SunTrust 2012 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

Notes to Consolidated Financial Statements (Continued)

112

The Company applies the following fair value hierarchy:

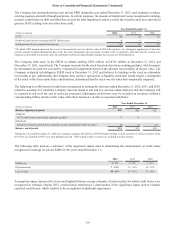

• Level 1 – Assets or liabilities valued using unadjusted quoted prices in active markets for identical assets or liabilities

that the Company can access at the measurement date, such as publicly-traded instruments or futures contracts.

• Level 2 – Assets and liabilities valued based on observable market data for similar instruments.

• Level 3 – Assets or liabilities for which significant valuation assumptions are not readily observable in the market;

instruments valued based on the best available data, some of which is internally developed, and considers risk

premiums that a market participant would require.

To determine the fair value measurement for assets and liabilities required or permitted to be recorded at fair value, the

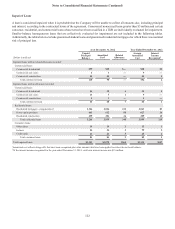

Company considers the principal or most advantageous market in which it would transact and considers assumptions that

market participants would use when pricing the asset or liability. If available, the Company looks to active and observable

markets to price identical assets or liabilities. If identical assets and liabilities are not traded in active markets, the Company

looks to market observable data for similar assets and liabilities. Nevertheless, the Company uses alternative valuation

techniques to derive a fair value measurement for those assets and liabilities that are either not actively traded in observable

markets or for which market observable inputs are not available. For additional information on the Company’s valuation of

its assets and liabilities held at fair value, see Note 18, “Fair Value Election and Measurement.”

Accounting Policies Recently Adopted and Pending Accounting Pronouncements

In April 2011, the FASB issued ASU 2011-03, “Transfers and Servicing (Topic 860): Reconsideration of Effective Control

for Repurchase Agreements.” A repurchase agreement is a transaction in which a company sells financial instruments to a

buyer, typically in exchange for cash, and simultaneously enters into an agreement to repurchase the same or substantially

the same financial instruments from the buyer at a stated price plus accrued interest at a future date. The determination of

whether the transaction is accounted for as a sale or a collateralized financing is determined by assessing whether the seller

retains effective control of the financial instrument. The ASU changes the assessment of effective control by removing the

criterion that requires the seller to have the ability to repurchase or redeem financial assets with substantially the same terms,

even in the event of default by the buyer and the collateral maintenance implementation guidance related to that criterion. The

Company applied the new guidance to repurchase agreements entered into or amended after January 1, 2012. The adoption

of the ASU did not have a significant impact on the Company’s financial position, results of operations, or EPS.

In May 2011, the FASB issued ASU 2011-04, “Fair Value Measurement (Topic 820): Amendments to Achieve Common Fair

Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.” The primary purpose of the ASU was to conform

the language in the fair value measurements guidance in U.S. GAAP and IFRS. The ASU also clarified how to apply existing

fair value measurement and disclosure requirements. Further, the ASU required additional disclosures about transfers between

level 1 and 2 of the fair value hierarchy, quantitative information for level 3 inputs, and the level of the fair value measurement

hierarchy for items that are not measured at fair value in the statement of financial position but for which the fair value is

required to be disclosed. The ASU was effective for the interim reporting period ending March 31, 2012. The Company adopted

the standard as of January 1, 2012, and the required disclosures are included in Note 18, “Fair Value Election and Measurement.”

The adoption did not impact the Company’s financial position, results of operations, or EPS.

In June 2011, the FASB issued ASU 2011-05, “Comprehensive Income (Topic 220): Presentation of Comprehensive Income.”

The ASU requires presentation of the components of comprehensive income in either a continuous statement of comprehensive

income or two separate but consecutive statements. The update does not change the items presented in OCI and does not affect

the calculation or reporting of EPS. The guidance, with the exception of reclassification adjustments, was effective on January 1,

2012, and must be applied retrospectively for all periods presented. The Company adopted the standard as of January 1, 2012,

and the required disclosures are included in the Consolidated Statements of Comprehensive Income. The adoption did not

impact the Company’s financial position, results of operations, or EPS.

In February 2013, the FASB issued ASU 2013-02, "Comprehensive Income (Topic 220): Reporting of Amounts Reclassified

Out of Accumulated Other Comprehensive Income" which provides disclosure guidance on amounts reclassified out of OCI

by component. The ASU is effective for fiscal periods beginning after December 15, 2012. Since the ASU only impacts

financial statement disclosures, its adoption will not impact the Company's financial position, results of operations, or EPS.

In September 2011, the FASB issued ASU 2011-08, “Intangibles-Goodwill and Other (Topic 350): Testing Goodwill for

Impairment.” The ASU amends interim and annual goodwill impairment testing requirements such that an entity is not required

to calculate the fair value of a reporting unit unless the entity determines that it is more likely than not that the fair value of a

reporting unit is less than its carrying amount. The guidance was effective for annual and interim goodwill impairment tests