Wells Fargo 2014 Annual Report Download - page 169

Download and view the complete annual report

Please find page 169 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

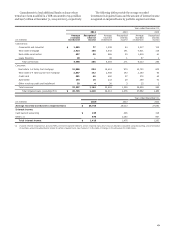

|

|

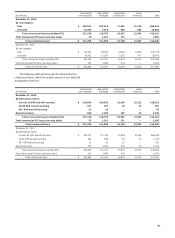

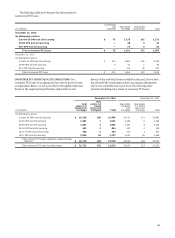

Real estate Real estate Other

1-4 family 1-4 family revolving

first junior lien credit and

(in millions) mortgage mortgage Credit card Automobile installment Total

December 31, 2014

By updated FICO:

< 600 $ 11,166 4,001 2,639 8,825 894 27,525

600-639 7,866 2,794 2,588 6,236 1,058 20,542

640-679 13,894 5,324 4,931 9,352 2,366 35,867

680-719 24,412 8,970 6,285 9,994 4,389 54,050

720-759 35,490 12,171 6,407 7,475 5,896 67,439

760-799 82,123 17,897 5,234 7,315 7,673 120,242

800+ 39,219 7,581 2,758 6,184 5,819 61,561

No FICO available 3,236 878 277 359 1,814 6,564

FICO not required — — — — 5,854 5,854

Government insured/guaranteed loans (1) 26,268 — — — — 26,268

Total consumer loans (excluding PCI) 243,674 59,616 31,119 55,740 35,763 425,912

Total consumer PCI loans (carrying value) 21,712 101 — — — 21,813

Total consumer loans $ 265,386 59,717 31,119 55,740 35,763 447,725

December 31, 2013

By updated FICO:

< 600 $ 14,128 5,047 2,404 8,400 956 30,935

600-639 9,029 3,247 2,175 5,925 1,015 21,391

640-679 14,918 5,985 4,176 8,827 2,158 36,064

680-719 24,336 10,043 5,398 8,992 3,917 52,686

720-759 32,991 13,581 5,530 6,546 5,264 63,912

760-799 72,062 19,238 4,535 6,313 6,836 108,984

800+ 33,310 7,707 2,409 5,397 5,130 53,953

No FICO available 2,896 979 255 408 2,054 6,592

FICO not required — — — — 5,007 5,007

Government insured/guaranteed loans (1) 30,737 — — — 10,712 41,449

Total consumer loans (excluding PCI) 234,407 65,827 26,882 50,808 43,049 420,973

Total consumer PCI loans (carrying value) 24,100 123 — — — 24,223

Total consumer loans $ 258,507 65,950 26,882 50,808 43,049 445,196

(1) Represents loans whose repayments are predominantly insured by the FHA or guaranteed by the VA and student loans whose repayments are predominantly guaranteed by

agencies on behalf of the U.S. Department of Education under FFELP.

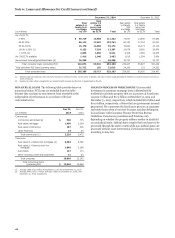

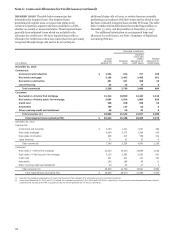

LTV refers to the ratio comparing the loan’s unpaid

principal balance to the property’s collateral value. CLTV refers

to the combination of first mortgage and junior lien mortgage

(including unused line amounts for credit line products) ratios.

LTVs and CLTVs are updated quarterly using a cascade approach

which first uses values provided by automated valuation models

(AVMs) for the property. If an AVM is not available, then the

value is estimated using the original appraised value adjusted by

the change in Home Price Index (HPI) for the property location.

If an HPI is not available, the original appraised value is used.

The HPI value is normally the only method considered for high

value properties, generally with an original value of $1 million or

more, as the AVM values have proven less accurate for these

properties.

The following table shows the most updated LTV and CLTV

distribution of the real estate 1-4 family first and junior lien

mortgage loan portfolios. We consider the trends in residential

real estate markets as we monitor credit risk and establish our

allowance for credit losses. In the event of a default, any loss

should be limited to the portion of the loan amount in excess of

the net realizable value of the underlying real estate collateral

value. Certain loans do not have an LTV or CLTV primarily due

to industry data availability and portfolios acquired from or

serviced by other institutions.

167