PNC Bank 2015 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

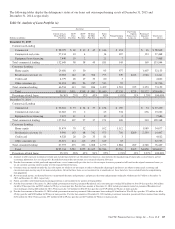

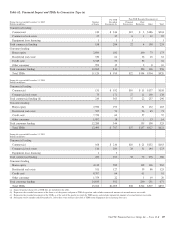

Table 56: Commercial Lending Asset Quality Indicators (a)(b)

Criticized Commercial Loans

In millions Pass Rated

Special

Mention (c) Substandard (d) Doubtful (e) Total Loans

December 31, 2015

Commercial $ 93,364 $2,029 $3,089 $ 90 $ 98,572

Commercial real estate 26,729 120 481 5 27,335

Equipment lease financing 7,230 87 150 1 7,468

Purchased impaired loans 6 157 6 169

Total commercial lending $127,323 $2,242 $3,877 $102 $133,544

December 31, 2014

Commercial $ 92,884 $1,984 $2,424 $ 55 $ 97,347

Commercial real estate 22,066 285 639 35 23,025

Equipment lease financing 7,518 73 93 2 7,686

Purchased impaired loans 4 280 26 310

Total commercial lending $122,468 $2,346 $3,436 $118 $128,368

(a) Based upon PDs and LGDs. We apply a split rating classification to certain loans meeting threshold criteria. By assigning a split classification, a loan’s exposure amount may be split

into more than one classification category in the above table.

(b) Loans are included above based on the Regulatory Classification definitions of “Pass”, “Special Mention”, “Substandard” and “Doubtful”.

(c) Special Mention rated loans have a potential weakness that deserves management’s close attention. If left uncorrected, these potential weaknesses may result in deterioration of

repayment prospects at some future date. These loans do not expose us to sufficient risk to warrant a more adverse classification at this time.

(d) Substandard rated loans have a well-defined weakness or weaknesses that jeopardize the collection or liquidation of debt. They are characterized by the distinct possibility that we will

sustain some loss if the deficiencies are not corrected.

(e) Doubtful rated loans possess all the inherent weaknesses of a Substandard loan with the additional characteristics that the weakness makes collection or liquidation in full improbable

due to existing facts, conditions, and values.

Consumer Lending Asset Classes

Home Equity and Residential Real Estate Loan Classes

We use several credit quality indicators, including

delinquency information, nonperforming loan information,

updated credit scores, originated and updated LTV ratios, and

geography, to monitor and manage credit risk within the home

equity and residential real estate loan classes. We evaluate

mortgage loan performance by source originators and loan

servicers. A summary of asset quality indicators follows:

Delinquency/Delinquency Rates: We monitor trending of

delinquency/delinquency rates for home equity and residential

real estate loans. See the Asset Quality section of this Note 3

for additional information.

Nonperforming Loans: We monitor trending of

nonperforming loans for home equity and residential real

estate loans. See the Asset Quality section of this Note 3 for

additional information.

Credit Scores: We use a national third-party provider to

update FICO credit scores for home equity loans and lines of

credit and residential real estate loans at least quarterly. The

updated scores are incorporated into a series of credit

management reports, which are utilized to monitor the risk in

the loan classes.

LTV (inclusive of combined loan-to-value (CLTV) for first

and subordinate lien positions): At least annually, we update

the property values of real estate collateral and calculate an

updated LTV ratio. For open-end credit lines secured by real

estate in regions experiencing significant declines in property

values, more frequent valuations may occur. We examine

LTV migration and stratify LTV into categories to monitor the

risk in the loan classes.

Historically, we used, and we continue to use, a combination

of original LTV and updated LTV for internal risk

management and reporting purposes (e.g., line management,

loss mitigation strategies). In addition to the fact that

estimated property values by their nature are estimates, given

certain data limitations it is important to note that updated

LTVs may be based upon management’s assumptions (e.g.,if

an updated LTV is not provided by the third-party service

provider, home price index (HPI) changes will be incorporated

in arriving at management’s estimate of updated LTV).

Geography: Geographic concentrations are monitored to

evaluate and manage exposures. Loan purchase programs are

sensitive to, and focused within, certain regions to manage

geographic exposures and associated risks.

A combination of updated FICO scores, originated and

updated LTV ratios and geographic location assigned to home

equity loans and lines of credit and residential real estate loans

is used to monitor the risk in the loan classes. Loans with

higher FICO scores and lower LTVs tend to have a lower

level of risk. Conversely, loans with lower FICO scores,

higher LTVs, and in certain geographic locations tend to have

a higher level of risk.

130 The PNC Financial Services Group, Inc. – Form 10-K