Sallie Mae 2010 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2010 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

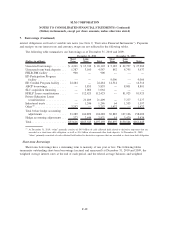

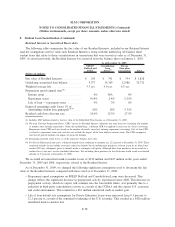

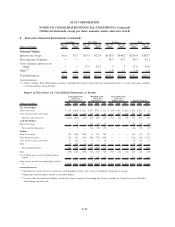

8. Student Loan Securitization (Continued)

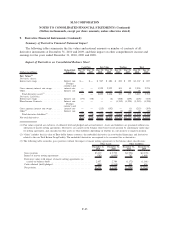

Retained Interest in Securitized Receivables

The following tables summarize the fair value of our Residual Interests, included in our Retained Interest

(and the assumptions used to value such Residual Interests), along with the underlying off-balance sheet

student loans that relate to those securitizations in transactions that were treated as sales as of December 31,

2009. As noted previously, the Residual Interest was removed from the balance sheet on January 1, 2010.

FFELP

Stafford and

PLUS

Consolidation

Loan

Trusts

(1)

Private

Education

Loan Trusts Total

As of December 31, 2009

(Dollars in millions)

Fair value of Residual Interests ............ $ 243 $ 791 $ 794 $ 1,828

Underlying securitized loan balance ......... 5,377 14,369 12,986 32,732

Weighted average life ................... 3.3yrs. 9.0 yrs. 6.3 yrs.

Prepayment speed (annual rate)

(2)

:

Interim status ....................... 0% N/A 0%

Repayment status .................... 0-14% 2-4% 2-15%

Life of loan — repayment status ......... 9% 3% 6%

Expected remaining credit losses (% of

outstanding student loan principal)

(3)(4)

..... .10% .25% 5.31%

Residual cash flows discount rate .......... 10.6% 12.3% 27.5%

(1) Includes $569 million related to the fair value of the Embedded Floor Income as of December 31, 2009.

(2) We used Constant Prepayment Rate (“CPR”) curves for Residual Interest valuations that were based on seasoning (the number

of months since entering repayment). Under this methodology, a different CPR was applied to each year of a loan’s seasoning.

Repayment status CPR used was based on the number of months since first entering repayment (seasoning). Life of loan CPR

is related to repayment status only and does not include the impact of the loan while in interim status. The CPR assumption

used for all periods includes the impact of projected defaults.

(3) Remaining expected credit losses as of the respective balance sheet date.

(4) For Private Education Loan trusts, estimated defaults from settlement to maturity are 12.2 percent at December 31, 2009. These

estimated defaults do not include recoveries related to defaults but do include prior purchases of loans at par by us when loans

reached 180 days delinquent (prior to default) under a contingent call option. Although these loan purchases do not result in a

realized loss to the trust, we have included them here. Not including these purchases in the disclosure would result in estimated

defaults of 9.3 percent at December 31, 2009.

We recorded net unrealized mark-to-market losses of $330 million and $425 million in the years ended

December 31, 2009 and 2008, respectively, related to the Residual Interest.

As of December 31, 2009, we changed the following significant assumptions used to determine the fair

value of the Residual Interests compared with those used as of December 31, 2008:

• Prepayment speed assumptions on FFELP Stafford and Consolidation Loans were decreased. This

change reflects the significant decrease in prepayment activity experienced since 2008. This decrease in

prepayment activity, which we expect will continue into the foreseeable future, was primarily due to a

reduction in third-party consolidation activity as a result of the CCRAA and the current U.S. economic

and credit environment. This resulted in a $61 million unrealized mark-to-market gain.

• Life of loan default rate assumptions for Private Education Loans were increased from 9.1 percent to

12.2 percent as a result of the continued weakening of the U.S. economy. This resulted in a $426 million

unrealized mark-to-market loss.

F-58

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)