Sallie Mae 2006 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

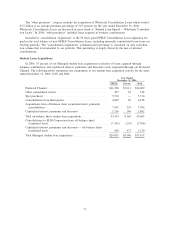

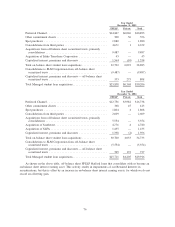

interest. Traditional student borrowers use the proceeds of these loans to obtain higher education, which

increases the likelihood of obtaining employment at higher income levels than would be available without the

additional education. As a result, the borrowers’ repayment capability improves between the time the loan is

made and the time they enter the post-education work force. We generally allow the loan repayment period on

traditional higher education Private Education Loans to begin six months after the borrower leaves school

(consistent with our federally regulated FFELP loans). This provides the borrower time after graduation to

obtain a job to service the debt. For borrowers that need more time or experience other hardships, we permit

additional delays in payment or partial payments (both referred to as forbearances) when we believe additional

time will improve the borrower’s ability to repay the loan. Forbearance is also granted to borrowers who may

experience temporary hardship after entering repayment, when we believe that it will increase the likelihood

of ultimate collection of the loan. Forbearance can be requested by the borrower or initiated by the Company

and is granted within established policies that include limits on the number of forbearance months granted

consecutively and limits on the total number of forbearance months granted over the life of the loan. In some

instances of forbearance, we require good-faith payments or continuing partial payments. Exceptions to

forbearance policies are permitted in limited circumstances and only when such exceptions are judged to

increase the likelihood of ultimate collection of the loan.

Forbearance does not grant any reduction in the total repayment obligation (principal or interest) but does

allow for the temporary cessation of borrower payments (on a prospective and/or retroactive basis) or a

reduction in monthly payments for an agreed period of time. The forbearance period extends the original term

of the loan. While the loan is in forbearance, interest continues to accrue and is capitalized as principal upon

the loan re-entering repayment status. Loans exiting forbearance into repayment status are considered current

regardless of their previous delinquency status.

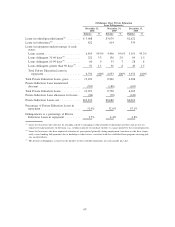

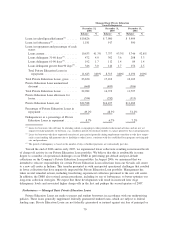

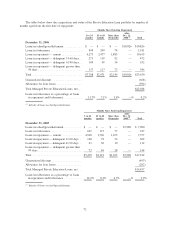

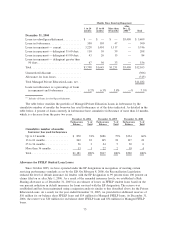

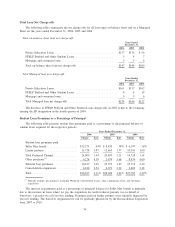

Forbearance is used most heavily immediately after the loan enters repayment. As indicated in the tables

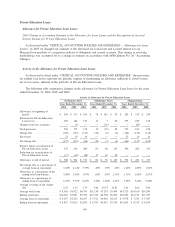

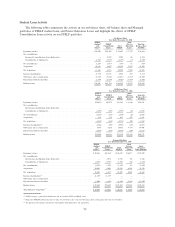

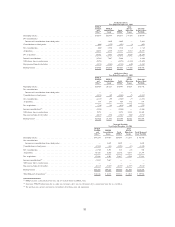

below that show the composition and status of the Managed Private Education Loan portfolio by number of

months aged from the first date of repayment, the percentage of loans in forbearance decreases the longer the

loans have been in repayment. At December 31, 2006, loans in forbearance as a percentage of loans in

repayment and forbearance is 11.7 percent for loans that have been in repayment one to twenty-four months.

The percentage drops to 3.4 percent for loans that have been in repayment more than 48 months.

Approximately 76 percent of our Managed Private Education Loans in forbearance have been in repayment

less than 24 months. These borrowers are essentially extending their grace period as they transition to the

workforce. Forbearance continues to be a positive collection tool for Private Education Loans as we believe it

can provide the borrower with sufficient time to obtain employment and income to support his or her

obligation. We consider the potential impact of forbearance in the determination of the loan loss reserves.

71