Sallie Mae 2006 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

|

|

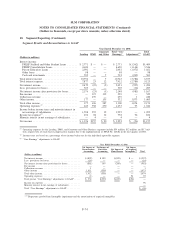

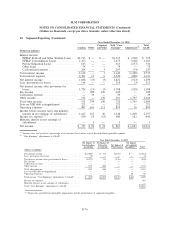

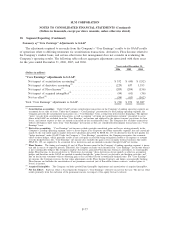

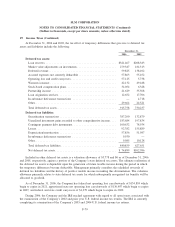

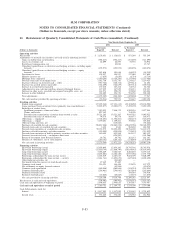

22. Subsequent Events

On January 25, 2007, the Attorney General of Illinois filed a lawsuit against Arrow Financial Services,

LLC (“AFS”) in the Circuit Court of Cook County, Illinois alleging that AFS violated the Illinois Consumer

Fraud and Deceptive Practices Act and the federal Fair Debt Collections Practices Act. The lawsuit seeks to

enjoin AFS from violating the Illinois Consumer Fraud and Deceptive Practices Act and from engaging in

debt management and collection services in or from the State of Illinois. The lawsuit also seeks to rescind

certain agreements to pay back debt between AFS and Illinois consumers, to pay restitution to all consumers

who have been harmed by AFS’s alleged unlawful practices, to impose a statutory civil penalty of $50,000 and

to impose a civil penalty of $50,000 per violation ($60,000 per violation if the consumer is 65 years of age or

older). The lawsuit alleges that as of January 25, 2007, 660 complaints against Arrow Financial have been

filed with the Office of the Illinois Attorney General since 1999 and over 800 complaints have been filed with

the Better Business Bureau. As of December 29, 2006, the Company owns 88 percent of the membership

interests in AFS Holdings, LLC, the parent company of AFS.

ED Dear Colleague Letter Restating Requirements of 9.5 Percent Loan Special Allowance Payments

Eligibility

On January, 23, 2007, ED issued a “Dear Colleague Letter” to the industry. The letter restated the

requirements of the Higher Education Act of 1965, as amended, and ED’s regulations that control whether

FFELP loans made or acquired with funds derived from tax-exempt obligations are eligible for 9.5 percent

SAP. The letter’s restatement is consistent with claims asserted by the ED’s Office of Inspector General

(“OIG”) in their Final Audit Report on “Special Allowance Payments to Nelnet for Loans Funded by Tax-

Exempt Obligations” issued on September 29, 2006. On January 24, 2007, ED sent a letter to the Company

which sets forth the same restatement and also imposes audit and certification requirements for any 9.5 percent

SAP billings after September 30, 2006. On February 15, 2007, the Company delivered a letter to ED, which,

subject to certain conditions, including no successful challenge by an industry participant of ED’s restated

eligibility requirements for 9.5 percent SAP, stated that the Company would make no further claims for

9.5 percent SAP retroactive to October 1, 2006, and for those loans affected, would bill at the standard SAP

rate. In the fourth quarter of 2006, the Company accrued $2.4 million in interest income in excess of income

based upon the standard special allowance rate on its portfolio of loans that is entitled to receive 9.5 percent

SAP. After adjusting for the fourth quarter accrual, the Company earned a total of $13.1 million in interest

income in excess of standard special allowance payments during 2006. Regardless of the issuance of the “Dear

Colleague Letter,” the Company’s portfolio of 9.5 percent loans and associated SAP billings have been in a

constant state of decline. As a result, the Company’s voluntary forgoing of future claims of 9.5 percent SAP

will not have a material impact on future earnings. In addition, the Company will record an impairment of

$9 million related to the intangible asset associated with the 9.5 percent loans acquired in business

combinations.

F-84

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)