Wells Fargo 2014 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

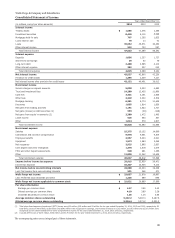

See the Glossary of Acronyms at the end of this Report for terms used throughout the Financial Statements and related Notes.

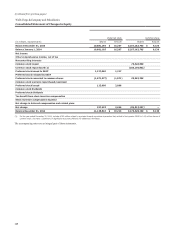

Note 1: Summary of Significant Accounting Policies

Wells Fargo & Company is a diversified financial services

company. We provide banking, insurance, trust and

investments, mortgage banking, investment banking, retail

banking, brokerage, and consumer and commercial finance

through banking stores, the internet and other distribution

channels to consumers, businesses and institutions in all 50

states, the District of Columbia, and in foreign countries. When

we refer to “Wells Fargo,” “the Company,” “we,” “our” or “us,” we

mean Wells Fargo & Company and Subsidiaries (consolidated).

Wells Fargo & Company (the Parent) is a financial holding

company and a bank holding company. We also hold a majority

interest in a real estate investment trust, which has publicly

traded preferred stock outstanding.

Our accounting and reporting policies conform with U.S.

generally accepted accounting principles (GAAP) and practices

in the financial services industry. To prepare the financial

statements in conformity with GAAP, management must make

estimates based on assumptions about future economic and

market conditions (for example, unemployment, market

liquidity, real estate prices, etc.) that affect the reported amounts

of assets and liabilities at the date of the financial statements and

income and expenses during the reporting period and the related

disclosures. Although our estimates contemplate current

conditions and how we expect them to change in the future, it is

reasonably possible that actual conditions could be worse than

anticipated in those estimates, which could materially affect our

results of operations and financial condition. Management has

made significant estimates in several areas, including allowance

for credit losses and purchased credit-impaired (PCI) loans

(Note 6 (Loans and Allowance for Credit Losses)), valuations of

residential mortgage servicing rights (MSRs) (Note 8

(Securitizations and Variable Interest Entities) and Note 9

(Mortgage Banking Activities)) and financial instruments

(Note 17 (Fair Values of Assets and Liabilities)) and income taxes

(Note 21 (Income Taxes)). Actual results could differ from those

estimates.

Accounting for Certain Factored Loan Receivable

Arrangements

The Company determined that certain factoring arrangements

previously included within commercial loans, which were

recorded with a corresponding obligation in other liabilities, did

not qualify as loan purchases under Accounting Standard

Codification (ASC) Topic 860 (Transfers and Servicing of

Financial Assets) based on interpretations of the specific

arrangements. Accordingly, we revised our commercial loan

balances for year-end 2012 and each of the quarters in 2013 in

order to present the Company’s lending trends on a comparable

basis over this period. This revision, which resulted in a

reduction to total commercial loans and a corresponding

decrease to other liabilities, did not impact the Company’s

consolidated net income or total cash flows. We reduced our

commercial loans by $3.5 billion, $3.2 billion, $2.1 billion,

$1.6 billion, and $1.2 billion at December 31, September 30,

June 30 and March 31, 2013, and December 31, 2012,

respectively, which represented less than 1% of total commercial

loans and less than 0.5% of our total loan portfolio. We also

appropriately revised other affected financial information,

including financial guarantees and financial ratios, to reflect this

revision.

Accounting Standards Adopted in 2014

In 2014, we adopted the following new accounting guidance:

• Accounting Standards Update (ASU) 2014-17, Business

Combinations (Topic 805): Pushdown Accounting;

• ASU 2014-14, Receivables - Troubled Debt Restructurings

by Creditors (Subtopic 310-40): Classification of Certain

Government-Guaranteed Mortgage Loans Upon

Foreclosure;

• ASU 2014-04, Receivables - Troubled Debt Restructurings

by Creditors (Subtopic 310-40): Reclassification of

Residential Real Estate Collateralized Consumer Mortgage

Loans upon Foreclosure;

• ASU 2013-11, Income Taxes (Topic 740): Presentation of an

Unrecognized Tax Benefit When a Net Operating Loss

Carryforward, a Similar Tax Loss, or a Tax Credit

Carryforward Exists; and

• ASU 2013-08, Financial Services - Investment Companies

(Topic 946): Amendments to the Scope, Measurement and

Disclosure Requirements.

ASU 2014-17 provides an acquired entity with the option to

apply pushdown accounting in its separate financial statements.

We adopted the guidance in fourth quarter 2014 with

prospective application. This Update did not have a material

effect on our consolidated financial statements.

ASU 2014-14 requires certain government-guaranteed

mortgage loans to be classified as other receivables upon

foreclosure and measured based on the loan balance expected to

be recovered from the guarantor. We early adopted this guidance

in fourth quarter 2014, effective as of January 1, 2014, through a

modified retrospective transition. Our adoption of this Update

did not have a material effect on our consolidated financial

statements. See Note 7 (Premises, Equipment, Lease

Commitments and Other Assets).

ASU 2014-04 clarifies the timing of when a creditor has taken

physical possession of residential real estate collateral for a

consumer mortgage loan, resulting in the reclassification of the

loan receivable to real estate owned. The guidance also requires

disclosure of the amount of foreclosed residential real estate

property held by the creditor and the recorded investment in

residential real estate mortgage loans that are in process of

foreclosure. We adopted this guidance in first quarter 2014. This

Update did not have a material effect on our consolidated

financial statements as this guidance was consistent with our

prior practice. See Note 6 (Loans and Allowance for Credit

Losses).

ASU 2013-11 provides guidance on the financial statement

presentation of an unrecognized tax benefit when a net operating

loss (NOL) carryforward, a similar tax loss, or a tax credit

carryforward exists. We adopted this guidance in first quarter

2014 with prospective application to all existing unrecognized

tax benefits at the effective date. This Update did not have a

material effect on our consolidated financial statements.

ASU 2013-08 changes the criteria companies use to assess

whether an entity is an investment company and requires new

disclosures for investment companies. We adopted this guidance

139