SunTrust 2012 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

Notes to Consolidated Financial Statements (Continued)

134

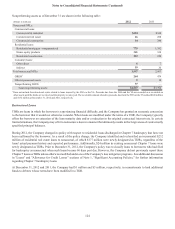

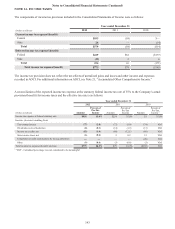

VIE have no recourse to the general credit of the Company, as the liabilities of the CLO are paid only to the extent

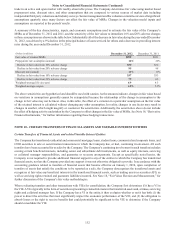

of available cash flows from the CLO’s assets.

For the remaining CLOs, which are also considered to be VIEs, the Company has determined that it is not the primary

beneficiary as it does not have an obligation to absorb losses or the right to receive benefits from the entities that

could potentially be significant to the VIE. The Company's preference share exposure was valued at $3 million as

of December 31, 2012 and $2 million as of December 31, 2011. The Company’s only remaining involvement with

these VIEs is through its collateral manager role. The Company receives fees for managing the assets of these vehicles;

these fees are considered adequate compensation and are commensurate with the level of effort required to provide

such services. The fees received by the Company from these entities are recorded as trust and investment management

income in the Consolidated Statements of Income. Senior fees earned by the Company are generally not considered

at risk; however, subordinate fees earned by the Company are subject to the availability of cash flows and to the

priority of payments. At December 31, 2012 and 2011, the Company’s Consolidated Balance Sheets did not include

$1.8 billion and $2.0 billion, respectively, of estimated assets and $1.7 billion and $1.9 billion, respectively, of

estimated liabilities. The Company is not obligated to provide any support to these entities, nor has it previously

provided support to these entities. No events occurred during the year ended December 31, 2012, that would change

the Company’s previous conclusion that it is not the primary beneficiary of any of these securitization entities.

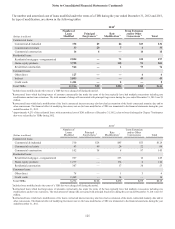

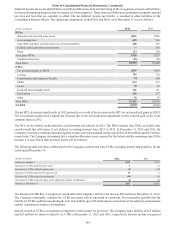

Student Loans

During 2006, the Company completed a securitization of government-guaranteed student loans through a transfer of

loans to a securitization SPE, which previously qualified as a QSPE, and retained the related residual interest in the

SPE. The Company concluded that this securitization of government-guaranteed student loans (the “Student Loan

entity”) should be consolidated. At December 31, 2012 and 2011, the Company’s Consolidated Balance Sheets

reflected $384 million and $438 million, respectively, of assets held by the Student Loan entity and $380 million and

$433 million, respectively, of debt issued by the Student Loan entity.

Payments from the assets in the SPE must first be used to settle the obligations of the SPE, with any remaining

payments remitted to the Company as the owner of the residual interest. To the extent that losses occur on the SPE’s

assets, the SPE has recourse to the federal government as the guarantor up to a maximum guarantee amount of 97%.

Losses in excess of the government guarantee reduce the amount of available cash payable to the Company as the

owner of the residual interest. To the extent that losses result from a breach of the master servicer’s servicing

responsibilities, the SPE has recourse to the Company; the SPE may require the Company to repurchase the loan

from the SPE at par value. If the breach was caused by the subservicer, the Company has recourse to seek

reimbursement from the subservicer up to the guaranteed amount. The Company’s maximum exposure to loss related

to the SPE is represented by the potential losses resulting from a breach of servicing responsibilities. To date, all loss

claims filed with the guarantor that have been denied due to servicing errors have either been cured or reimbursement

has been provided to the Company by the subservicer.

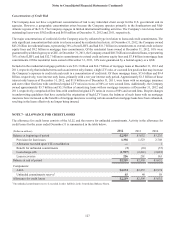

CDO Securities

The Company has transferred bank trust preferred securities in securitization transactions. The Company is not

obligated to provide any support to these entities and its maximum exposure to loss at December 31, 2012 and 2011,

includes current senior interests held in trading securities, which have fair values of $52 million and $43 million,

respectively.

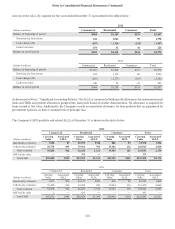

As discussed further in Note 18, "Fair Value Election and Measurement," the Company values these interests by

constructing a pricing matrix of values based on a range of overcollateralization levels that are derived from discussions

with the dealer community along with limited trade data. The price derived from the matrix is then adjusted for each

security based on deal specific factors such as the percentage of collateral that is considered to be at heightened risk

for future deferral or default, and collateral specific prepayment expectations, among other factors. The underlying

collateral of the VIEs is highly concentrated, and as a result, the default or deferral of certain large exposures adversely

impacts the value of the interests. From a sensitivity analysis of the overcollateralization, the Company estimates

that if each of the VIEs in which the Company holds retained positions experienced one to three additional large

deferrals or defaults of an underlying collateral obligation, the fair value of the retained ARS would decline $7 million

to $19 million, respectively.

At December 31, 2012 and 2011, the total assets of the trust preferred CDO entities in which the Company has

remaining exposure to loss were $1.2 billion. The Company determined that it was not the primary beneficiary of

any of these VIEs as the Company lacks the power to direct the significant activities of any of the VIEs. No events

occurred during the year ended December 31, 2012 , that changed either the Company’s sale accounting or the

Company’s conclusions that it is not the primary beneficiary of these VIEs.