Sallie Mae 2006 Annual Report Download - page 191

Download and view the complete annual report

Please find page 191 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

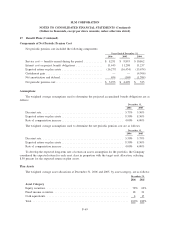

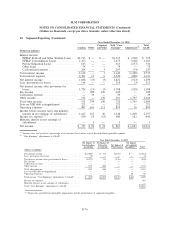

18. Segment Reporting (Continued)

ended December 31, 2006, 2005 and 2004. USA Funds is the Company’s largest customer in both the DMO

and Corporate and Other segments. During the years ended December 31, 2006, 2005 and 2004, USA Funds

accounted for 31 percent, 36 percent and 44 percent, respectively, of the aggregate revenues generated by the

Company’s DMO and Corporate and Other reportable segments. No other customers accounted for more than

10 percent of total revenues in those segments for the years mentioned.

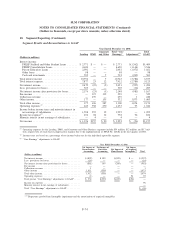

Lending

In the Company’s Lending business segment, the Company originates and acquires both federally

guaranteed student loans, which are administered by ED, and Private Education Loans, which are not federally

guaranteed. Private Education Loans are primarily used by borrowers to supplement FFELP loans to meet the

rising cost of education. As of December 31, 2006, the Company manages $142 billion of student loans, of

which $120 billion or 84 percent are federally insured, and serves nearly 10 million student and parent

customers. In addition to education lending, the Company also originates mortgage and consumer loans with

the intent of selling the majority of such loans. In 2006, the Company originated $2 billion in mortgage and

consumer loans and its mortgage and consumer loan portfolio totaled $619 million at December 31, 2006, of

which $119 million pertains to mortgages in the held for sale portfolio.

In addition to its federally insured FFELP products, the Company originates and acquires Private

Education Loans which consist of two general types: (1) those that are designed to bridge the gap between the

cost of higher education and the amount financed through either capped federally insured loans or the

borrowers’ resources, and (2) those that are used to meet the needs of students in alternative learning programs

such as career training, distance learning and lifelong learning programs. Most higher education Private

Education Loans are made in conjunction with a FFELP Stafford loan and as such are marketed through the

same channel as FFELP loans by the same sales force. Unlike FFELP loans, Private Education Loans are

subject to the full credit risk of the borrower. The Company manages this additional risk through industry-

tested loan underwriting standards and a combination of higher interest rates and loan origination fees that

compensate the Company for the higher risk.

DMO

The Company’s DMO operating segment provides a wide range of accounts receivable and collections

services including student loan default aversion services, defaulted student loan portfolio management services,

contingency collections services for student loans and other asset classes, and accounts receivable management

and collection for purchased portfolios of receivables that are delinquent or have been charged off by their

original creditors as well as sub-performing and non-performing mortgage loans. The Company’s DMO

operating segment serves the student loan marketplace through a broad array of default management services

on a contingency fee or other pay-for-performance basis to 14 FFELP guarantors and for campus based

programs.

In addition to collecting on its own purchased receivables and mortgage loans, the DMO operating

segment provides receivable management and collection services for large federal agencies, credit card clients

and other holders of consumer debt.

Corporate and Other

The Company’s Corporate and Other business segment includes the aggregate activity of its smaller

operating segments primarily its Guarantor Servicing, student loan servicing operating segments, and its

F-72

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)