Wells Fargo 2014 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

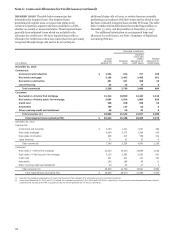

Note 6: Loans and Allowance for Credit Losses (continued)

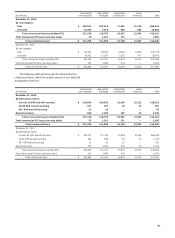

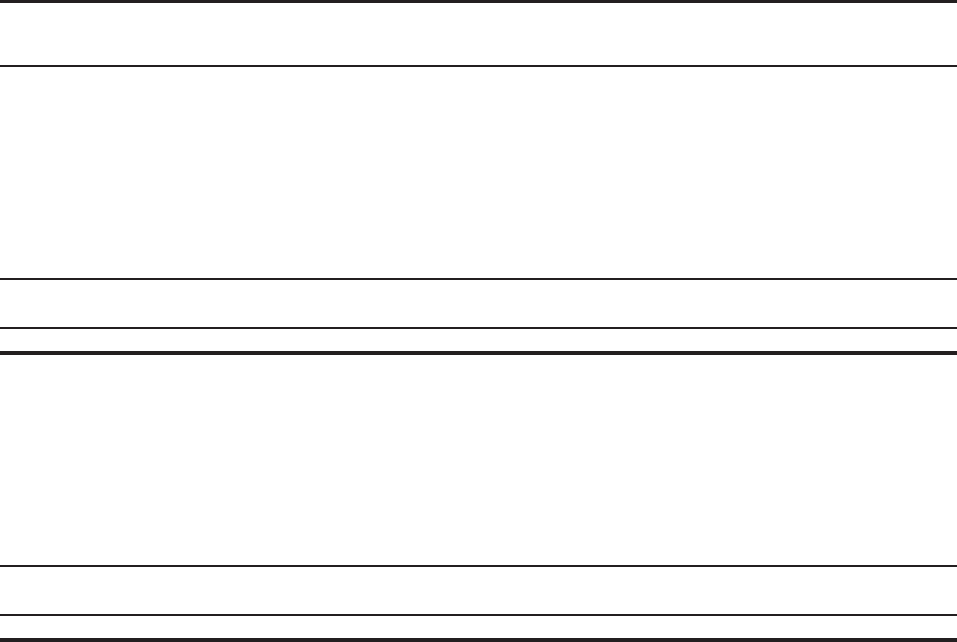

CONSUMER CREDIT QUALITY INDICATORS We have various Many of our loss estimation techniques used for the

classes of consumer loans that present unique risks. Loan allowance for credit losses rely on delinquency-based models;

delinquency, FICO credit scores and LTV for loan types are therefore, delinquency is an important indicator of credit quality

common credit quality indicators that we monitor and utilize in and the establishment of our allowance for credit losses. The

our evaluation of the appropriateness of the allowance for credit following table provides the outstanding balances of our

losses for the consumer portfolio segment. consumer portfolio by delinquency status.

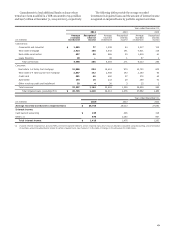

Real estate Real estate Other

(in millions)

1-4 family

first

mortgage

1-4 family

junior lien

mortgage Credit card Automobile

revolving

credit and

installment Total

December 31, 2014

By delinquency status:

Current-29 DPD $ 208,642 58,182 30,356 54,365 35,356 386,901

30-59 DPD 2,415 398 239 1,056 180 4,288

60-89 DPD 993 220 160 235 111 1,719

90-119 DPD 488 158 136 78 82 942

120-179 DPD 610 194 227 5 21 1,057

180+ DPD 4,258 464 1 1 13 4,737

Government insured/guaranteed loans (1) 26,268 — — — — 26,268

Total consumer loans (excluding PCI) 243,674 59,616 31,119 55,740 35,763 425,912

Total consumer PCI loans (carrying value) 21,712 101 — — — 21,813

Total consumer loans $ 265,386 59,717 31,119 55,740 35,763 447,725

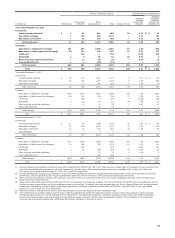

December 31, 2013

By delinquency status:

Current-29 DPD $ 193,371 64,230 26,218 49,699 31,944 365,462

30-59 DPD 2,784 461 201 852 179 4,477

60-89 DPD 1,157 253 143 186 111 1,850

90-119 DPD 587 182 124 66 76 1,035

120-179 DPD 747 216 195 4 20 1,182

180+ DPD 5,024 485 1 1 7 5,518

Government insured/guaranteed loans (1) 30,737 — — — 10,712 41,449

Total consumer loans (excluding PCI) 234,407 65,827 26,882 50,808 43,049 420,973

Total consumer PCI loans (carrying value) 24,100 123 — — — 24,223

Total consumer loans $ 258,507 65,950 26,882 50,808 43,049 445,196

(1) Represents loans whose repayments are predominantly insured by the FHA or guaranteed by the VA and student loans whose repayments are predominantly guaranteed by

agencies on behalf of the U.S. Department of Education under the Federal Family Education Loan Program (FFELP). Loans insured/guaranteed by the FHA/VA and 90+ DPD

totaled $16.2 billion at December 31, 2014, compared with $20.8 billion at December 31, 2013. On June 30, 2014, we transferred all government guaranteed student loans

to loans held for sale. Student loans 90+ DPD totaled $900 million at December 31, 2013.

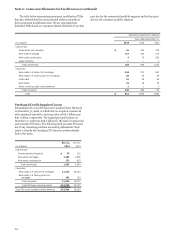

Of the $6.7 billion of consumer loans not government

insured/guaranteed that are 90 days or more past due at

December 31, 2014, $873 million was accruing, compared with

$7.7 billion past due and $902 million accruing at December 31,

2013.

Real estate 1-4 family first mortgage loans 180 days or more

past due totaled $4.3 billion, or 1.7% of total first mortgages

(excluding PCI), at December 31, 2014, compared with

$5.0 billion, or 2.1%, at December 31, 2013.

The following table provides a breakdown of our consumer

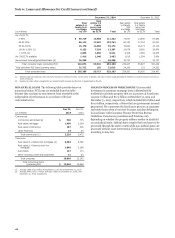

portfolio by updated FICO. We obtain FICO scores at loan

origination and the scores are updated at least quarterly. The

majority of our portfolio is underwritten with a FICO score of

680 and above. FICO is not available for certain loan types and

may not be obtained if we deem it unnecessary due to strong

collateral and other borrower attributes, primarily security-

based loans of $5.9 billion at December 31, 2014, and

$5.0 billion at December 31, 2013.

166