Sallie Mae 2006 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

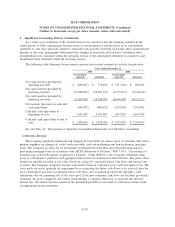

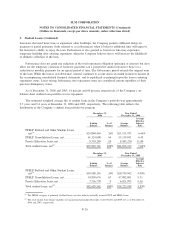

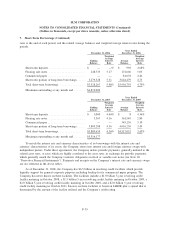

4. Allowance for Student Loan Losses

The Company’s provisions for loan losses represents the periodic expense of maintaining an allowance

sufficient to absorb losses, net of recoveries, inherent in the student loan portfolios. The evaluation of the

provisions for student loan losses is inherently subjective as it requires material estimates that may be

susceptible to significant changes. The Company believes that the allowance for student loan losses is

appropriate to cover probable losses in the student loan portfolios.

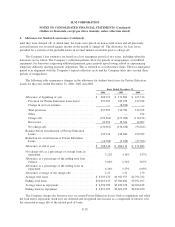

The following table summarizes changes in the allowance for student loan losses for both the Private

Education Loan and federally insured student loan portfolios for the years ended December 31, 2006, 2005,

and 2004.

2006 2005 2004

Years Ended December 31,

Balance at beginning of period ...................... $219,062 $ 179,664 $ 211,709

Provisions for student loan losses ................... 271,890 187,693 133,123

Charge-offs.................................... (164,600) (157,947) (117,441)

Recoveries .................................... 22,599 19,580 14,138

Net charge-offs ................................. (142,001) (138,367) (103,303)

Reductions for student loan sales and securitizations ..... (20,290) (9,928) (35,887)

Reduction in federal Risk Sharing allowance/provision for

EP designation ............................... — — (32,709)

Other ........................................ — — 6,731

Balance at end of period ........................... $328,661 $ 219,062 $ 179,664

In addition to the provisions for student loan losses, provisions for other losses totaled $15 million,

$15 million, and $11 million for the years ended December 31, 2006, 2005, and 2004, respectively.

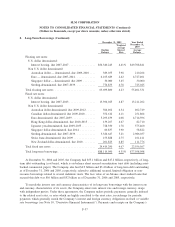

Allowance for Private Education Loan Losses

The Company’s allowance for Private Education Loan losses is an estimate of losses in the portfolio at

the balance sheet date that will be charged off in subsequent periods. The maturing of the Company’s Private

Education Loan portfolios has provided more historical data on borrower default behavior such that those

portfolios can now be analyzed to determine the effects that the various stages of delinquency have on

borrower default behavior and ultimate charge-off. In 2005, the Company changed its estimate of the

allowance for loan losses to include a migration analysis of delinquent and current accounts, in addition to

other considerations. A migration analysis is a technique used to estimate the likelihood that a loan receivable

may progress through the various delinquency stages and ultimately charge off. Previously, the Company

calculated its allowance for Private Education Loan losses by estimating the probable losses in the portfolio

based primarily on loan characteristics and where pools of loans were in their life with less emphasis on

current delinquency status of the loan. Also, in the prior methodology for calculating the allowance, some loss

rates were based on proxies and extrapolations of FFELP loan loss data.

The Company also transitioned to a migration analysis to revise its estimates pertaining to its non-accrual

policy for interest income. Under this methodology, the amount of uncollectible accrued interest on Private

Education Loans is estimated and written off against current period interest income. Under the Company’s

prior methodology, Private Education Loans continued to accrue interest, including in periods of forbearance,

F-27

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)