Wells Fargo 2014 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

Risk Management - Credit Risk Management (continued)

capacity at the time of modification are charged down to the fair

value of the collateral, if applicable. For an accruing loan that

has been modified, if the borrower has demonstrated

performance under the previous terms and the underwriting

process shows the capacity to continue to perform under the

restructured terms, the loan will generally remain in accruing

status. Otherwise, the loan will be placed in nonaccrual status

until the borrower demonstrates a sustained period of

performance, generally six consecutive months of payments, or

equivalent, inclusive of consecutive payments made prior to

modification. Loans will also be placed on nonaccrual, and a

corresponding charge-off is recorded to the loan balance, when

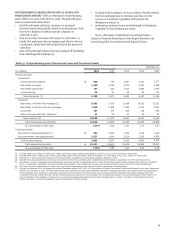

Table 37: Analysis of Changes in TDRs

we believe that principal and interest contractually due under

the modified agreement will not be collectible.

Table 37 provides an analysis of the changes in TDRs. Loans

that may be modified more than once are reported as TDR

inflows only in the period they are first modified. Other than

resolutions such as foreclosures, sales and transfers to held for

sale, we may remove loans held for investment from TDR

classification, but only if they have been refinanced or

restructured at market terms and qualify as a new loan.

Quarter ended

Dec 31, Sep 30, Jun 30, Mar 31, Year ended Dec. 31,

(in millions) 2014 2014 2014 2014 2014

Commercial TDRs

Balance, beginning of period $ 3,201 3,525 3,781 3,765 3,765 5,146

Inflows 232 208 276 442 1,158 1,794

Outflows

Charge-offs (62) (42) (28) (23) (155) (132)

Foreclosure (27) (12) (8) (3) (50) (88)

Payments, sales and other (1) (424) (478) (496) (400) (1,798) (2,955)

Balance, end of period 2,920 3,201 3,525 3,781 2,920 3,765

Consumer TDRs

Balance, beginning of period 21,841 22,082 22,698 22,696 22,696 21,768

Inflows 957 946 1,003 1,104 4,010 5,958

Outflows

Charge-offs (99) (120) (139) (157) (515) (859)

Foreclosure (252) (303) (283) (325) (1,163) (1,290)

Payments, sales and other (1) (797) (768) (1,073) (563) (3,201) (2,826)

Net change in trial modifications (2) (21) 4 (124) (57) (198) (55)

Balance, end of period 21,629 21,841 22,082 22,698 21,629 22,696

Total TDRs $ 24,549 25,042 25,607 26,479 24,549 26,461

(1) Other outflows include normal amortization/accretion of loan basis adjustments and loans transferred to held-for-sale. It also includes $1 million of loans refinanced or

restructured as new loans and removed from TDR classification for the quarter ended March 31, 2014. No loans were removed from TDR classification for the quarters

ended December 31, September 30, and June 30, 2014, respectively. During 2013, $84 million of loans were refinanced or restructured as new loans and removed from

TDR classification.

(2) Net change in trial modifications includes: inflows of new TDRs entering the trial payment period, net of outflows for modifications that either (i) successfully perform and

enter into a permanent modification, or (ii) did not successfully perform according to the terms of the trial period plan and are subsequently charged-off, foreclosed upon or

otherwise resolved. Our experience is that substantially all of the mortgages that enter a trial payment period program are successful in completing the program

requirements.

2013

78