MetLife 2009 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

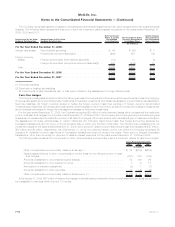

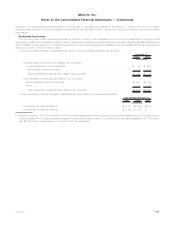

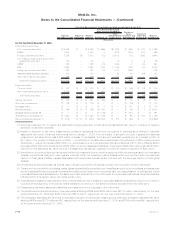

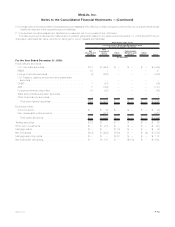

equity securities, mortgage loans, derivatives, hedge funds, other limited partnership interests, short-term investments and cash and cash

equivalents. The estimated fair value of mutual funds is based upon quoted prices or reported NAVs provided by the fund manager.

Accounting guidance effective for December 31, 2009 clarified how investments that use NAV as a practical expedient for their fair value

measurement are classified in the fair value hierarchy. As a result, the Company has included certain mutual funds in the amount of

$96.2 billion in Level 2 of the fair value hierarchy which were previously included in Level 1. The estimated fair values of fixed maturity

securities, equity securities, derivatives, short-term investments and cash and cash equivalents held by separate accounts are determined

on a basis consistent with the methodologies described herein for similar financial instruments held within the general account. The estimated

fair value of hedge funds is based upon NAVs provided by the fund manager. The estimated fair value of mortgage loans is determined by

discounting expected future cash flows, using current interest rates for similar loans with similar credit risk. Other limited partnership interests

are valued giving consideration to the value of the underlying holdings of the partnerships and by applying a premium or discount, if

appropriate, for factors such as liquidity, bid/ask spreads, the performance record of the fund manager or other relevant variables which may

impact the exit value of the particular partnership interest.

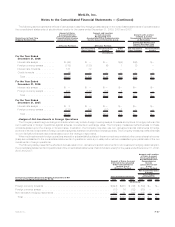

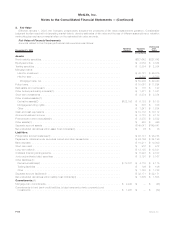

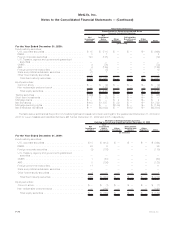

Policyholder Account Balances — Policyholder account balances in the table above include investment contracts. Embedded derivatives

on investment contracts and certain variable annuity guarantees accounted for as embedded derivatives are included in this caption in the

consolidated financial statements but excluded from this caption in the tables above as they are separately presented therein. The remaining

difference between the amounts reflected as policyholder account balances in the preceding table and those recognized in the consolidated

balance sheets represents those amounts due under contracts that satisfy the definition of insurance contracts and are not considered

financial instruments.

The investment contracts primarily include certain funding agreements, fixed deferred annuities, modified guaranteed annuities, fixed

term payout annuities and total control accounts. The fair values for these investment contracts are estimated by discounting best estimate

future cash flows using current market risk-free interest rates and adding a spread for the Company’s own credit which is determined using

publicly available information relating to the Company’s debt, as well as its claims paying ability.

Bank Deposits — Due to frequency of interest rate resets on customer bank deposits held in money market accounts, the Company

believes that there is minimal risk of a material change in interest rates such that the estimated fair value approximates carrying value. For time

deposits, estimated fair values are estimated by discounting the expected cash flows to maturity using a discount rate based on an average

market rate for certificates of deposit being offered by a representative group of large financial institutions at the date of the valuation.

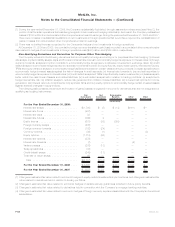

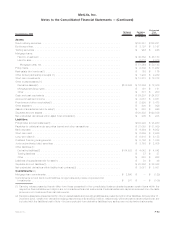

Short-term and Long-term Debt, Collateral Financing Arrangements and Junior Subordinated Debt Securities — The estimated fair value

for short-term debt approximates carrying value due to the short-term nature of these obligations. The estimated fair values of long-term debt,

collateral financing arrangements and junior subordinated debt securities are generally determined by discounting expected future cash

flows using market rates currently available for debt with similar remaining maturities and reflecting the credit risk of the Company including

inputs, when available, from actively traded debt of the Company or other companies with similar types of borrowing arrangements. Risk-

adjusted discount rates applied to the expected future cash flows can vary significantly based upon the specific terms of each individual

arrangement, including, but not limited to: subordinated rights; contractual interest rates in relation to current market rates; the structuring of

the arrangement; and the nature and observability of the applicable valuation inputs. Use of different risk-adjusted discount rates could result

in different estimated fair values.

The carrying value of long-term debt presented in the table above differs from the amounts presented in the consolidated balance sheets

as it does not include capital leases which are not required to be disclosed at estimated fair value.

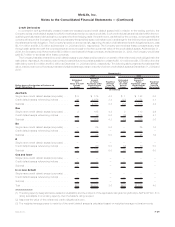

Payables for Collateral Under Securities Loaned and Other Transactions — The estimated fair value for payables for collateral under

securities loaned and other transactions approximates carrying value. The related agreements to loan securities are short-term in nature such

that the Company believes there is limited risk of a material change in market interest rates. Additionally, because borrowers are cross-

collateralized by the borrowed securities, the Company believes no additional consideration for changes in its own credit are necessary.

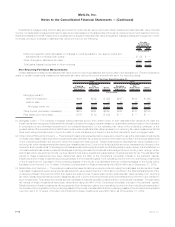

Other Liabilities — Other liabilities in the consolidated balance sheets are principally comprised of freestanding derivatives with negative

estimated fair values; securities trading liabilities; tax and litigation contingency liabilities; obligations for employee-related benefits; interest

due on the Company’s debt obligations and on cash collateral held in relation to securities lending; dividends payable; amounts due for

securities purchased but not yet settled; amounts due under assumed reinsurance contracts; and general operating accruals and payables.

The estimated fair value of derivatives — with positive and negative estimated fair values — and embedded derivatives within asset and

liability host contracts are described in the sections labeled “Derivatives” and “Embedded Derivatives within Asset and Liability Host

Contracts” which follow.

The remaining other amounts included in the table above reflect those other liabilities that satisfy the definition of financial instruments

subject to disclosure. These items consist primarily of securities trading liabilities; interest and dividends payable; amounts due for securities

purchased but not yet settled; and amounts payable under certain assumed reinsurance contracts recognized using the deposit method of

accounting. The Company evaluates the specific terms, facts and circumstances of each instrument to determine the appropriate estimated

fair values, which were not materially different from the recognized carrying values.

Separate Account Liabilities — Separate account liabilities included in the table above represent those balances due to policyholders

under contracts that are classified as investment contracts. The difference between the separate account liabilities reflected above and the

amounts presented in the consolidated balance sheets represents those contracts classified as insurance contracts which do not satisfy the

criteria of financial instruments for which fair value is to be disclosed.

Separate account liabilities classified as investment contracts primarily represent variable annuities with no significant mortality risk to the

Company such that the death benefit is equal to the account balance; funding agreements related to group life contracts; and certain

contracts that provide for benefit funding.

Separate account liabilities, whether related to investment or insurance contracts, are recognized in the consolidated balance sheets at

an equivalent summary total of the separate account assets. Separate account assets, which equal net deposits, net investment income and

F-66 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)