Sallie Mae 2006 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2006 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

2. Significant Accounting Policies (Continued)

The adoption of SFAS No. 156 will not have a material impact on the Company’s financial statements.

Accounting for Certain Hybrid Financial Instruments

In February 2006, the FASB issued SFAS No. 155, “Accounting for Certain Hybrid Financial

Instruments” which amends SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities,”

and SFAS No. 140. This statement will be effective for the Company beginning January 1, 2007.

This statement:

• Requires that all interests in securitized financial assets be evaluated to determine if the interests are

free standing derivatives or if the interests contain an embedded derivative;

• Clarifies which interest-only strips and principal-only strips are exempt from the requirements of

SFAS No. 133;

• Clarifies that the concentrations of credit risk in the form of subordination are not an embedded

derivative; and

• Allows a hybrid financial instrument containing an embedded derivative that would have required

bifurcation under SFAS No. 133 to be measured at fair value as one instrument on a case by case basis;

• Amends SFAS Statement No. 140 to eliminate the prohibition of a qualifying special purpose entity

from holding a derivative financial instrument that pertains to beneficial interests other than another

derivative financial instrument.

In January 2007, the FASB issued SFAS No. 133, “Accounting for Derivative Instruments and Hedging

Activities,” Implementation Issues No. B39, “Embedded Derivatives: Application of Paragraph 13(b) to Call

Options That Are Exercisable Only by the Debtor (Amended)”, and No. B40, “Embedded Derivatives:

Application of Paragraph 13(b) to Securitized Interests in Prepayable Financial Assets”. The guidance clarifies

various aspects of SFAS No. 155 and will require the Company to either (1) separately record embedded

derivatives that may reside in the Company’s Residual Interest and on-balance sheet securitization debt, or

(2) if embedded derivatives exist that require bifurcation, mark-to-market through income changes in the fair

value of the Company’s Residual Interest and on-balance sheet securitization debt in their entirety. This

standard will be prospectively applied in 2007 for new securitizations and would not apply to the Company’s

existing Residual Interest or on-balance sheet securitization debt.

If material embedded derivatives exist within the Residual Interest that require bifurcation, the Company

will most likely elect to carry the entire Residual Interest at fair value with subsequent changes in fair value

recorded in earnings. This could have a material impact on earnings, as prior to the adoption of SFAS No. 155,

changes in the fair value of these Residual Interests would have been recorded through other comprehensive

income (except for impairment which is recorded through income). The Company has concluded, based on its

current securitization deal structures, that its on-balance sheet securitization debt will not be materially

impacted upon the adoption of SFAS No. 155 as potential embedded derivatives will not have a material

value.

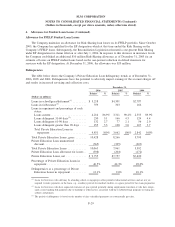

3. Student Loans

The FFELP is subject to comprehensive reauthorization every five years and to frequent statutory and

regulatory changes. The most recent reauthorization was the Higher Education Reconciliation Act of 2005 (the

“Reconciliation Legislation”).

F-24

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)