Wells Fargo 2014 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

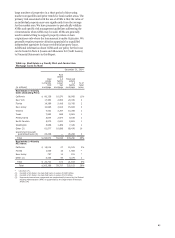

Risk Management - Credit Risk Management (continued)

Table 20: Commercial and Industrial Loans and Lease

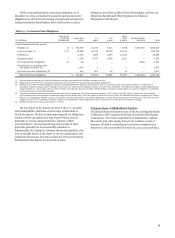

Financing by Industry (1)

December 31, 2014

Nonaccrual Total % of total

(in millions) loans portfolio (2) loans

Investors $ 40 39,192 5%

Financial institutions 26 38,256 4

Oil and gas 76 18,410 2

Food and beverage 16 14,029 2

Real estate lessor 3 13,030 2

Cyclical retailers 24 12,971 2

Healthcare 26 12,914 1

Industrial equipment 4 12,898 1

Technology 9 8,320 1

Public administration 10 8,120 1

Transportation 3 7,184 1

Business services 27 7,018 1

Other 298 91,760 (3) 10

Total $ 562 284,102 33%

(1) Industry categories are based on the North American Industry Classification

System and the amounts reported include foreign loans, which were reported

in a separate foreign loan class in prior periods. See Note 6 (Loans and

Allowance for Credit Losses) to Financial Statements in this Report for a

breakout of commercial foreign loans.

(2) Includes $75 million PCI loans, which are considered to be accruing due to the

existence of the accretable yield and not based on consideration given to

contractual interest payments.

(3) No other single category had loans in excess of $5.5 billion.

Risk mitigation actions, including the restructuring of

repayment terms, securing collateral or guarantees, and entering

into extensions, are based on a re-underwriting of the loan and

our assessment of the borrower’s ability to perform under the

agreed-upon terms. Extension terms generally range from six to

thirty-six months and may require that the borrower provide

additional economic support in the form of partial repayment, or

additional collateral or guarantees. In cases where the value of

collateral or financial condition of the borrower is insufficient to

repay our loan, we may rely upon the support of an outside

repayment guarantee in providing the extension.

Our ability to seek performance under a guarantee is

directly related to the guarantor’s creditworthiness, capacity and

willingness to perform, which is evaluated on an annual basis, or

more frequently as warranted. Our evaluation is based on the

most current financial information available and is focused on

various key financial metrics, including net worth, leverage, and

current and future liquidity. We consider the guarantor’s

reputation, creditworthiness, and willingness to work with us

based on our analysis as well as other lenders’ experience with

the guarantor. Our assessment of the guarantor’s credit strength

is reflected in our loan risk ratings for such loans. The loan risk

rating and accruing status are important factors in our allowance

methodology.

In considering the accrual status of the loan, we evaluate the

collateral and future cash flows as well as the anticipated support

of any repayment guarantor. In many cases the strength of the

guarantor provides sufficient assurance that full repayment of

the loan is expected. When full and timely collection of the loan

becomes uncertain, including the performance of the guarantor,

we place the loan on nonaccrual status. As appropriate, we also

charge the loan down in accordance with our charge-off policies,

generally to the net realizable value of the collateral securing the

loan, if any.

62