Sallie Mae 2006 Annual Report Download - page 211

Download and view the complete annual report

Please find page 211 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215

|

|

graduated, income-sensitive and extended repayment schedule, if applicable, to all borrowers entering

repayment.

Grace Periods, Deferral Periods and Forbearance Periods. After the borrower stops pursuing at least a

half-time course of study, he must begin to repay principal of a Stafford Loan following the grace period.

However, no principal repayments need be made, subject to some conditions, during deferment and

forbearance periods.

For borrowers whose first loans are disbursed on or after July 1, 1993, repayment of principal may be

deferred while the borrower returns to school at least half-time. Additional deferrals are available, when the

borrower is:

• enrolled in an approved graduate fellowship program or rehabilitation program; or

• seeking, but unable to find, full-time employment (subject to a maximum deferment of 3 years); or

• having an economic hardship, as defined in the Act (subject to a maximum deferment of 3 years); or

• serving on active duty during a war or other military operation or national emergency, or performing

qualifying National Guard duty during a war or other military operation or national emergency (subject

to a maximum deferment of 3 years, and effective July 1, 2006 on loans made on or after July 1,

2001).

The Higher Education Act also permits, and in some cases requires, “forbearance” periods from loan

collection in some circumstances. Interest that accrues during forbearance is never subsidized. Interest that

accrues during deferment periods may be subsidized.

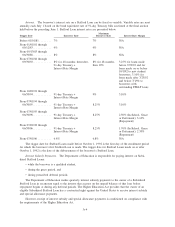

PLUS and SLS Loan Programs

The Higher Education Act authorizes PLUS Loans to be made to graduate or professional students

(effective July 1, 2006) and parents of eligible dependent students and previously authorized SLS Loans to be

made to the categories of students now served by the Unsubsidized Stafford Loan program. Only borrowers

who have no adverse credit history or who are able to secure an endorser without an adverse credit history are

eligible for PLUS Loans. The basic provisions applicable to PLUS and SLS Loans are similar to those of

Stafford Loans for federal insurance and reinsurance. However, interest subsidy payments are not available

under the PLUS and SLS programs and, in some instances, special allowance payments are more restricted.

Loan Limits. PLUS and SLS Loans disbursed before July 1, 1993 were limited to $4,000 per academic

year with a maximum aggregate amount of $20,000.

The annual and aggregate amounts of PLUS Loans first disbursed on or after July 1, 1993 are limited

only to the difference between the cost of the student’s education and other financial aid received, including

scholarship, grants and other student loans.

Interest. The interest rate for a PLUS or SLS Loan depends on the date of disbursement and period of

enrollment. The interest rates for PLUS Loans and SLS Loans are presented in the following chart. Until

July 1, 2001, the 1-year index was the bond equivalent rate of 52-week Treasury bills auctioned at the final

auction held prior to each June 1. Beginning July 1, 2001, the 1-year index is the weekly average 1-year

constant maturity Treasury yield determined the preceding June 26.

A-8