SunTrust 2012 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2012 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

22

and may acquire banks and other financial institutions. This may significantly change the competitive environment in which

we conduct business. Some of our competitors have greater financial resources and/or face fewer regulatory constraints. As

a result of these various sources of competition, we could lose business to competitors or be forced to price products and

services on less advantageous terms to retain or attract clients, either of which would adversely affect our profitability.

Maintaining or increasing market share depends on market acceptance and regulatory approval of new products and

services.

Our success depends, in part, on our ability to adapt products and services to evolving industry standards. There is increasing

pressure to provide products and services at lower prices. This can reduce net interest income and noninterest income from

fee-based products and services. In addition, the widespread adoption of new technologies could require us to make substantial

capital expenditures to modify or adapt existing products and services or develop new products and services. We may not be

successful in introducing new products and services in response to industry trends or developments in technology, or those

new products may not achieve market acceptance. As a result, we could lose business, be forced to price products and services

on less advantageous terms to retain or attract clients, or be subject to cost increases, any of which would adversely affect our

profitability.

We might not pay dividends on your common stock.

Holders of our common stock are only entitled to receive such dividends as our Board may declare out of funds legally available

for such payments. Although we have historically declared cash dividends on our common stock, we are not required to do

so.

Further, in February 2009, the Federal Reserve required bank holding companies to substantially reduce or eliminate dividends.

Since that time, the Federal Reserve has indicated that increased capital distributions would generally not be considered

prudent in the absence of a well-developed capital plan and a capital position that would remain strong even under adverse

conditions. As a result, we expect that any substantial increase in our dividend will require the approval of the Federal Reserve.

Refer to the discussion under the caption "We are subject to capital adequacy and liquidity guidelines and, if we fail to meet

these guidelines, our financial condition would be adversely affected," above.

Additionally, our obligations under the warrant agreements (that we entered into with the U.S. Treasury as part of the CPP)

will increase to the extent that we pay dividends prior to December 31, 2018 exceeding $0.54 per share per quarter, which

was the amount of dividends we paid when we first participated in the CPP. Specifically, the exercise price and the number

of shares to be issued upon exercise of the warrants will be adjusted proportionately (that is, adversely to us) as specified in

a formula contained in the warrant agreements.

Our ability to receive dividends from our subsidiaries could affect our liquidity and ability to pay dividends.

We are a separate and distinct legal entity from our subsidiaries, including the Bank. We receive substantially all of our revenue

from dividends from our subsidiaries. These dividends are the principal source of funds to pay dividends on our common

stock and interest and principal on our debt. Various federal and/or state laws and regulations limit the amount of dividends

that our Bank and certain of our nonbank subsidiaries may pay us. Also, our right to participate in a distribution of assets upon

a subsidiary's liquidation or reorganization is subject to the prior claims of the subsidiary's creditors. Limitations on our ability

to receive dividends from our subsidiaries could have a material adverse effect on our liquidity and on our ability to pay

dividends on common stock. Additionally, if our subsidiaries' earnings are not sufficient to make dividend payments to us

while maintaining adequate capital levels, we may not be able to make dividend payments to our common stockholders.

Disruptions in our ability to access global capital markets may adversely affect our capital resources and liquidity.

In managing our consolidated balance sheet, we depend on access to global capital markets to provide us with sufficient capital

resources and liquidity to meet our commitments and business needs, and to accommodate the transaction and cash management

needs of our clients. Other sources of contingent funding available to us includes inter-bank borrowings, repurchase agreements,

FHLB capacity, and borrowings from the Federal Reserve discount window. Any occurrence that may limit our access to the

capital markets, such as a decline in the confidence of debt investors, our depositors or counterparties participating in the

capital markets, or a downgrade of our debt rating, may adversely affect our capital costs and our ability to raise capital and,

in turn, our liquidity.

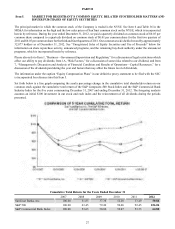

Any reduction in our credit rating could increase the cost of our funding from the capital markets.

Our issuer ratings are rated investment grade by the major rating agencies. There were no changes to our primary credit ratings

during 2012. On February 27, 2012, Fitch affirmed our senior long- and short-term credit ratings and revised its outlook on

our ratings from “Positive” to “Stable”. On December 10, 2012, S&P also affirmed our senior long- and short-term credit

ratings; however, its outlook on our ratings was upgraded from “Stable” to “Positive”. Our credit ratings also remain on

“Stable” outlook with Moody's and DBRS. Additional downgrades are possible, although not anticipated, given the “Stable”

or "Positive" outlook from all four major rating agencies.