Sallie Mae 2010 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2010 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

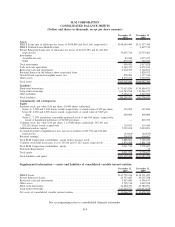

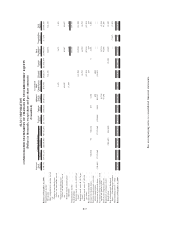

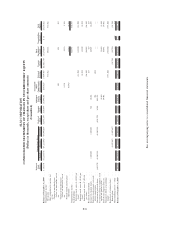

2. Significant Accounting Policies (Continued)

All our student loans, except for those which were sold under the ED’s Purchase Program, as discussed below,

are initially categorized as held for investment until there is certainty as to each specific loan’s ultimate

financing because we do not securitize all loans and most of our securitizations do not qualify for sales

treatment. It is only when we have selected the loans to securitize and that securitization transaction qualifies

as a sale do we transfer the loan into the held-for-sale classification and carry them at the lower of cost or fair

value. If we anticipate recognizing a gain related to the impending securitization, then the fair value of the

loans is higher than their respective cost basis and no valuation allowance is recorded.

Under The Ensuring Continued Access to Student Loans Act of 2008 (“ECASLA”), ED has implemented the

Loan Purchase Commitment Program (the “Purchase Program”) and Loan Participation Purchase Program (the

“Participation Program”). Under the Purchase Program, ED agreed to purchase eligible FFELP Loans at a set price

by September 30, 2010 at our option. Because we have the intent to sell such loans to ED we have classified all

loans eligible to be sold to ED under the Purchase Program as held-for-sale. These loans are included in the

“FFELP Stafford Held-for-Sale Loans” line on our consolidated balance sheets.

Student Loan Income

For loans classified as held for investment we recognize student loan interest income as earned, adjusted for

the amortization of premiums and capitalized direct origination costs, accretion of discounts, and Repayment

Borrower Benefits. These adjustments result in income being recognized based upon the expected yield of the

loan over its life after giving effect to prepayments and extensions, and to estimates related to Repayment

Borrower Benefits. The estimate of the prepayment speed includes the effect of consolidations, voluntary

prepayments and student loan defaults, all of which shorten the life of loan. Prepayment speed estimates also

consider the utilization of deferment and forbearance, which lengthen the life of loan. For Repayment Borrower

Benefits, the estimates of their effect on student loan yield are based on analyses of historical payment behavior

of borrowers who are eligible for the incentives and its effect on the ultimate qualification rate for these

incentives. If our expectation is that the utilization of Repayment Borrower Benefits were to increase in future

periods, it would reduce our current student loan yield. We regularly evaluate the assumptions used to estimate

the prepayment speeds and the qualification rates used for Repayment Borrower Benefits. In instances where

there are changes to the assumptions, amortization is adjusted on a cumulative basis to reflect the change since

the acquisition of the loan. We also pay an annual 105 basis point Consolidation Loan Rebate Fee on FFELP

Consolidation Loans which is netted against student loan interest income. Additionally, interest earned on student

loans reflects potential non-payment adjustments in accordance with our uncollectible interest recognition policy

as discussed further in “Allowance for Student Loan Losses” below. We do not amortize any premiums, discounts

or other adjustments to the basis of student loans when they are classified as held for sale.

Allowance for Loan Losses

We consider a loan to be impaired when, based on current information, it is probable that we will not

receive all contractual amounts due. When making our assessment as to whether a loan is impaired, we also

take into account more than insignificant delays in payment. We generally evaluate impaired loans on an

aggregate basis by grouping similar loans. Impaired loans also include those loans which are individually

assessed and measured for impairment, such as in a troubled debt restructuring. We maintain an allowance for

loan losses at an amount sufficient to absorb losses incurred in our portfolios at the reporting date based on a

projection of estimated probable credit losses incurred in the portfolio.

When calculating the allowance for loan loss we estimate the amount of loans which will default over the

next two years and how much we will recover over time related to the defaulted amount. Our historical

experience indicates that, on average, the time between the date that a borrower experiences a default causing

F-13

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)