Sallie Mae 2010 Annual Report Download - page 223

Download and view the complete annual report

Please find page 223 of the 2010 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226

|

|

Embedded Floor Income — Embedded Floor Income is Floor Income (see definition below) that is

earned on off-balance sheet student loans that are in securitization trusts we sponsor. At the time of the

securitization, the value of Embedded Fixed Rate Floor Income is included in the initial valuation of the

Residual Interest (see definition below) and the gain or loss on sale of the student loans. Embedded Floor

Income is also included in the quarterly fair value adjustments of the Residual Interest.

Exceptional Performer — The exceptional performer designation is determined by ED in recognition of

a servicer meeting certain performance standards set by ED in servicing FFELP Loans. Upon receiving the

designation, the servicer receives reimbursement on default claims higher than the legislated Risk Sharing

levels on federally guaranteed student loans for all loans serviced for a period of at least 270 days before the

date of default. The servicer is entitled to receive this benefit as long as it remains in compliance with the

required servicing standards, which are assessed on an annual and quarterly basis through compliance audits

and other criteria. The annual assessment is in part based upon subjective factors which alone may form the

basis for an ED determination to withdraw the designation. If the designation is withdrawn, Risk Sharing may

be applied retroactively to the date of the occurrence that resulted in noncompliance. The CCRAA eliminated

the EP designation effective October 1, 2007. See also Appendix A “Federal Family Education Loan

Program.”

FFELP — The Federal Family Education Loan Program, formerly the Guaranteed Student Loan

Program.

FFELP Consolidation Loans — Under the FFELP, borrowers with multiple eligible student loans may

consolidate them into a single student loan with one lender at a fixed rate for the life of the loan. The new

loan is considered a FFELP Consolidation Loan. Typically a borrower may consolidate his student loans only

once unless the borrower has another eligible loan to consolidate with the existing FFELP Consolidation Loan.

The borrower rate on a FFELP Consolidation Loan is fixed for the term of the loan and is set by the weighted

average interest rate of the loans being consolidated, rounded up to the nearest 1/8th of a percent, not to

exceed 8.25 percent. In low interest rate environments, FFELP Consolidation Loans provide an attractive

refinancing opportunity to certain borrowers because they allow borrowers to consolidate variable rate loans

into a long-term fixed rate loan. Holders of FFELP Consolidation Loans are eligible to earn interest under the

Special Allowance Payment (“SAP”) formula. In April 2008, we suspended originating new FFELP Consoli-

dation Loans.

FFELP Stafford and Other Student Loans — Education loans to students or parents of students that

are guaranteed or reinsured under the FFELP. The loans are primarily Stafford loans but also include PLUS

and HEAL loans.

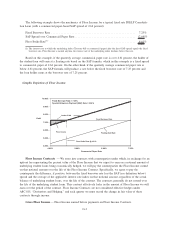

Fixed Rate Floor Income — Fixed Rate Floor Income is Floor Income associated with student loans

with borrower rates that are fixed to term (primarily FFELP Consolidation Loans and Stafford Loans

originated on or after July 1, 2006).

Floor Income — FFELP Loans generally earn interest at the higher of either the borrower rate, which is

fixed over a period of time, or a floating rate based on the SAP formula. We generally finance our student

loan portfolio with floating rate debt whose interest is matched closely to the floating nature of the applicable

SAP formula. If interest rates decline to a level at which the borrower rate exceeds the SAP formula rate, we

continue to earn interest on the loan at the fixed borrower rate while the floating rate interest on our debt

continues to decline. In these interest rate environments, we refer to the additional spread it earns between the

fixed borrower rate and the SAP formula rate as Floor Income. Depending on the type of student loan and

when it was originated, the borrower rate is either fixed to term or is reset to a market rate each July 1. As a

result, for loans where the borrower rate is fixed to term, we may earn Floor Income for an extended period

of time, and for those loans where the borrower interest rate is reset annually on July 1, we may earn Floor

Income to the next reset date. In accordance with legislation enacted in 2006, lenders are required to rebate

Floor Income to ED for all FFELP Loans disbursed on or after April 1, 2006.

G-2