MetLife 2009 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

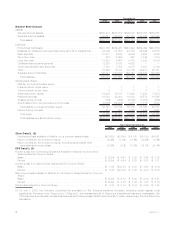

|

|

• Increases in our International segment, as a result of ongoing investments and improvements in the various distribution and service

operations throughout the regions; and

• Modest growth in Insurance products. Our growth continues to be impacted by the current higher levels of unemployment and it is

possible that certain customers may further reduce or eliminate coverages in response to the financial pressures they are

experiencing.

• Offsetting these growth areas, MetLife Bank’s premiums, fees & other revenues are expected to decline from the 2009 level, which

benefited from the large number of mortgage refinancings in that year.

• Higher returns on the investment portfolio

Despite expectations that the real estate market will remain challenging in 2010, higher returns on the investment portfolio are

expected across all segments. We believe returns on alternative investment classes will improve and expect to reinvest cash and

U.S. Treasuries into higher yielding asset classes.

• Improvement in net investment gains (losses)

Although difficult to predict, net investment gains (losses) on our invested asset portfolio are expected to show significant

improvement as the financial markets stabilize across asset classes, returning to a more normalized level from the large losses

encountered in 2009. More difficult to predict is the impact of potential changes in fair value of derivatives instruments as even relatively

small movements in market variables, including interest rates, equity levels and volatility, can have a large impact on derivatives fair

values. Additionally, changes in MetLife’s credit spread, may have a material impact on net investmentgains(losses)asitisrequiredto

be included in the valuation of certain embedded derivatives.

• Reduced volatility in guarantee-related liabilities

Certain annuity and life benefit guarantees are tied to market performance, which when markets are depressed, may require us to

establish additional liabilities, even though these guarantees are significantly hedged. In line with the assumptions discussed above,

we expect a significant reduction in the volatility of these items in 2010 compared to 2009.

• Focus on disciplined underwriting

We do not expect any significant changes to the underlying trends that drive underwriting results and we anticipate solid results in

2010. While we did begin to see the negative impact of the economy on non-medical health experience in 2009, we expect to see

improvement in our results in 2010 as the economy continues to improve. Pricing actions taken in 2009 in our dental business will help

mitigate the impact of elevated claim utilization, experienced as a result of the challenging economic conditions and higher

unemployment.

• Focus on expense management

Our continued focus on expense control throughout the Company, as well the continuing impact of specific initiatives such as

Operational Excellence (our enterprise-wide cost reduction and revenue enhancement initiative), should contribute to increased

profitability. With continued improvement in the financial markets, we also expect that the Company’s pension-related expenses will

return to a more normal level in 2010.

Industry Trends

The Company’s segments continue to be influenced by a continuing unstable financial and economic environment that affects the

industry.

Financial and Economic Environment. Our results of operations are materially affected by conditions in the global capital markets and the

economy, generally, both in the United States and elsewhere around the world. The global economy and markets are now recovering from a

period of significant stress that began in the second half of 2007 and substantially increased through the first quarter of 2009. This disruption

adversely affected the financial services industry, in particular. The U.S. economy entered a recession in January 2008 and most economists

believe this recession ended in the third quarter of 2009 when positive growth returned. Most economists now expect positive growth to

continue through 2010.

Throughout 2008 and continuing in 2009, Congress, the Federal Reserve Bank of New York, the U.S. Treasury and other agencies of the

Federal government took a number of increasingly aggressive actions (in addition to continuing a series of interest rate reductions that began

in the second half of 2007) intended to provide liquidity to financial institutions and markets, to avert a loss of investor confidence in particular

troubled institutions, to prevent or contain the spread of the financial crisis and to spur economic growth. How and to whom these

governmental institutions distribute amounts available under the governmental programs could have the effect of supporting some aspects of

the financial services industry more than others or provide advantages to some of our competitors. Governments in many of the foreign

markets in which MetLife operates have also responded to address market imbalances and have taken meaningful steps intended to restore

market confidence. As market conditions have stabilized, some of these programs have been terminated or allowed to expire. We cannot

predict whether or when the U.S. or foreign governments will establish additional governmental programs or terminate or permit other

programs to expire or the impact any additional measures, existing programs or termination or expiration of programs will have on the financial

markets, whether on the levels of volatility currently being experienced, the levels of lending by financial institutions, the prices buyers are

willing to pay for financial assets or otherwise. See “Business — Regulation — Governmental Responses to Extraordinary Market

Conditions.”

The economic crisis and the resulting recession have had and will continue to have an adverse effect on the financial results of companies

in the financial services industry, including MetLife. The declining financial markets and economic conditions have negatively impacted our

investment income, our net investment gains (losses), and the demand for and the cost and profitability of certain of our products, including

variable annuities and guarantee benefits. See “— Results of Operations” and “— Liquidity and Capital Resources.”

Demographics. In the coming decade, a key driver shaping the actions of the life insurance industry will be the rising income protection,

wealth accumulation and needs of the retiring Baby Boomers. As a result of increasing longevity, retirees will need to accumulate sufficient

savings to finance retirements that may span 30 or more years. Helping the Baby Boomers to accumulate assets for retirement and

subsequently to convert these assets into retirement income represents an opportunity for the life insurance industry.

7MetLife, Inc.