulatory capital ratios of at

least 6% Tier 1 risk-based and 10% for Total risk-based.

The access to and cost of funding for new business initiatives,

the ability to undertake new business initiatives including

acquisitions, the ability to engage in expanded business

activities, the ability to pay dividends or repurchase shares or

other capital instruments, the level of deposit insurance costs,

and the level and nature of regulatory oversight depend, in

large part, on a financial institution’s capital strength.

We provide additional information regarding regulatory

capital requirements and some of their potential impacts on

PNC in the Supervision and Regulation section of Item 1

Business, Item 1A Risk Factors and Note 19 Regulatory

Matters in the Notes To Consolidated Financial Statements in

Item 8 of this Report.

The PNC Financial Services Group, Inc. – Form 10-K 49