Wells Fargo 2014 Annual Report Download - page 174

Download and view the complete annual report

Please find page 174 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

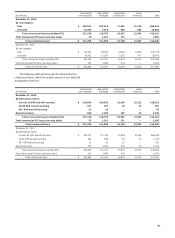

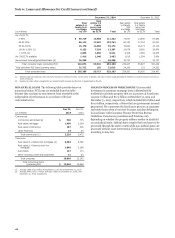

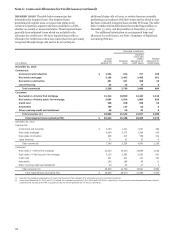

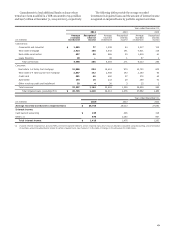

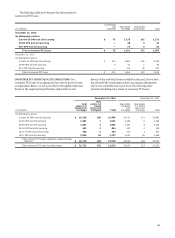

Note 6: Loans and Allowance for Credit Losses (continued)

TROUBLED DEBT RESTRUCTURINGS (TDRs) When, for

economic or legal reasons related to a borrower’s financial

difficulties, we grant a concession for other than an insignificant

period of time to a borrower that we would not otherwise

consider, the related loan is classified as a TDR. We do not

consider any loans modified through a loan resolution such as

foreclosure or short sale to be a TDR.

We may require some consumer borrowers experiencing

financial difficulty to make trial payments generally for a period

of three to four months, according to the terms of a planned

permanent modification, to determine if they can perform

according to those terms. These arrangements represent trial

modifications, which we classify and account for as TDRs. While

loans are in trial payment programs, their original terms are not

considered modified and they continue to advance through

delinquency status and accrue interest according to their original

terms. The planned modifications for these arrangements

predominantly involve interest rate reductions or other interest

rate concessions; however, the exact concession type and

resulting financial effect are usually not finalized and do not take

effect until the loan is permanently modified. The trial period

terms are developed in accordance with our proprietary

programs or the U.S. Treasury’s Making Homes Affordable

programs for real estate 1-4 family first lien (i.e. Home

Affordable Modification Program – HAMP) and junior lien (i.e.

Second Lien Modification Program – 2MP) mortgage loans.

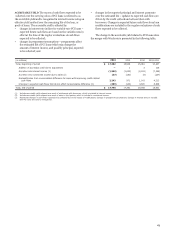

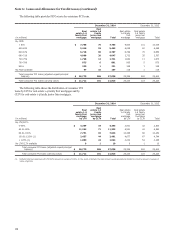

At December 31, 2014, the loans in trial modification period

were $149 million under HAMP, $34 million under 2MP and

$269 million under proprietary programs, compared with

$253 million, $45 million and $352 million at

December 31, 2013, respectively. Trial modifications with a

recorded investment of $167 million at December 31, 2014, and

$286 million at December 31, 2013, were accruing loans and

$285 million and $364 million, respectively, were nonaccruing

loans. Our experience is that substantially all of the mortgages

that enter a trial payment period program are successful in

completing the program requirements and are then permanently

modified at the end of the trial period. Our allowance process

considers the impact of those modifications that are probable to

occur.

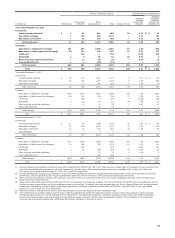

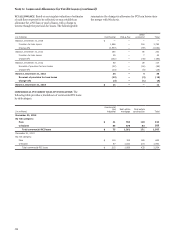

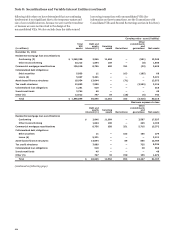

The following table summarizes our TDR modifications for

the periods presented by primary modification type and includes

the financial effects of these modifications. For those loans that

modify more than once, the table reflects each modification that

occurred during the period.

172