Sallie Mae 2006 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

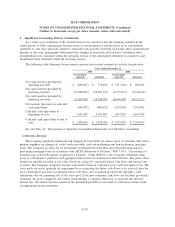

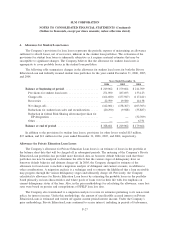

3. Student Loans (Continued)

borrowers that need more time or experience other hardships, the Company permits additional delays in

payment or partial payments (both referred to as forbearances) when it believes additional time will improve

the borrower’s ability to repay the loan. Forbearance is also granted to borrowers who may experience

temporary hardship after entering repayment, when the Company believes that it will increase the likelihood

of ultimate collection of the loan.

Forbearance does not grant any reduction in the total repayment obligation (principal or interest) but does

allow for the temporary cessation of borrower payments (on a prospective and/or retroactive basis) or a

reduction in monthly payments for an agreed period of time. The forbearance period extends the original term

of the loan. While the loan is in forbearance, interest continues to accrue and is recorded in interest income in

the accompanying consolidated financial statements, and is capitalized as principal upon the loan re-entering

repayment status. Loans exiting forbearance into repayment status are considered current regardless of their

previous delinquency status.

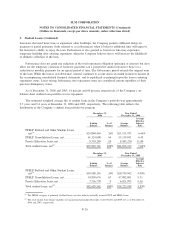

As of December 31, 2006 and 2005, 61 percent and 60 percent, respectively, of the Company’s on-

balance sheet student loan portfolio was in repayment.

The estimated weighted average life of student loans in the Company’s portfolio was approximately

9.7 years and 9.4 years at December 31, 2006 and 2005, respectively. The following table reflects the

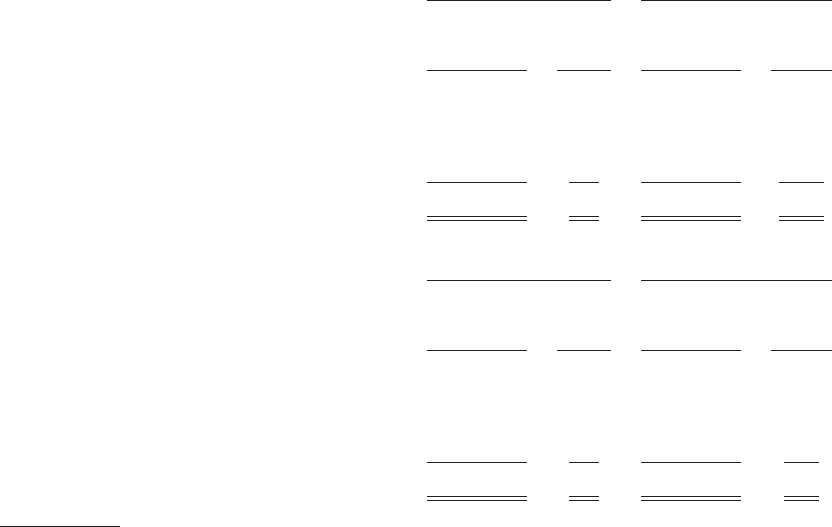

distribution of the Company’s student loan portfolio by program.

Ending

Balance

%of

Balance

Average

Balance

Average

Effective

Interest

Rate

December 31,

2006

Year Ended

December 31, 2006

FFELP Stafford and Other Student Loans,

net

(1)

............................... $24,840,464 26% $21,151,871 6.66%

FFELP Consolidation Loans, net ............. 61,324,008 64 55,119,011 6.43

Private Education loans, net ................ 9,755,289 10 8,585,270 11.90

Total student loans, net

(2)

.................. $95,919,761 100% $84,856,152 7.04%

Ending

Balance

%of

Balance

Average

Balance

Average

Effective

Interest

Rate

December 31,

2005

Year Ended

December 31, 2005

FFELP Stafford and Other Student Loans,

net

(1)

............................... $19,988,116 24% $20,719,942 4.90%

FFELP Consolidation Loans, net ............. 54,858,676 67 47,082,001 5.31

Private Education loans, net ................ 7,756,770 9 6,921,975 9.16

Total student loans, net

(2)

.................. $82,603,562 100% $74,723,918 5.55%

(1)

The FFELP category is primarily Stafford loans, but also includes federally insured PLUS and HEAL loans.

(2)

The total student loan balance includes net unamortized premiums/discounts of $1,198,404 and $909,417 as of December 31,

2006 and 2005, respectively.

F-26

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)