Sallie Mae 2006 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

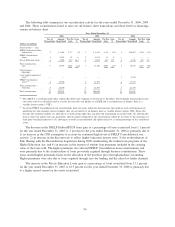

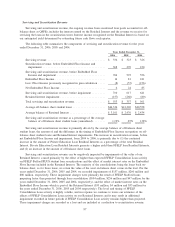

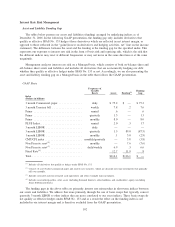

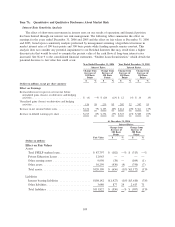

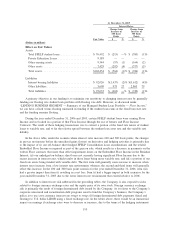

Interest Rate Risk Management

Asset and Liability Funding Gap

The tables below present our assets and liabilities (funding) arranged by underlying indices as of

December 31, 2006. In the following GAAP presentation, the funding gap only includes derivatives that

qualify as effective SFAS No. 133 hedges (those derivatives which are reflected in net interest margin, as

opposed to those reflected in the “gains/(losses) on derivatives and hedging activities, net” line on the income

statement). The difference between the asset and the funding is the funding gap for the specified index. This

represents our exposure to interest rate risk in the form of basis risk and repricing risk, which is the risk that

the different indices may reset at different frequencies or may not move in the same direction or at the same

magnitude.

Management analyzes interest rate risk on a Managed basis, which consists of both on-balance sheet and

off-balance sheet assets and liabilities and includes all derivatives that are economically hedging our debt

whether they qualify as effective hedges under SFAS No. 133 or not. Accordingly, we are also presenting the

asset and liability funding gap on a Managed basis in the table that follows the GAAP presentation.

GAAP Basis

Frequency of

Variable

Resets Assets Funding

(1)

Funding

Gap

Index

(Dollars in billions)

3 month Commercial paper ............... daily $ 75.2 $ — $ 75.2

3 month Treasury bill . .................. weekly 7.8 .2 7.6

Prime ............................... annual .6 — .6

Prime ............................... quarterly 1.3 — 1.3

Prime ............................... monthly 8.0 — 8.0

PLUS Index........................... annual 2.0 .3 1.7

3-month LIBOR ....................... daily — — —

3-month LIBOR ....................... quarterly 1.5 89.0 (87.5)

1-month LIBOR ....................... monthly .1 3.0 (2.9)

CMT/CPI index ........................ monthly/quarterly — 3.8 (3.8)

Non Discrete reset

(2)

.................... monthly — 7.6 (7.6)

Non Discrete reset

(3)

.................... daily/weekly 6.9 .3 6.6

Fixed Rate

(4)

.......................... 12.7 11.9 .8

Total ................................ $116.1 $116.1 $ —

(1)

Includes all derivatives that qualify as hedges under SFAS No. 133.

(2)

Consists of asset-backed commercial paper and auction rate securities, which are discount note type instruments that generally

roll over monthly.

(3)

Includes restricted and non-restricted cash equivalents and other overnight type instruments.

(4)

Includes receivables/payables, other assets (including Retained Interest), other liabilities and stockholders’ equity (excluding

Series B Preferred Stock).

The funding gaps in the above table are primarily interest rate mismatches in short-term indices between

our assets and liabilities. We address this issue primarily through the use of basis swaps that typically convert

quarterly 3-month LIBOR to other indices that are more correlated to our asset indices. These basis swaps do

not qualify as effective hedges under SFAS No. 133 and as a result the effect on the funding index is not

included in our interest margin and is therefore excluded from the GAAP presentation.

102