PNC Bank 2015 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2015 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

|

|

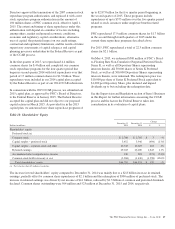

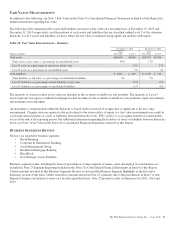

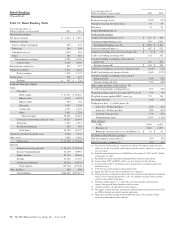

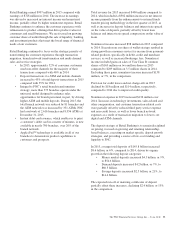

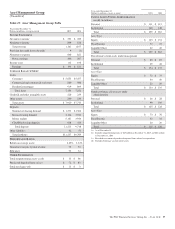

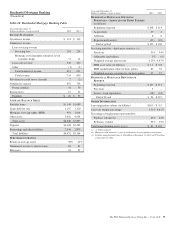

Retail Banking continued to focus on a relationship-based

lending strategy that targets specific products and markets for

growth. In 2015, average total loans declined $2.0 billion, or

3%, compared to 2014, driven by a decline in home equity

loans and declines from run-off of non-strategic portions of

the portfolios, as more fully described below.

• Average home equity loans decreased $1.2 billion, or

4%, as pay-downs and payoffs on loans exceeded

new booked volume, consistent with lower mortgage

demand. Retail Banking’s home equity loan portfolio

is relationship based, with over 97% of the portfolio

attributable to borrowers in our primary geographic

footprint.

• Average commercial & commercial real estate loans

declined $347 million, or 3%, as pay-downs and

payoffs on loans exceeded new volume.

• Average auto dealer floor plan loans declined $30

million, or 1%, primarily resulting from lower dealer

line utilization.

• Average indirect auto loans increased $245 million,

or 3%, primarily due to portfolio growth in

previously underpenetrated markets.

• Average credit card balances increased $163 million,

or 4%, as a result of efforts to increase credit card

share of wallet through organic growth.

• Average residential mortgage balances increased $79

million, or 13%, due to the transfer of $198 million in

CRA mortgage loans from the Residential Mortgage

Banking business segment in January 2015.

• In 2015, average loan balances for the remainder of

the portfolio declined $895 million, compared to

2014, driven by declines in the education and indirect

other portfolios of $901 million and $163 million,

respectively, as the discontinued government

guaranteed education loan and indirect other balances

are primarily run-off portfolios.

Nonperforming assets declined $153 million, or 13%, at

December 31, 2015 compared to December 31, 2014. The

decrease was driven by declines in both consumer and

commercial non-performing loans.

54 The PNC Financial Services Group, Inc. – Form 10-K