Sallie Mae 2006 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

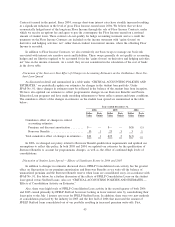

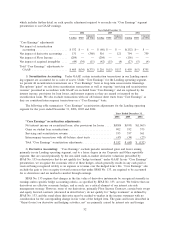

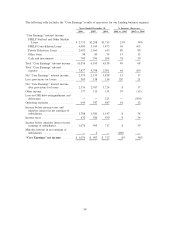

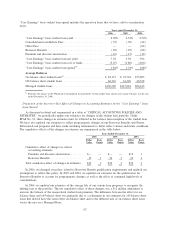

Reclassification of Realized Gains (Losses) on Derivative and Hedging Activities

SFAS No. 133 requires net settlement income/expense on derivatives and realized gains/losses related to

derivative dispositions (collectively referred to as “realized gains (losses) on derivative and hedging activities”)

that do not qualify as hedges under SFAS No. 133 to be recorded in a separate income statement line item

below net interest income. The table below summarizes the realized losses on derivative and hedging activities,

and the associated reclassification on a “Core Earnings” basis for the years ended December 31, 2006, 2005

and 2004.

2006 2005 2004

Years Ended December 31,

Reclassification of realized gains (losses) on derivative and hedging

activities:

Net settlement expense on Floor Income Contracts reclassified to net

interest income .......................................... $ (50) $(259) $ (562)

Net settlement expense on interest rate swaps reclassified to net interest

income ................................................ (59) (123) (88)

Net realized losses on terminated derivative contracts reclassified to

other income ........................................... — (5) (63)

Total reclassifications of realized losses on derivative and hedging

activities .............................................. (109) (387) (713)

Add: Unrealized gains (losses) on derivative and hedging activities,

net

(1)

................................................. (230) 634 1,562

Gains (losses) on derivative and hedging activities, net .............. $(339) $ 247 $ 849

(1)

“Unrealized gains (losses) on derivative and hedging activities, net” is comprised of the following unrealized mark-to-market

gains (losses):

2006 2005 2004

Years Ended December 31,

Floor Income Contracts . . . ................................................ $176 $481 $ 729

Equity forward contracts . . ................................................ (360) 121 759

Basis swaps .......................................................... (58) 40 73

Other . . . ............................................................ 12 (8) 1

Total unrealized gains (losses) on derivative and hedging activities, net . . .................. $(230) $634 $1,562

Unrealized gains and losses on Floor Income Contracts are primarily caused by changes in interest rates.

In general, an increase in interest rates results in an unrealized gain and vice versa. Unrealized gains and

losses on Equity Forward Contracts fluctuate with changes in the Company’s stock price. Unrealized gains and

losses on basis swaps result from changes in the spread between indices, primarily as it relates to Consumer

Price Index (“CPI”) swaps economically hedging debt issuances indexed to CPI.

3) Floor Income: The timing and amount (if any) of Floor Income earned in our Lending operating

segment is uncertain and in excess of expected spreads. Therefore, we exclude such income from “Core

Earnings” when it is not economically hedged. We employ derivatives, primarily Floor Income Contracts and

futures, to economically hedge Floor Income. As discussed above in “Derivative Accounting,” these derivatives

do not qualify as effective accounting hedges, and therefore, under GAAP, they are marked-to-market through

the “gains (losses) on derivative and hedging activities, net” line on the income statement with no offsetting

gain or loss recorded for the economically hedged items. For “Core Earnings,” we reverse the fair value

adjustments on the Floor Income Contracts and futures economically hedging Floor Income and include the

amortization of net premiums received in income.

54