PNC Bank 2015 Annual Report Download - page 185

Download and view the complete annual report

Please find page 185 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

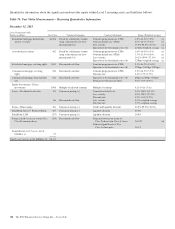

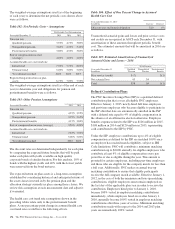

Changes in commercial MSRs during 2013, prior to the

irrevocable fair value election, follow:

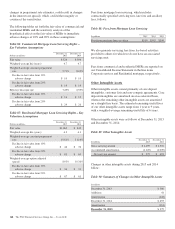

Table 84: Commercial Mortgage Servicing Rights Accounted

for Under the Amortization Method

In millions 2013

Commercial Mortgage Servicing Rights – Net Carrying

Amount

January 1 $ 420

Additions (a) 138

Amortization expense (97)

Change in valuation allowance 88

December 31 $ 549

Servicing advances at December 31 $ 412

Commercial Mortgage Servicing Rights – Valuation

Allowance

January 1 $(176)

Provision (21)

Recoveries 108

Other 1

December 31 $ (88)

(a) Additions for 2013 included $53 million from loans sold with servicing retained and

$85 million from purchases of servicing rights from third parties.

Residential Mortgage Servicing Rights

We recognize mortgage servicing right assets on residential

real estate loans when we retain the obligation to service these

loans upon sale and the servicing fee is more than adequate

compensation. Residential MSRs are subject to declines in

value from actual or expected prepayment of the underlying

loans and defaults as well as market driven changes in interest

rates. We manage this risk by economically hedging the fair

value of residential MSRs with securities and derivative

instruments which are expected to increase (or decrease) in

value when the value of residential MSRs declines (or

increases).

The fair value of residential MSRs is estimated by using a

discounted cash flow valuation model which calculates the

present value of estimated future net servicing cash flows,

taking into consideration actual and expected mortgage loan

prepayment rates, discount rates, servicing costs, and other

economic factors which are determined based on current

market conditions.

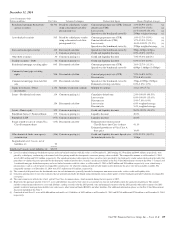

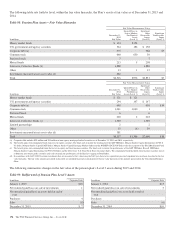

Changes in the residential MSRs follow:

Table 85: Residential Mortgage Servicing Rights

In millions 2015 2014 2013

January 1 $ 845 $ 1,087 $ 650

Additions:

From loans sold with

servicing retained 78 85 158

Purchases 316 45 110

Sales (4)

Changes in fair value due to:

Time and payoffs (a) (178) (134) (193)

Other (b) 2 (238) 366

December 31 $ 1,063 $ 845 $ 1,087

Unpaid principal balance of

loans serviced for others at

December 31 $123,466 $108,010 $113,994

Servicing advances at

December 31 $ 411 $ 501 $ 571

(a) Represents decrease in MSR value due to passage of time, including the impact from

both regularly scheduled loan principal payments and loans that were paid down or

paid off during the period.

(b) Represents MSR value changes resulting primarily from market-driven changes in

interest rates.

Sensitivity Analysis

The fair value of commercial and residential MSRs and

significant inputs to the valuation models as of December 31,

2015 are shown in the tables below. The expected and actual

rates of mortgage loan prepayments are significant factors

driving the fair value. Management uses both internal

proprietary models and a third-party model to estimate future

commercial mortgage loan prepayments and a third-party

model to estimate future residential mortgage loan

prepayments. These models have been refined based on

current market conditions and management judgment. Future

interest rates are another important factor in the valuation of

MSRs. Management utilizes market implied forward interest

rates to estimate the future direction of mortgage and discount

rates. The forward rates utilized are derived from the current

yield curve for U.S. dollar interest rate swaps and are

consistent with pricing of capital markets instruments.

Changes in the shape and slope of the forward curve in future

periods may result in volatility in the fair value estimate.

A sensitivity analysis of the hypothetical effect on the fair

value of MSRs to adverse changes in key assumptions is

presented below. These sensitivities do not include the impact

of the related hedging activities. Changes in fair value

generally cannot be extrapolated because the relationship of

the change in the assumption to the change in fair value may

not be linear. Also, the effect of a variation in a particular

assumption on the fair value of the MSRs is calculated

independently without changing any other assumption. In

reality, changes in one factor may result in changes in another

(for example, changes in mortgage interest rates, which drive

The PNC Financial Services Group, Inc. – Form 10-K 167