SunTrust 2012 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

32

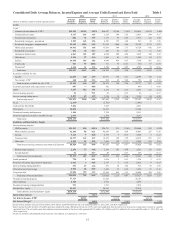

Reporting," to the Consolidated Financial Statements in this Form 10-K for a description of our business segments and a discussion

of the change in our segment reporting structure during 2012. In addition to deposit, credit, and trust and investment services

offered by the Bank, our other subsidiaries provide mortgage banking, asset management, securities brokerage, and capital market

services.

This MD&A is intended to assist readers in their analysis of the accompanying consolidated financial statements and supplemental

financial information. It should be read in conjunction with the Consolidated Financial Statements and Notes in Item 8 of this

Form 10-K. When we refer to “SunTrust,” “the Company,” “we,” “our” and “us” in this narrative, we mean SunTrust Banks, Inc.

and subsidiaries (consolidated). In the MD&A, net interest income, net interest margin, and efficiency ratios are presented on an

FTE basis. The FTE basis adjusts for the tax-favored status of net interest income from certain loans and investments. We believe

this measure to be the preferred industry measurement of net interest income and it enhances comparability of net interest income

arising from taxable and tax-exempt sources. Additionally, we present certain non-U.S. GAAP metrics to assist investors in

understanding management’s view of particular financial measures, as well as, to align presentation of these financial measures

with peers in the industry who may also provide a similar presentation. Reconcilements for all non-U.S. GAAP measures are

provided in Tables 39 and 40.

EXECUTIVE OVERVIEW

Economic and regulatory

Economic indicators generally improved during 2012 after remaining relatively unchanged during 2011. During 2012,

unemployment declined, consumer confidence improved, and the housing markets began to show some signs of improvement,

but remained uneven in their recovery. The unemployment rate, which was just below 9% at December 31, 2011, continued to

decline during 2012, settling at just below 8% at December 31, 2012. Consumer confidence improved moderately during 2012,

as consumer spending increased amidst improving labor market conditions and subdued consumer price inflation. However,

consumer confidence remained depressed overall when compared to pre-recession levels as a result of a continued sluggish

economic recovery in the U.S., continued concerns over the economic health of the European Union, and reports of slowing growth

in other emerging economies. While some actions were taken during 2012 to ease the European sovereign debt crisis, uncertainty

in the direction of the financial markets continues to exist as European consumer confidence continued to decline during the year.

As of December 31, 2012, we had no direct exposure to sovereign debt of European countries experiencing significant economic,

fiscal, and/or political strains. See additional discussion of European debt exposure in "Other Market Risk" in this MD&A. The

U.S. housing market continued to be weak as evidenced by the large inventory of foreclosed or distressed properties, and, while

home prices rose modestly during 2012, home values remained under pressure and many borrowers continued to owe more on

their mortgage than the current market value of their home.

Amidst the somewhat stagnant economic conditions seen during 2012, the Federal Reserve indicated that highly accommodative

monetary policy will remain for a considerable time after the economic recovery strengthens. Accordingly, it anticipates maintaining

key interest rates at exceptionally low levels, at least as long as the unemployment rate remains above 6.5% and its long-term

inflation goals are not met. As a result of employing its monetary policy, the Federal Reserve continues to maintain large portfolios

of U.S. Treasury notes and bonds and agency MBS with plans to continue adding Treasuries and agency MBS to the portfolio in

2013. The Federal Reserve outlook remains for moderate economic growth over coming quarters, a relatively high unemployment

rate, and the expectation of stable longer-term inflation. These monetary policy actions may result in a persistent low interest rate

environment that may adversely affect the interest income we earn on loans and investments.

Regulatory and financial reform efforts continued during 2012, as regulatory agencies proposed and worked to finalize numerous

rules. These rules covered a wide array of regulatory topics, the most significant of which was the Federal Reserve and other U.S.

banking regulators' NPR issued during 2012 related to capital adequacy rules to implement the BCBS's Basel III framework for

financial institutions in the U.S. Much of the NPR was consistent with the BCBS's Basel III framework. However, we have noted

some substantial differences from the original framework. As currently proposed, we believe that our risk-weighted assets would

increase primarily due to increased risk-weightings for residential mortgages, home equity loans, and commercial real estate,

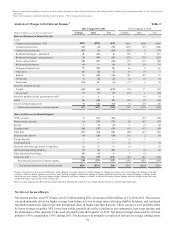

resulting in a decline in our capital ratios. Under current rules (Basel I), our Tier 1 common equity ratio was 10.04% at December

31, 2012. Under the proposed rules, we estimate our current Basel III Tier 1 common ratio, on a fully phased-in basis, would be

approximately 8.2%, which would be in compliance with the proposed requirements. See the "Reconcilement of Non-U.S. GAAP

Measures - Annual" section in this MD&A for a reconciliation of the current Basel I ratio to the proposed Basel III ratio. The

agencies are expected to consider the feedback received during the comment period that ended in October 2012, and draft a final

rule, which could take several quarters to complete. Accordingly, the final rule may differ from the current NPR. Further, the NPR

indicates a phase-in for the new capital rules with the proposed risk-weightings requirement not becoming effective until 2015.

Notwithstanding the uncertainty surrounding the timing and content of the final rule, our current Basel III Tier 1 common ratio

estimate that we calculated using our interpretation of the NPR assumptions does not include the effect of any mitigating actions

we may undertake to offset some of the anticipated impact of the proposed capital changes. We continue to dedicate the appropriate