Sallie Mae 2010 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2010 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

|

|

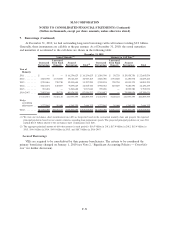

9. Derivative Financial Instruments (Continued)

Accounting for Derivative Instruments

Derivative instruments that are used as part of our interest rate and foreign currency risk management

strategy include interest rate swaps, basis swaps, cross-currency interest rate swaps, interest rate futures

contracts, and interest rate floor and cap contracts with indices that relate to the pricing of specific balance

sheet assets and liabilities, including the Residual Interests from off-balance sheet securitizations (prior to the

adoption of topic updates to new consolidation accounting guidance adopted on January 1, 2010, see Note 2,

“Significant Accounting Policies — Consolidation”). The accounting for derivative instruments requires that

every derivative instrument, including certain derivative instruments embedded in other contracts, be recorded

on the balance sheet as either an asset or liability measured at its fair value. As more fully described below, if

certain criteria are met, derivative instruments are classified and accounted for by us as either fair value or

cash flow hedges. If these criteria are not met, the derivative financial instruments are accounted for as

trading.

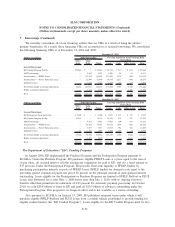

Fair Value Hedges

Fair value hedges are generally used by us to hedge the exposure to changes in fair value of a recognized

fixed rate asset or liability. We enter into interest rate swaps to economically convert fixed rate assets into

variable rate assets and fixed rate debt into variable rate debt. We also enter into cross-currency interest rate

swaps to economically convert foreign currency denominated fixed and floating debt to U.S. dollar denom-

inated variable debt. For fair value hedges, we generally consider all components of the derivative’s gain

and/or loss when assessing hedge effectiveness (in some cases we exclude time-value components) and

generally hedge changes in fair values due to interest rates or interest rates and foreign currency exchange

rates or the total change in fair values.

Cash Flow Hedges

We use cash flow hedges to hedge the exposure to variability in cash flows for a forecasted debt issuance

and for exposure to variability in cash flows of floating rate debt. This strategy is used primarily to minimize

the exposure to volatility from future changes in interest rates. Gains and losses on the effective portion of a

qualifying hedge are recorded in accumulated in other comprehensive income and ineffectiveness is recorded

immediately to earnings. In the case of a forecasted debt issuance, gains and losses are reclassified to earnings

over the period which the stated hedged transaction affects earnings. If we determine it is not probable that

the anticipated transaction will occur, gains and losses are reclassified immediately to earnings. In assessing

hedge effectiveness, generally all components of each derivative’s gains or losses are included in the

assessment. We generally hedge exposure to changes in cash flows due to changes in interest rates or total

changes in cash flow.

Trading Activities

When derivative instruments do not qualify as hedges, they are accounted for as trading instruments

where all changes in fair value are recorded through earnings. We sell interest rate floors (Floor Income

Contracts) to hedge the Embedded Floor Income options in student loan assets. The Floor Income Contracts

are written options which have a more stringent hedge effectiveness hurdle to meet. Therefore, Floor Income

Contracts do not qualify for hedge accounting treatment, and are recorded as trading instruments. Regardless

of the accounting treatment, we consider these contracts to be economic hedges for risk management purposes.

We use this strategy to minimize our exposure to changes in interest rates.

F-61

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)