Sallie Mae 2006 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

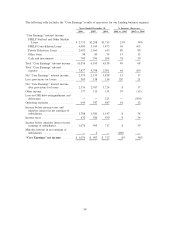

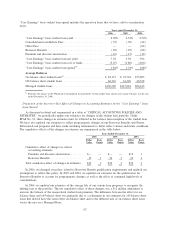

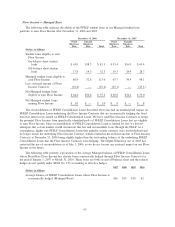

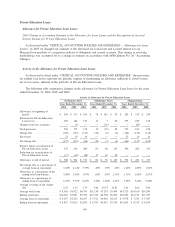

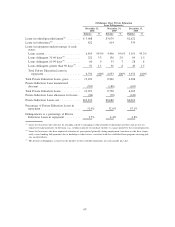

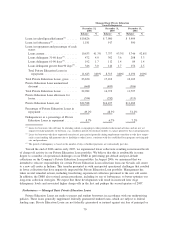

Discussion of “Core Earnings” Basis Student Loan Spread — Effects of Significant Events in 2006 and 2005

In addition to changes in estimates discussed above, FFELP Consolidation Loan activity has the greatest

effect on fluctuations in our premium amortization and Borrower Benefits as we write-off the balance of

unamortized premium and the Borrower Benefit reserve when loans are consolidated away, in accordance with

SFAS No. 91. See below for a further discussion of the effects of FFELP Consolidation Loans on the student

loan spread versus Stafford Loans. See also, “CRITICAL ACCOUNTING POLICIES AND ESTIMATES —

Effects of Consolidation Activity on Estimates,” above.

Also, there were high levels of FFELP Consolidation Loan activity in the second quarter of both 2006

and 2005 caused primarily by FFELP Stafford borrowers locking in lower interest rates by consolidating their

loans prior to the July 1 interest rate reset for FFELP Stafford loans. In addition, there were two new methods

of consolidation practiced by the industry in 2005 and the first half of 2006. First, borrowers were permitted

for the first time to consolidate their loans while still in school. Second, a significant volume of our FFELP

Consolidation Loans was reconsolidated with third party lenders through the FDLP, resulting in an increase in

student loan premium write-offs. Also, the repeal of the Single Holder Rule increased the amount of loans that

consolidated with third parties resulting in increased premium write-offs in the second half of the year.

Consolidation of student loans does benefit the student loan spread to a lesser extent through the write-off of

Borrower Benefits reserves associated with these loans. Both in-school consolidation and reconsolidation with

third party through the FDLP were restricted as of July 1, 2006, through the Higher Education Act of 2005.

While FFELP Consolidation Loan activity remained high in 2006, it was lower than 2005, which contributed

to lower student loan premium amortization in 2006.

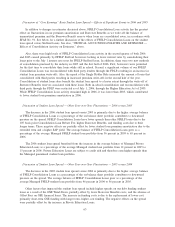

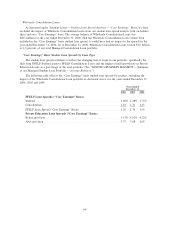

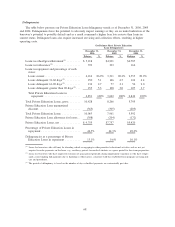

Discussion of Student Loan Spread — Other Year-over-Year Fluctuations — 2006 versus 2005

The decrease in the 2006 student loan spread versus 2005 is primarily due to the higher average balance

of FFELP Consolidation Loans as a percentage of the on-balance sheet portfolio contributes to downward

pressure on the spread. FFELP Consolidation Loans have lower spreads than other FFELP loans due to the

105 basis point Consolidation Loan Rebate Fee, higher Borrower Benefits, and funding costs due to their

longer terms. These negative effects are partially offset by lower student loan premium amortization due to the

extended term and a higher SAP yield. The average balance of FFELP Consolidation Loans grew as a

percentage of the average Managed FFELP student loan portfolio from 56 percent in 2005 to 63 percent in

2006.

The 2006 student loan spread benefited from the increase in the average balance of Managed Private

Education Loans as a percentage of the average Managed student loan portfolio from 12 percent in 2005 to

15 percent in 2006. Private Education Loans are subject to credit risk and therefore earn higher spreads than

the Managed guaranteed student loan portfolio.

Discussion of Student Loan Spread — Other Year-over-Year Fluctuations — 2005 versus 2004

The decrease in the 2005 student loan spread versus 2004 is primarily due to the higher average balance

of FFELP Consolidation Loans as a percentage of the on-balance sheet portfolio contributes to downward

pressure on the spread. The average balance of FFELP Consolidation Loans grew as a percentage of the

average Managed FFELP student loan portfolio from 46 percent in 2004 to 56 percent in 2005.

Other factors that impacted the student loan spread include higher spreads on our debt funding student

loans as a result of the GSE Wind-Down, partially offset by lower Borrower Benefits costs, and the absence of

Offset Fees on GSE financed loans. The increase in funding costs is due to the replacement of lower cost,

primarily short-term GSE funding with longer term, higher cost funding. The negative effects on the spread

were partially offset by the increase in Private Education Loans.

63