PNC Bank 2015 Annual Report Download - page 213

Download and view the complete annual report

Please find page 213 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

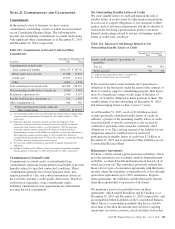

benefit of $46 million of gross interest and penalties,

decreasing income tax expense. The total accrued interest and

penalties at December 31, 2014 was $41 million. At

December 31, 2015, the total accrued interest and penalties

was not significant.

During 2015, we recognized $202 million of amortization,

$224 million of tax credits and $74 million of other tax

benefits associated with qualified investments in low income

housing tax credits within Income taxes.

N

OTE

19 R

EGULATORY

M

ATTERS

We are subject to the regulations of certain federal, state, and

foreign agencies and undergo periodic examinations by such

regulatory authorities.

The ability to undertake new business initiatives (including

acquisitions), the access to and cost of funding for new

business initiatives, the ability to pay dividends, the ability to

repurchase shares or other capital instruments, the level of

deposit insurance costs, and the level and nature of regulatory

oversight depend, in large part, on a financial institution’s

capital strength.

At December 31, 2015 and December 31, 2014, PNC and

PNC Bank, our domestic banking subsidiary, were both

considered “well capitalized,” based on applicable U.S.

regulatory capital ratio requirements. Beginning in 2015, to

qualify as “well capitalized”, PNC must have Transitional

Basel III capital ratios of at least 6% for Tier 1 risk-based

capital and 10% for Total risk-based capital, and PNC Bank

must have Transitional Basel III capital ratios of at least 6.5%

for Common equity Tier 1 risk-based capital, 8% for Tier 1

risk-based capital, 10% for Total risk-based capital, and a

Leverage ratio of at least 5%. To qualify as “well capitalized”

in 2014, regulators required insured depository institutions,

such as PNC Bank, to maintain Transitional Basel III capital

ratios of at least 6% for Tier 1 risk-based, 10% for Total risk-

based and 5% for Leverage, and required bank holding

companies, such as PNC, to maintain Transitional Basel III

regulatory capital ratios of at least 6% Tier 1 risk-based and

10% for Total risk-based.

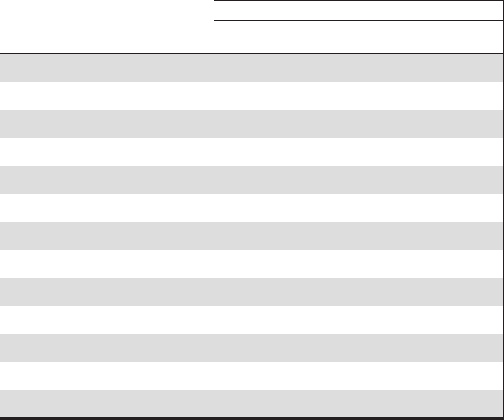

The following table sets forth the Transitional Basel III

regulatory capital ratios at December 31, 2015 and

December 31, 2014 for PNC and PNC Bank.

Table 130: Basel Regulatory Capital (a)

Amount Ratios

December 31

Dollars in millions 2015 2014 2015 2014

Risk-based capital

Common equity Tier 1 (b)

PNC $31,493 N/A 10.6% N/A

PNC Bank 27,484 N/A 9.7 N/A

Tier 1

PNC 35,522 $35,687 12.0 12.6%

PNC Bank 29,425 29,328 10.4 10.7

Total

PNC 43,260 44,782 14.6 15.8

PNC Bank 36,482 37,559 12.9 13.7

Leverage

PNC 35,522 35,687 10.1 10.8

PNC Bank 29,425 29,328 8.7 9.2

(a) Calculated using the Transitional Basel III regulatory capital methodology

applicable to PNC during both 2015 and 2014.

(b) For 2014, Common equity Tier 1 was not applicable to U.S. regulatory capital ratio

requirements for “well capitalized.”

The principal source of parent company cash flow is the

dividends it receives from its subsidiary bank, which may be

impacted by the following:

• Capital needs,

• Laws and regulations,

• Corporate policies,

• Contractual restrictions, and

• Other factors.

Also, there are statutory and regulatory limitations on the

ability of national banks to pay dividends or make other

capital distributions. The amount available for dividend

payments to the parent company by PNC Bank without prior

regulatory approval was approximately $1.7 billion at

December 31, 2015.

Under federal law, a bank subsidiary generally may not extend

credit to, or engage in other types of covered transactions

(including the purchase of assets) with, the parent company or

its non-bank subsidiaries on terms and under circumstances

that are not substantially the same as comparable transactions

with nonaffiliates. A bank subsidiary may not extend credit to,

or engage in a covered transaction with, the parent company

or a non-bank subsidiary if the aggregate amount of the bank’s

extensions of credit and other covered transactions with the

parent company or non-bank subsidiary exceeds 10% of the

capital stock and surplus of such bank subsidiary or the

aggregate amount of the bank’s extensions of credit and other

covered transactions with the parent company and all non-

bank subsidiaries exceeds 20% of the capital and surplus of

such bank subsidiary. Such extensions of credit, with limited

exceptions, must be at least fully collateralized in accordance

with specified collateralization thresholds, with the thresholds

The PNC Financial Services Group, Inc. – Form 10-K 195