PNC Bank 2009 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2009 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

The long-term investment strategy for pension plan assets is

to:

• Meet present and future benefit obligations to all

participants and beneficiaries,

• Cover reasonable expenses incurred to provide such

benefits, including expenses incurred in the

administration of the Trust and the Plan,

• Provide sufficient liquidity to meet benefit and

expense payment requirements on a timely basis, and

• Provide a total return that, over the long term,

maximizes the ratio of trust assets to liabilities by

maximizing investment return, at an appropriate level

of risk.

The Plan’s specific investment objective is to meet or exceed

the investment policy benchmark over the long term. The

investment policy benchmark compares actual performance to

a weighted market index, and measures the contribution of

active investment management and policy implementation.

This investment objective is expected to be achieved over the

long term (one or more market cycles) and is measured over

rolling five-year periods. Total return calculations are time-

weighted and are net of investment-related fees and expenses.

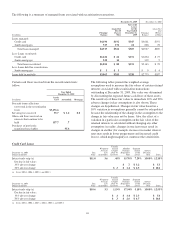

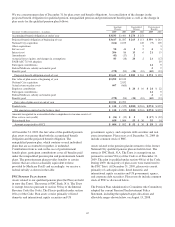

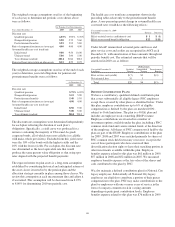

The asset strategy allocations for the Trust at the end of 2009

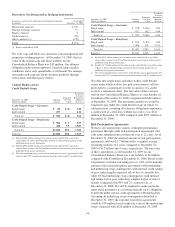

and 2008, and the target allocation range, by asset category,

including National City assets, are as follows:

Target

Allocation

Range

Percentage of Plan Assets

by Strategy at

December 31

PNC Pension Plan 2009 2008

Asset Category

Domestic Equity 32-38% 39% 34%

International Equity 17-23% 18% 12%

Private Equity 0-8% 2% 2%

Total Equity 49-69% 59% 48%

Domestic Fixed Income 23-28% 29% 17%

High Yield Fixed Income 9-11% 6% 3%

Total Fixed Income 32-39% 35% 20%

Real estate 4-6% 5% 2%

Other 0-5% 1% 30%

Total 100% 100%

The asset category represents the allocation of Plan assets in

accordance with the investment objective of each of the Plan’s

investment managers. Certain domestic equity investment

managers utilize derivatives and fixed income securities as

described in their Investment Management Agreements to

achieve their investment objective under the Investment

Policy Statement. Other investment managers may invest in

eligible securities outside of their assigned asset category to

meet their investment objectives. The actual percentage of the

fair value of total plan assets held as of December 31, 2009 for

equity securities, fixed income securities, real estate and all

other assets are 53%, 33%, 5%, and 9%, respectively.

In addition to the use of derivatives, 2008 actual asset

allocations vary from the PNC target allocation in several

categories due to the incorporation of the National City

investments. As of December 31, 2008, this plan had a

temporary large cash and cash equivalents balance due to a

contribution of $850 million made by National City to the

plan on December 30, 2008 which had not yet been fully

invested. During 2009, the majority of plan assets were

transferred to the PNC Trust and invested in accordance with

the current PNC Investment Policy Statement.

At December 31, 2008, equity securities included $9 million

of National City common stock, representing 5,048,833 shares

at a closing price of $1.81. In conjunction with PNC’s

acquisition of National City, these shares were exchanged into

197,914 shares of PNC common stock.

We believe that, over the long term, asset allocation is the

single greatest determinant of risk. Asset allocation will

deviate from the target percentages due to market movement,

cash flows, and investment manager performance. Material

deviations from the asset allocation targets can alter the

expected return and risk of the Trust. On the other hand,

frequent rebalancing to the asset allocation targets may result

in significant transaction costs, which can impair the Trust’s

ability to meet its investment objective. Accordingly, the Trust

portfolio is periodically rebalanced to maintain asset

allocation within the target ranges described above.

In addition to being diversified across asset classes, the Trust

is diversified within each asset class. Secondary

diversification provides a reasonable basis for the expectation

that no single security or class of securities will have a

disproportionate impact on the total risk and return of the

Trust.

The Committee selects investment managers for the Trust

based on the contributions that their respective investment

styles and processes are expected to make to the investment

performance of the overall portfolio. The managers’

Investment Objectives and Guidelines, which are a part of

each manager’s Investment Management Agreement,

document performance expectations and each manager’s role

in the portfolio. The Committee uses the Investment

Objectives and Guidelines to establish, guide, control and

measure the strategy and performance for each manager.

The purpose of investment manager guidelines is to:

• Establish the investment objective and performance

standards for each manager,

• Provide the manager with the capability to evaluate

the risks of all financial instruments or other assets in

which the manager’s account is invested, and

• Prevent the manager from exposing its account to

excessive levels of risk, undesired or inappropriate

risk, or disproportionate concentration of risk.

138