SunTrust 2012 Annual Report Download - page 192

Download and view the complete annual report

Please find page 192 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

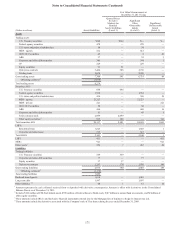

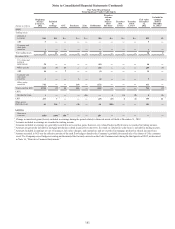

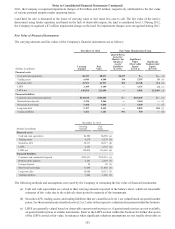

Notes to Consolidated Financial Statements (Continued)

176

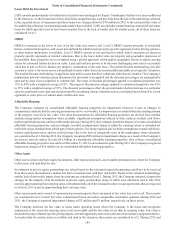

with the issuer at par and cannot be traded in the market; as such, no significant observable market data for these

instruments is available.

Commercial paper

From time to time, the Company trades third party CP that is generally short-term in nature (less than 30 days) and

highly rated. The Company estimates the fair value of this CP based on observable pricing from executed trades of

similar instruments; thus, CP is classified as level 2.

Equity securities

Level 3 equity securities classified as securities AFS include FHLB stock and Federal Reserve Bank stock, which

are redeemable with the issuer at cost and cannot be traded in the market. As such, no significant observable market

data for these instruments is available. The Company accounts for the stock based on industry guidance that requires

these investments be carried at cost and evaluated for impairment based on the ultimate recovery of cost.

Derivative contracts (trading assets or trading liabilities)

With the exception of certain instruments discussed under "other assets/liabilities, net" that qualify as derivative

instruments, the Company’s derivative instruments are level 1 or 2 instruments. Level 1 derivative contracts generally

include exchange-traded futures or option contracts for which pricing is readily available. See Note 16, “Derivative

Financial Instruments,” for additional information on the Company’s derivative contracts.

The Company’s level 2 instruments are predominantly standard OTC swaps, options, and forwards, with underlying

market variables of interest rates, foreign exchange, equity, and credit. Because fair values for OTC contracts are not

readily available, the Company estimates fair values using internal, but standard, valuation models that incorporate

market-observable inputs. The valuation model is driven by the type of contract: for option-based products, the

Company uses an appropriate option pricing model, such as Black-Scholes; for forward-based products, the

Company’s valuation methodology is generally a discounted cash flow approach. The primary drivers of the fair

values of derivative instruments are the underlying variables, such as interest rates, exchange rates, equity, or credit.

As such, the Company uses market-based assumptions for all of its significant inputs, such as interest rate yield

curves, quoted exchange rates and spot prices, market implied volatilities, and credit curves.

Derivative instruments are primarily transacted in the institutional dealer market and priced with observable market

assumptions at a mid-market valuation point, with appropriate valuation adjustments for liquidity and credit risk.

For purposes of valuation adjustments to its derivative positions, the Company has evaluated liquidity premiums that

may be demanded by market participants, as well as the credit risk of its counterparties and its own credit. The

Company has considered factors such as the likelihood of default by itself and its counterparties, its net exposures,

and remaining maturities in determining the appropriate fair value adjustments to record. Generally, the expected

loss of each counterparty is estimated using the Company's proprietary internal risk rating system. The risk rating

system utilizes counterparty-specific probabilities of default and LGD estimates to derive the expected loss. For

counterparties that are rated by national rating agencies, those ratings are also considered in estimating the credit

risk. In addition, counterparty exposure is evaluated by netting positions that are subject to master netting

arrangements, as well as considering the amount of marketable collateral securing the position. Specifically approved

counterparties and exposure limits are defined. Creditworthiness of the approved counterparties is regularly reviewed

and appropriate business action is taken to adjust the exposure to certain counterparties, as necessary. This approach

used to estimate exposures to counterparties is also used by the Company to estimate its own credit risk on derivative

liability positions.

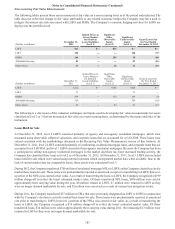

During the year ended December 31, 2012, the Company terminated the Agreements that were entered into in 2008

related to its Coke common stock. The Agreements were considered level 3 instruments due to the unobservability

of the volatility assumption used to value these instruments. Volatility was a significant assumption used in the

valuation of the Agreements and was unobservable due to the unusually large size of the trade and the long tenor

until settlement, which was originally 6.5 years and 7 years from the effective date. Because of this significant

unobservable assumption, the observable and active options market on Coke did not provide for any identical or

similar instruments. Prior to termination of the Agreements, the Company received estimated market values from a

market participant who is knowledgeable about Coke equity derivatives and was active in the market. Based on

inquiries of the market participant as to their procedures, as well as the Company's own valuation assessment

procedures, the Company satisfied itself that the market participant was using methodologies and assumptions that

other market participants would use in estimating the fair value of the Agreements. At December 31, 2011, the

Agreements’ combined fair value was a liability of $189 million.

See Note 16, “Derivative Financial Instruments,” for additional information on the Company's derivative contracts.