PNC Bank 2009 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2009 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Although the allowance declined as a percentage of

nonperforming loans at December 31, 2009 as compared with

December 31, 2008, coverage is considered adequate given

the mix of the loan portfolio. The majority of the commercial

portfolio is secured by collateral, including loans to asset-

based lending customers that continue to show demonstrably

lower loss given default. Further, the large high investment

grade portion of the loan portfolio has performed well and has

not been subject to significant deterioration.

The allowance for loan and lease losses is significantly lower

than it would have been otherwise due to the accounting

treatment for purchased impaired loans. This treatment also

results in a lower ratio of allowance for loan and lease losses

to total loans. Loan loss reserves on the purchased impaired

loans were not carried over on the date of acquisition. In

addition, these loans were recorded net of $9.2 billion of fair

value marks as of December 31, 2008. As a result, the ratio of

allowance for loan and lease losses to total loans is lower than

it would be otherwise.

In addition to the allowance for loan and lease losses, we

maintain an allowance for unfunded loan commitments and

letters of credit. We report this allowance as a liability on our

Consolidated Balance Sheet. We determine this amount using

estimates of the probability of the ultimate funding and losses

related to those credit exposures. This methodology is similar

to the one we use for determining the adequacy of our

allowance for loan and lease losses.

We refer you to Note 5 Asset Quality and Note 6 Purchased

Impaired Loans Related to National City in the Notes To

Consolidated Financial Statements in Item 8 of this Report

regarding changes in the allowance for loan and lease losses

and in the allowance for unfunded loan commitments and

letters of credit. Also see the Allocation Of Allowance For

Loan And Lease Losses table in the Statistical Information

(Unaudited) section of Item 8 of this Report for additional

information included herein by reference.

We establish specific allowances for loans considered

impaired using a method prescribed by GAAP. All impaired

loans except leases and large groups of smaller-balance

homogeneous loans which may include but are not limited to

credit card, residential mortgage, and consumer installment

loans are subject to individual analysis. Specific allowances

for individual loans are determined by our Special Asset

Committee based on an analysis of the present value of

expected future cash flows from the loans discounted at their

effective interest rate, observable market price, or the fair

value of the underlying collateral.

Allocations to commercial and commercial real estate loans

(pool reserve methodology) are assigned to pools of loans as

defined by our business structure and are based on internal

probability of default and loss given default credit risk ratings.

Key elements of the pool reserve methodology include:

• Probability of default (PD), which is primarily based

on historical default analyses and is derived from the

borrower’s internal PD credit risk rating;

• Exposure at default (EAD), which is derived from

historical default data; and

• Loss given default (LGD), which is based on

historical loss data, collateral value and other

structural factors that may affect our ultimate ability

to collect on the loan and is derived from the loan’s

internal LGD credit risk rating.

Our pool reserve methodology is sensitive to changes in key

risk parameters such as PDs, LGDs and EADs. In general, a

given change in any of the major risk parameters will have a

corresponding change in the pool reserve allocations for

non-impaired commercial loans. Our commercial loans are the

largest category of credits and are most sensitive to changes in

the key risk parameters and pool reserve loss rates. To

illustrate, if we increase the pool reserve loss rates by 5% for

all categories of non-impaired commercial loans, then the

aggregate of the allowance for loan and lease losses and

allowance for unfunded loan commitments and letters of

credit would increase by $104 million. Additionally, other

factors such as the rate of migration in the severity of problem

loans will contribute to the final pool reserve allocations.

We make consumer (including residential mortgage) loan

reserve allocations within our business structure by consumer

product line based on historical loss experience. We compute

the allocation loss rates using the roll-rate, historical loss or

other appropriate loss calculation methodologies.

We expect to see credit cost improvements in line with the

pace of economic recovery in 2010.

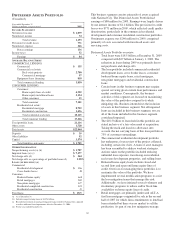

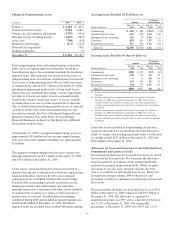

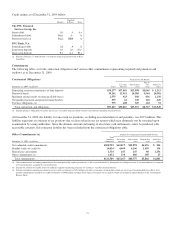

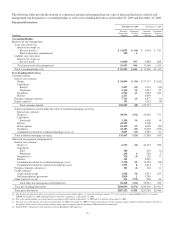

Charge-Offs And Recoveries

Year ended December 31

Dollars in millions Charge-offs Recoveries

Net

Charge-offs

Percent of

Average

Loans

2009

Commercial $1,276 $181 $1,095 1.79%

Commercial real

estate 510 38 472 1.91

Equipment lease

financing 149 27 122 1.97

Consumer 961 105 856 1.63

Residential real

estate 259 93 166 .79

Total $3,155 $444 $2,711 1.64

2008

Commercial $ 301 $ 53 $ 248 .79%

Commercial real

estate 165 10 155 1.65

Equipment lease

financing 3 1 2 .08

Consumer 143 15 128 .62

Residential real

estate 6 6 .07

Total $ 618 $ 79 $ 539 .74

69