Sallie Mae 2006 Annual Report Download - page 210

Download and view the complete annual report

Please find page 210 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215

|

|

Lenders generally receive interest subsidy and special allowance payments within 45 days to 60 days after

submitting the applicable data for any given calendar quarter to the Department of Education. However, there

can be no assurance that payments will, in fact, be received from the Department within that period.

If the loan is not held by an eligible lender in accordance with the requirements of the Higher Education

Act and the applicable guarantee agreement, the loan may lose its federal assistance.

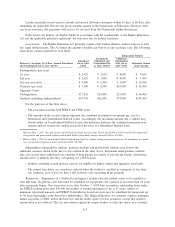

Loan Limits. The Higher Education Act generally requires that lenders disburse student loans in at least

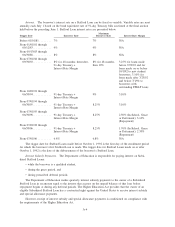

two equal disbursements. The Act limits the amount a student can borrow in any academic year. The following

chart shows current and historic loan limits.

Borrower’s Academic Level Base Amount Subsidized

and Unsubsidized On or After 10/1/93

Subsidized

On or After

1/1/87

All Students

Subsidized and

Unsubsidized On

or After 10/1/93

Additional

Unsubsidized

Only On or

After 7/1/94

Maximum Annual

Total Amount

Independent Students

Undergraduate (per year):

1st year ............................. $ 2,625 $ 2,625

*

$ 4,000 $ 6,625

2nd year ............................ $ 2,625 $ 3,500

*

$ 4,000 $ 7,500

3rd year and above .................... $ 4,000 $ 5,500 $ 5,000

**

$ 10,500

Graduate (per year) .................... $ 7,500 $ 8,500 $10,000

*

$ 18,500

Aggregate Limit:

Undergraduate ........................ $17,250 $23,000 $23,000 $ 46,000

Graduate (including undergraduate) ........ $54,750 $65,500 $73,000 $138,500

For the purposes of the table above:

• The loan limits include both FFELP and FDLP loans.

• The amounts in the second column represent the combined maximum loan amount per year for

Subsidized and Unsubsidized Stafford Loans. Accordingly, the maximum amount that a student may

borrow under an Unsubsidized Stafford Loan is the difference between the combined maximum loan

amount and the amount the student received in the form of a Subsidized Stafford Loan.

*

Effective July 1, 2007, first and second year Stafford loan limits increase from $2,625 and $3,500 to $3,500 and $4,500 respectively,

and graduate and professional student unsubsidized Stafford loan limits increase from $10,000 to $12,000.

**

Effective July 1, 2007 the annual unsubsidized Stafford loan limit for students taking coursework necessary for enrollment in a gradu-

ate or professional program is increased from $5,000 to $7,000.

Independent undergraduate students, graduate students and professional students may borrow the

additional amounts shown in the next to last column in the chart above. Dependent undergraduate students

may also receive these additional loan amounts if their parents are unable to provide the family contribution

amount and it is unlikely that they will qualify for a PLUS Loan.

• Students attending certain medical schools are eligible for higher annual and aggregate loan limits.

• The annual loan limits are sometimes reduced when the student is enrolled in a program of less than

one academic year or has less than a full academic year remaining in his program.

Repayment. Repayment of a Stafford Loan begins 6 months after the student ceases to be enrolled at

least half time. In general, each loan must be scheduled for repayment over a period of not more than 10 years

after repayment begins. New borrowers on or after October 7, 1998 who accumulate outstanding loans under

the FFELP totaling more than $30,000 are entitled to extend repayment for up to 25 years, subject to

minimum repayment amounts and FFELP Consolidation Loan borrowers may be scheduled for repayment up

to 30 years depending on the borrower’s indebtedness. The Higher Education Act currently requires minimum

annual payments of $600, unless the borrower and the lender agree to lower payments, except that negative

amortization is not allowed. The Act and related regulations require lenders to offer the choice of a standard,

A-7