Wells Fargo 2014 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2014 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

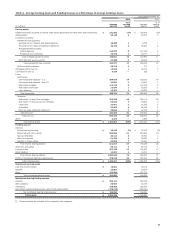

Earnings Performance (continued)

Community Banking reported net income of $14.2 billion in

2014, up $1.4 billion, or 11%, from $12.7 billion in 2013, which

was up 21% from $10.5 billion in 2012. Revenue was

$50.9 billion in 2014, an increase of $523 million, or 1%,

compared with $50.3 billion in 2013, which was down 6%

compared with $53.4 billion in 2012. The increase in revenue for

2014 was primarily driven by higher net interest income, gains

on sale of equity investments and debt securities, higher trust

and investment fees, and higher card fees, partially offset by

lower mortgage banking revenue, the phase out of the direct

deposit advance product during the first half of 2014, and lower

deferred compensation plan investment gains (offset in

employee benefits expense). Higher other income for 2014

compared with a year ago reflected larger ineffectiveness gains

on derivatives that qualify for hedge accounting and a gain on

sale of government guaranteed student loans in fourth quarter

2014. The decrease in 2013 was a result of lower mortgage

banking revenue, partially offset by higher trust and investment

fees, and revenue from debit, credit and merchant card volumes.

Lower other segment income for 2013 compared with 2012 was

due to larger ineffectiveness losses on derivatives that qualify for

hedge accounting and interest-related valuation changes on

certain mortgage-related assets carried at fair value. Average

core deposits increased $22.2 billion in 2014, or 4%, from 2013,

which increased $28.9 billion, or 5%, from 2012. Noninterest

expense decreased $597 million in 2014, or 2%, from 2013,

which declined $2.1 billion, or 7%, from 2012. The decrease in

noninterest expense for 2014 largely reflected lower mortgage

volume-related expenses and deferred compensation expense

(offset in revenue), partially offset by higher operating losses.

The decrease in noninterest expense for 2013 reflected lower

FDIC and other deposit insurance assessments primarily due to

lower FDIC assessment rates. The provision for credit losses of

$1.7 billion in 2014 was 39% lower than 2013, which was

$2.8 billion, or 60%, lower than 2012, due to improved

performance of the consumer real estate portfolio in both 2014

and 2013.

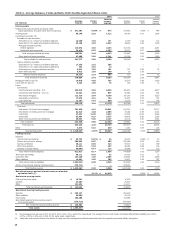

WHOLESALE BANKING provides financial solutions to

businesses across the United States and globally with annual

sales generally in excess of $20 million. Products and business

segments include Middle Market Commercial Banking,

Government and Institutional Banking, Corporate Banking,

Commercial Real Estate, Treasury Management, Wells Fargo

Capital Finance, Insurance, International, Real Estate Capital

Markets, Commercial Mortgage Servicing, Corporate Trust,

Equipment Finance, Wells Fargo Securities, Principal

Investments, Asset Backed Finance, and Asset Management.

Wholesale Banking cross-sell was 7.2 products per relationship

in September 2014, up from 7.1 in September 2013 and 6.8 in

September 2012. Table 9b provides additional financial

information for Wholesale Banking.

46