SunTrust 2012 Annual Report Download - page 184

Download and view the complete annual report

Please find page 184 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

Notes to Consolidated Financial Statements (Continued)

168

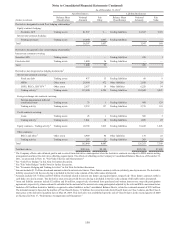

Public Deposits

The Company holds public deposits from various states in which it does business. Individual state laws require banks to

collateralize public deposits, typically as a percentage of their public deposit balance in excess of FDIC insurance and may

also require a cross-guarantee among all banks holding public deposits of the individual state. The amount of collateral

required varies by state and may also vary by institution within each state, depending on the individual state's risk assessment

of depository institutions. Certain of the states in which the Company holds public deposits use a pooled collateral method,

whereby in the event of default of a bank holding public deposits, the collateral of the defaulting bank is liquidated to the

extent necessary to recover the loss of public deposits of the defaulting bank. To the extent the collateral is insufficient,

the remaining public deposit balances of the defaulting bank are recovered through an assessment of the other banks holding

public deposits in that state. The maximum potential amount of future payments the Company could be required to make

is dependent on a variety of factors, including the amount of public funds held by banks in the states in which the Company

also holds public deposits and the amount of collateral coverage associated with any defaulting bank. Individual states

appear to be monitoring this risk relative to the current economic environment and evaluating collateral requirements;

therefore, the likelihood that the Company would have to perform under this guarantee is dependent on whether any banks

holding public funds default as well as the adequacy of collateral coverage.

Other

In the normal course of business, the Company enters into indemnification agreements and provides standard representations

and warranties in connection with numerous transactions. These transactions include those arising from securitization

activities, underwriting agreements, merger and acquisition agreements, loan sales, contractual commitments, payment

processing, sponsorship agreements, and various other business transactions or arrangements. The extent of the Company’ s

obligations under these indemnification agreements depends upon the occurrence of future events; therefore, the Company’s

potential future liability under these arrangements is not determinable.

STIS and STRH, broker-dealer affiliates of SunTrust, use a common third-party clearing broker to clear and execute their

customers' securities transactions and to hold customer accounts. Under their respective agreements, STIS and STRH agree

to indemnify the clearing broker for losses that result from a customer's failure to fulfill its contractual obligations. As the

clearing broker's rights to charge STIS and STRH have no maximum amount, the Company believes that the maximum

potential obligation cannot be estimated. However, to mitigate exposure, the affiliate may seek recourse from the customer

through cash or securities held in the defaulting customers' account. For the years ended December 31, 2012, 2011, and

2010, STIS and STRH experienced minimal net losses as a result of the indemnity. The clearing agreements expire in May

2015 for both STIS and STRH.

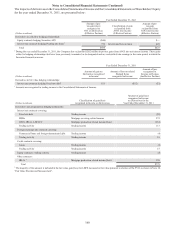

NOTE 18 - FAIR VALUE ELECTION AND MEASUREMENT

The Company carries certain assets and liabilities at fair value on a recurring basis and appropriately classifies them as level

1, 2, or 3 within the fair value hierarchy. The Company’s recurring fair value measurements are based on a requirement to

carry such assets and liabilities at fair value or the Company’s election to carry certain financial assets and liabilities at fair

value. Assets and liabilities that are required to be carried at fair value on a recurring basis include trading securities, securities

AFS, and derivative financial instruments. Assets and liabilities that the Company has elected to carry at fair value on a

recurring basis include certain LHFS and LHFI, MSRs, certain brokered time deposits, and certain issuances of fixed rate

debt.

In certain circumstances, fair value enables a company to more accurately align its financial performance with the economic

value of actively traded or hedged assets or liabilities. Fair value also enables a company to mitigate the non-economic earnings

volatility caused from financial assets and liabilities being carried at different bases of accounting, as well as, to more accurately

portray the active and dynamic management of a company’s balance sheet.

Depending on the nature of the asset or liability, the Company uses various valuation techniques and assumptions when

estimating fair value. The assumptions used to estimate the value of an instrument have varying degrees of impact to the

overall fair value of the asset or liability. This process involves the gathering of multiple sources of information, including

broker quotes, values provided by pricing services, trading activity in other similar securities, market indices, pricing matrices

along with employing various modeling techniques, such as discounted cash flow analyses, in arriving at the best estimate of

fair value. Any model used to produce material financial reporting information is required to have a satisfactory independent