Sallie Mae 2010 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2010 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

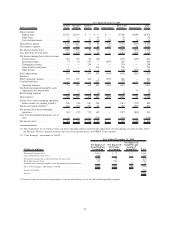

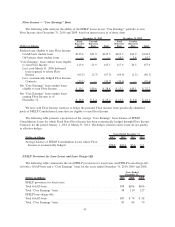

Net Loss from Discontinued Operations.

Net loss from discontinued operations in the year ended December 31, 2009 increased $5 million from

the prior year. Our Purchased Paper businesses are presented in discontinued operations for the current and

prior years.

Preferred Stock Dividend Expense

During 2009, we converted $339 million of our Series C Preferred Stock to common stock. As part of

this conversion, we delivered to the holders of the preferred stock: (1) approximately 17 million shares (the

number of common shares they would most likely receive if the preferred stock they held mandatorily

converted to common shares in the fourth quarter of 2010) plus (2) a discounted amount of the preferred stock

dividends the holders of the preferred stock would have received if they held the preferred stock through the

mandatory conversion date. The accounting treatment for this conversion resulted in additional expense

recorded as a part of preferred stock dividends for the period of approximately $53 million.

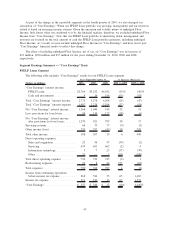

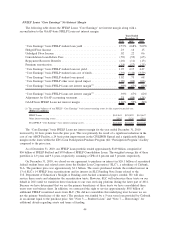

“Core Earnings” — Definition and Limitations

We prepare financial statements in accordance with GAAP. However, we also evaluate our business

segments on a basis that differs from GAAP. We refer to this different basis of presentation as “Core

Earnings”. We provide this “Core Earnings” basis of presentation on a consolidated basis for each business

segment because this is what we internally review when making management decisions regarding our

performance and how we allocate resources. We also refer to this information in our presentations with credit

rating agencies, lenders and investors. Because our “Core Earnings” basis of presentation corresponds to our

segment financial presentations, we are required by GAAP to provide “Core Earnings” disclosure in the notes

to our consolidated financial statements for our business segments. For additional information, see “Note 19 —

Segment Reporting.”

“Core Earnings” are not a substitute for reported results under GAAP. We use “Core Earnings” to manage

each business segment because “Core Earnings” reflect adjustments to GAAP financial results for three items,

discussed below, that create significant volatility mostly due to timing factors generally beyond the control of

management. Accordingly, we believe that “Core Earnings” provide management with a useful basis from

which to better evaluate results from ongoing operations against the business plan or against results from prior

periods. Consequently, we disclose this information as we believe it provides investors with additional

information regarding the operational and performance indicators that are most closely assessed by manage-

ment. The three items adjusted for in our “Core Earnings” presentations are (1) the off-balance sheet treatment

of certain securitization transactions, (2) our use of derivatives instruments to hedge our economic risks that

do not qualify for hedge accounting treatment or do qualify for hedge accounting treatment but result in

ineffectiveness and (3) the accounting for goodwill and acquired intangible assets.

While GAAP provides a uniform, comprehensive basis of accounting, for the reasons described above,

our “Core Earnings” basis of presentation does not. “Core Earnings” are subject to certain general and specific

limitations that investors should carefully consider. For example, there is no comprehensive, authoritative

guidance for management reporting. Our “Core Earnings” are not defined terms within GAAP and may not be

comparable to similarly titled measures reported by other companies. Accordingly, our “Core Earnings”

presentation does not represent a comprehensive basis of accounting. Investors, therefore, may not be able to

compare our performance with that of other financial services companies based upon “Core Earnings.” “Core

Earnings” results are only meant to supplement GAAP results by providing additional information regarding

the operational and performance indicators that are most closely used by management, our board of directors,

rating agencies, lenders and investors to assess performance.

Specific adjustments that management makes to GAAP results to derive our “Core Earnings” basis of

presentation are described in detail in the section entitled “‘Core Earnings’ — Definition and Limitations —

Differences between ‘Core Earnings’ and GAAP” of this Item 7.

35