SunTrust 2012 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

91

Year Ended December 31, 2011 vs. 2010

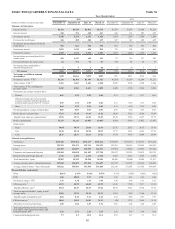

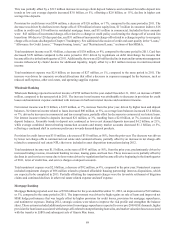

Consumer Banking and Private Wealth Management

Consumer Banking and Private Wealth Management reported net income of $243 million for the year ended December 31,

2011, an increase of $128 million compared to the same period in 2010. The increase in net income was attributable to a

decrease in provision for credit losses combined with an increase in net interest income, and a decrease in noninterest expense,

partially offset by a decrease in noninterest income.

Net interest income was $2.5 billion, an increase of $53 million, or 2%, compared to the same period in 2010. The increase

was driven by higher average loan and deposit balances and higher loan spreads, partially offset by the impact of lower deposit

spreads.

Net interest income related to loans increased $69 million, or 7%, compared to prior year driven by a $2.2 billion, or 6%,

increase in average loan balances and a 3 basis point increase in loan spreads. The increase in average loans was driven by

organic indirect auto loan production, by the acquisition of $1.7 billion of consumer auto loans in the third and fourth quarters

of 2010, and the purchase of $1.6 billion of guaranteed student loans during 2011. Partially offsetting the increases were

decreases in home equity lines and residential mortgages.

Net interest income related to client deposits was $1.7 billion, a decrease of $30 million, or 2% compared to the same period

in 2010. The decrease in net interest income was driven by a 10 basis point decline in deposit spreads and a decrease in funding

rates for other liabilities. This was partially offset by a $2.1 billion, or 3%, increase in average client deposit balances and

continued favorable deposit mix trends as low cost average deposits increased $5.4 billion, or 10%, and higher cost average

time deposits declined by $3.3 billion, or 16%.

Provision for credit losses was $722 million, a decrease of $169 million, or 19%, compared to the same period in 2010. The

decrease was driven by declines in net charge-offs of: $95 million in equity lines, $34 million in residential mortgage loans,

and $32 million in credit card.

Total noninterest income was $1.5 billion, a decrease of $32 million, or 2%, compared to the same period in 2010. Service

charges on deposits decreased $71 million, or 16%, driven by lower NSF/overdraft fees resulting from Regulation E changes

that became effective in 2010. Other income decreased predominantly due to a gain from the sale of the RidgeWorth Money

Market Fund business in 2010. These decreases were partially offset by increased trust and investment management income

due to higher revenue from the RidgeWorth mutual fund complex, market valuations on managed equity assets, and retail

investment income, which was driven by increased recurring brokerage revenue and annuity income.

Total noninterest expense was $2.9 billion, a decrease of $14 million, or 0.5%, compared to the same period in 2010. The

decrease was predominantly driven by lower corporate overhead allocations and outside processing expense, partially offset

by an increase in employee compensation and operations costs associated with revenue growth.

Wholesale Banking

Wholesale Banking reported net income of $384 million for the year ended December 31, 2011, an increase of $104 million,

or 37%, compared to the same period in 2010. The increase in net income was attributable to decreases in provision for credit

losses and an increase in net interest income, partially offset by increased noninterest expense and decreased noninterest

income.

Net interest income was $1.7 billion, a $166 million, or 10%, increase from the prior year, driven by higher loan and deposit

balances. Net interest income related to loans increased $103 million, or 11%, driven by higher spreads and to a lesser extent

increases in commercial and tax-exempt loans, partially offset by decreases in commercial real estate and other customer

loans. Net interest income related to deposits increased $37 million, or 5%, resulting from a $3.4 billion, or 9%, increase in

client deposit balances. Favorable trends in deposit mix continued as lower-cost demand deposits increased $3.9 billion, or

24%, while average combined interest-bearing transaction accounts and money market accounts also increased $182 million,

or 0.9%, reflecting a shift in customer preference towards demand deposit products. The increases were partially offset by

decreased balances in time deposits from prior year by $647 million, or 22%.

Provision for credit losses was $625 million, a decrease of $152 million, or 20%, from the prior year. The decrease was driven

by lower net charge-offs in commercial loans, commercial real estate loans, leasing, and residential mortgages.

Total noninterest income was $1.4 billion, a decrease of $40 million, or 3%, from the prior year, predominantly driven by

decreased trading revenue, letters of credit fees, card services revenue due to lower rates driven by regulations that became