MetLife 2009 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

• Foreign Currency Risk — The Company uses currency swaps and forwards to hedge foreign currency risk. These hedges primarily

swap foreign currency denominated bonds, investments in foreign subsidiaries or equity exposures to US dollars.

• General ALM Hedging Strategies — In the ordinary course of managing the Company’s asset/liability risks, the Company uses interest

rate futures, interest rate swaps, interest rate caps, interest rate floors and inflation swaps. These hedges are designed to reduce

interest rate risk or inflation risk related to the existing assets or liabilities or related to expected future cash flows.

Risk Measurement: Sensitivity Analysis

The Company measures market risk related to its market sensitive assets and liabilities based on changes in interest rates, equity prices

and foreign currency exchange rates utilizing a sensitivity analysis. This analysis estimates the potential changes in estimated fair value based

on a hypothetical 10% change (increase or decrease) in interest rates, equity market prices and foreign currency exchange rates. The

Company believes that a 10% change (increase or decrease) in these market rates and prices is reasonably possible in the near-term. In

performing the analysis summarized below, the Company used market rates at December 31, 2009. The sensitivity analysis separately

calculates each of the Company’s market risk exposures (interest rate, equity price and foreign currency exchange rate) relating to its trading

and non trading assets and liabilities. The Company modeled the impact of changes in market rates and prices on the estimated fair values of

its market sensitive assets and liabilities as follows:

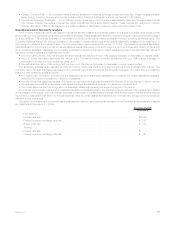

• the net present values of its interest rate sensitive exposures resulting from a 10% change (increase or decrease) in interest rates;

• the U.S. Dollar equivalent estimated fair values of the Company’s foreign currency exposures due to a 10% change (increase or

decrease) in foreign currency exchange rates; and

• the estimated fair value of its equity positions due to a 10% change (increase or decrease) in equity market prices.

The sensitivity analysis is an estimate and should not be viewed as predictive of the Company’s future financial performance. The

Company cannot ensure that its actual losses in any particular period will not exceed the amounts indicated in the table below. Limitations

related to this sensitivity analysis include:

• the market risk information is limited by the assumptions and parameters established in creating the related sensitivity analysis,

including the impact of prepayment rates on mortgages;

• the derivatives that qualify as hedges, the impact on reported earnings may be materially different from the change in market values;

• the analysis excludes other significant real estate holdings and liabilities pursuant to insurance contracts; and

• the model assumes that the composition of assets and liabilities remains unchanged throughout the period.

Accordingly, the Company uses such models as tools and not as substitutes for the experience and judgment of its management. Based

on its analysis of the impact of a 10% change (increase or decrease) in market rates and prices, MetLife has determined that such a change

could have a material adverse effect on the estimated fair value of certain assets and liabilities from interest rate, foreign currency exchange

rate and equity exposures.

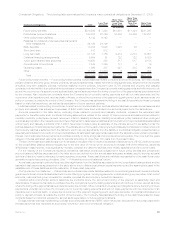

The table below illustrates the potential loss in estimated fair value for each market risk exposure of the Company’s market sensitive assets

and liabilities at December 31, 2009:

December 31, 2009

(In millions)

Non-trading:

Interestraterisk ........................................................ $4,050

Foreigncurrencyexchangeraterisk ........................................... $ 798

Equitypricerisk ........................................................ $ 218

Trading:

Interestraterisk ........................................................ $ 7

Foreigncurrencyexchangeraterisk ........................................... $ 93

71MetLife, Inc.