PNC Bank 2015 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

(continued from previous page)

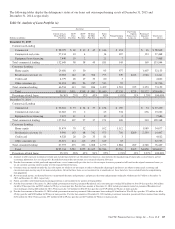

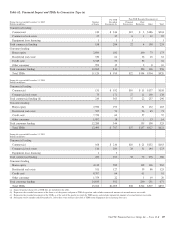

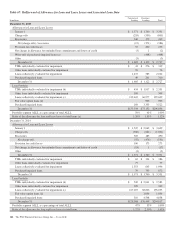

Home Equity Residential Real Estate

December 31, 2014 – in millions 1st Liens 2nd Liens Total

Current estimated LTV ratios (c)

Greater than or equal to 125% and updated FICO scores:

Greater than 660 $ 333 $ 1,399 $ 360 $ 2,092

Less than or equal to 660 (d) (e) 57 273 92 422

Missing FICO 1 9 8 18

Greater than or equal to 100% to less than 125% and updated FICO scores:

Greater than 660 839 2,190 772 3,801

Less than or equal to 660 (d) (e) 118 383 153 654

Missing FICO 1 5 12 18

Greater than or equal to 90% to less than 100% and updated FICO scores:

Greater than 660 891 1,703 755 3,349

Less than or equal to 660 103 271 118 492

Missing FICO 2 3 5 10

Less than 90% and updated FICO scores:

Greater than 660 13,878 7,874 7,703 29,455

Less than or equal to 660 1,319 995 573 2,887

Missing FICO 27 14 109 150

Total home equity and residential real estate loans $17,569 $15,119 $10,660 $43,348

(a) Excludes purchased impaired loans of approximately $3.4 billion and $4.5 billion in recorded investment, certain government insured or guaranteed residential real estate mortgages of

approximately $0.9 billion and $1.2 billion, and loans held for sale at December 31, 2015 and December 31, 2014, respectively. See the Home Equity and Residential Real Estate

Asset Quality Indicators – Purchased Impaired Loans table below for additional information on purchased impaired loans.

(b) Amounts shown represent recorded investment.

(c) Based upon updated LTV (inclusive of combined loan-to-value (CLTV) for first and subordinate lien positions). Updated LTV is estimated using modeled property values. These

ratios are updated at least semi-annually. The related estimates and inputs are based upon an approach that uses a combination of third-party automated valuation models (AVMs),

broker price opinions (BPOs), HPI indices, property location, internal and external balance information, origination data and management assumptions. We generally utilize

origination lien balances provided by a third-party, where applicable, which do not include an amortization assumption when calculating updated LTV. Accordingly, the results of

these calculations do not represent actual appraised loan level collateral or updated LTV based upon lien balances held by others, and as such, are necessarily imprecise and subject to

change as we enhance our methodology.

(d) Higher risk loans are defined as loans with both an updated FICO score of less than or equal to 660 and an updated LTV greater than or equal to 100%.

(e) The following states had the highest percentage of higher risk loans at December 31, 2015: New Jersey 14%, Pennsylvania 12%, Illinois 11%, Ohio 11%, Florida 7%, Maryland 7%

and Michigan 5%. The remainder of the states had lower than 4% of the higher risk loans individually, and collectively they represent approximately 33% of the higher risk loans. The

following states had the highest percentage of higher risk loans at December 31, 2014: New Jersey 14%, Pennsylvania 12%, Illinois 12%, Ohio 12%, Florida 8%, Maryland 6%,

Michigan 5%, and North Carolina 4%. The remainder of the states had lower than 4% of the high risk loans individually, and collectively they represent approximately 28% of the

higher risk loans.

132 The PNC Financial Services Group, Inc. – Form 10-K