PNC Bank 2015 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

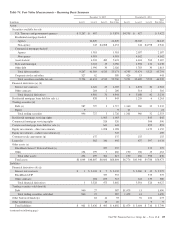

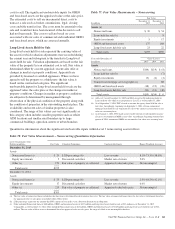

|

|

December 31, 2014

Level 3 Instruments Only

Dollars in millions Fair Value Valuation Techniques Unobservable Inputs Range (Weighted Average)

Residential mortgage-backed non-

agency securities

$4,798 Priced by a third-party vendor

using a discounted cash flow

Constant prepayment rate (CPR) Constant

default rate (CDR)

1.0%-28.9% (6.8%)

0.0%-16.7% (5.6%)

(a)

(a)

pricing model (a) Loss severity

Spread over the benchmark curve (b)

6.1%-100.0% (53.1%)

249bps weighted average

(a)

(a)

Asset-backed securities 563 Priced by a third-party vendor Constant prepayment rate (CPR) 1.0%-15.7% (5.9%) (a)

using a discounted cash flow Constant default rate (CDR) 1.7%-13.9% (7.6%) (a)

pricing model (a) Loss severity 14.6%-100.0% (73.5%) (a)

Spread over the benchmark curve (b) 352bps weighted average (a)

State and municipal securities 132 Discounted cash flow Spread over the benchmark curve (b) 55bps-165bps (67bps)

2 Consensus pricing (c) Credit and Liquidity discount 0.0%-20.0% (14.9%)

Other debt securities 30 Consensus pricing (c) Credit and Liquidity discount 7.0%-95.0% (88.6%)

Trading securities – Debt 32 Consensus pricing (c) Credit and Liquidity discount 0.0%-15.0% (8.0%)

Residential mortgage servicing rights 845 Discounted cash flow Constant prepayment rate (CPR) 3.8%-32.7% (11.2%)

Spread over the benchmark curve (b) 889bps-1,888bps (1,036bps)

Commercial mortgage servicing

rights 506 Discounted cash flow Constant prepayment rate (CPR) 7.0%-16.8% (8.0%)

Discount rate 2.5%-8.6% (6.6%)

Commercial mortgage loans held for

sale

893 Discounted cash flow Spread over the benchmark curve (b)

Estimated servicing cash flows

37bps-4,025bps (549bps)

0.0%-2.0% (1.2%)

Equity investments –Direct

investments

1,152 Multiple of adjusted earnings Multiple of earnings 3.2x-13.9x (7.7x)

Loans – Residential real estate 114 Consensus pricing (c) Cumulative default rate 2.0%-100.0% (90.5%)

Loss severity 0.0%-100.0% (35.6%)

Discount rate 5.4%-7.0% (6.4%)

154 Discounted cash flow Loss severity 8.0% weighted average

Discount rate 3.4% weighted average

Loans – Home equity 129 Consensus pricing (c) Credit and Liquidity discount 26.0%-99.0% (51.0%)

BlackRock Series C Preferred Stock 375 Consensus pricing (c) Liquidity discount 20.0%

BlackRock LTIP (375) Consensus pricing (c) Liquidity discount 20.0%

Swaps related to sales of certain Visa

Class B common shares

(135) Discounted cash flow Estimated conversion factor of

Class B shares into Class A shares

Estimated growth rate of Visa Class A

share price

41.1%

14.8%

Other borrowed funds –non-agency

securitization

(166) Consensus pricing (c) Credit and Liquidity discount Spread over

the benchmark curve (b)

0.0%-99.0% (18.0%)

113bps

Insignificant Level 3 assets, net of

liabilities (e) 23

Total Level 3 assets, net of liabilities (f) $9,072

(a) Level 3 residential mortgage-backed non-agency and asset-backed securities with fair values as of December 31, 2015 totaling $3,379 million and $448 million, respectively, were

priced by a third-party vendor using a discounted cash flow pricing model that incorporates consensus pricing, where available. The comparable amounts as of December 31, 2014

were $4,081 million and $532 million, respectively. The significant unobservable inputs for these securities were provided by the third-party vendor and are disclosed in the table. Our

procedures to validate the prices provided by the third-party vendor related to these securities are discussed further in the Fair Value Measurement section of this Note 7. Certain Level

3 residential mortgage-backed non-agency and asset-backed securities with fair values as of December 31, 2015 of $629 million and $34 million, respectively, were valued using a

pricing source, such as a dealer quote or comparable security price, for which the significant unobservable inputs used to determine the price were not reasonably available. The

comparable amounts as of December 31, 2014 were $717 million and $31 million, respectively.

(b) The assumed yield spread over the benchmark curve for each instrument is generally intended to incorporate non-interest-rate risks, such as credit and liquidity risks.

(c) Consensus pricing refers to fair value estimates that are generally internally developed using information such as dealer quotes or other third-party provided valuations or comparable

asset prices.

(d) This conversion factor reflects the 4-for-1 split of Visa Class A common shares, which occurred during the first quarter of 2015.

(e) Represents the aggregate amount of Level 3 assets and liabilities measured at fair value on a recurring basis that are individually and in the aggregate insignificant. The amount

includes certain financial derivative assets and liabilities, trading securities (for the 2015 period), state and municipal securities (for the 2015 period), other debt securities (for 2015

period), residential mortgage loans held for sale, other assets, other borrowed funds (ROAPs) and other liabilities. For additional information, please see the Fair Value Measurement

discussion included in this Note 7.

(f) Consisted of total Level 3 assets of $8,606 million and total Level 3 liabilities of $495 million as of December 31, 2015 and $9,788 million and $716 million as of December 31, 2014,

respectively.

The PNC Financial Services Group, Inc. – Form 10-K 159