MetLife 2009 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

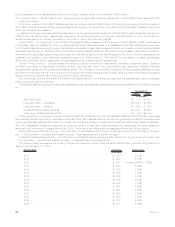

the Australian dollar, the Argentine peso and the Hong Kong dollar. In addition to hedging with foreign currency swaps, forwards and options,

local surplus in some countries, is held entirely or in part in U.S. Dollar assets which further minimizes exposure to foreign currency exchange

rate fluctuation risk. The Company has matched much of its foreign currency liabilities in its foreign subsidiaries with their respective foreign

currency assets, thereby reducing its risk to foreign currency exchange rate fluctuation.

Equity Prices. The Company has exposure to equity prices through certain liabilities that involve long-term guarantees on equity

performance such as net embedded derivatives on variable annuities with guaranteed minimum benefits, certain policyholder account

balances along with investments in equity securities. We manage this risk on an integrated basis with other risks through our asset/liability

management strategies including the dynamic hedging of certain variable annuity guarantee benefits. The Company also manages equity

price risk incurred in its investment portfolio through the use of derivatives. Equity exposures associated with other limited partnership

interests are excluded from this section as they are not considered financial instruments under generally accepted accounting principles.

Management of Market Risk Exposures

The Company uses a variety of strategies to manage interest rate, foreign currency exchange rate and equity price risk, including the use

of derivative instruments.

Interest Rate Risk Management. To manage interest rate risk, the Company analyzes interest rate risk using various models, including

multi-scenario cash flow projection models that forecast cash flows of the liabilities and their supporting investments, including derivative

instruments. These projections involve evaluating the potential gain or loss on most of the Company’s in-force business under various

increasing and decreasing interest rate environments. The New York State Insurance Department regulations require that MetLife perform

some of these analyses annually as part of MetLife’s review of the sufficiency of its regulatory reserves. For several of its legal entities, the

Company maintains segmented operating and surplus asset portfolios for the purpose of asset/liability management and the allocation of

investment income to product lines. For each segment, invested assets greater than or equal to the GAAP liabilities less the DAC asset and

any non-invested assets allocated to the segment are maintained, with any excess swept to the surplus segment. The operating segments

may reflect differences in legal entity, statutory line of business and any product market characteristic which may drive a distinct investment

strategy with respect to duration, liquidity or credit quality of the invested assets. Certain smaller entities make use of unsegmented general

accounts for which the investment strategy reflects the aggregate characteristics of liabilities in those entities. The Company measures

relative sensitivities of the value of its assets and liabilities to changes in key assumptions utilizing Company models. These models reflect

specific product characteristics and include assumptions based on current and anticipated experience regarding lapse, mortality and interest

crediting rates. In addition, these models include asset cash flow projections reflecting interest payments, sinking fund payments, principal

payments, bond calls, mortgage prepayments and defaults.

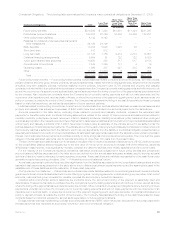

Common industry metrics, such as duration and convexity, are also used to measure the relative sensitivity of assets and liability values to

changes in interest rates. In computing the duration of liabilities, consideration is given to all policyholder guarantees and to how the Company

intends to set indeterminate policy elements such as interest credits or dividends. Each asset portfolio has a duration target based on the

liability duration and the investment objectives of that portfolio. Where a liability cash flow may exceed the maturity of available assets, as is the

case with certain retirement and non-medical health products, the Company may support such liabilities with equity investments, derivatives

or curve mismatch strategies.

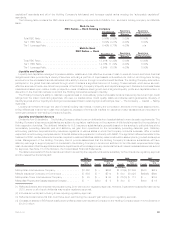

Foreign Currency Exchange Rate Risk Management. Foreign currency exchange rate risk is assumed primarily in three ways: invest-

ments in foreign subsidiaries, purchases of foreign currency denominated investments in the investment portfolio and the sale of certain

insurance products.

• The Company’s Treasury Department is responsible for managing the exposure to investments in foreign subsidiaries. Limits to

exposures are established and monitored by the Treasury Department and managed by the Investment Department.

• The Investment Department is responsible for managing the exposure to foreign currency investments. Exposure limits to unhedged

foreign currency investments are incorporated into the standing authorizations granted to management by the Board of Directors and

are reported to the Board of Directors on a periodic basis.

• The lines of business are responsible for establishing limits and managing any foreign exchange rate exposure caused by the sale or

issuance of insurance products.

MetLife uses foreign currency swaps and forwards to hedge its foreign currency denominated fixed income investments, its equity

exposure in subsidiaries and its foreign currency exposures caused by the sale of insurance products.

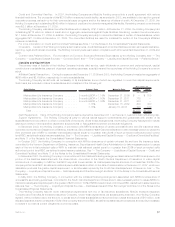

Equity Price Risk Management. Equity price risk incurred through the issuance of variable annuities is managed by the Company’s Asset/

Liability Management Unit in partnership with the Investment Department. Equity price risk is also incurred through its investment in equity

securities and is managed by its Investment Department. MetLife uses derivatives to hedge its equity exposure both in certain liability

guarantees such as variable annuities with guaranteed minimum benefit and equity securities. These derivatives include exchange-traded

equity futures, equity index options contracts and equity variance swaps. The Company’s derivative hedges performed effectively through the

extreme movements in the equity markets during the latter part of 2008. The Company also employs reinsurance to manage these exposures.

Hedging Activities. MetLife uses derivative contracts primarily to hedge a wide range of risks including interest rate risk, foreign currency

risk, and equity risk. Derivative hedges are designed to reduce risk on an economic basis while considering their impact on accounting results

and GAAP and Statutory capital. The construction of the Company’s derivative hedge programs vary depending on the type of risk being

hedged. Some hedge programs are asset or liability specific while others are portfolio hedges that reduce risk related to a group of liabilities or

assets. The Company’s use of derivatives by major hedge programs is as follows:

• Risks Related to Living Guarantee Benefits — The Company uses a wide range of derivative contracts to hedge the risk associated with

variable annuity living guarantee benefits. These hedges include equity and interest rate futures, interest rate swaps, currency futures/

forwards, equity indexed options and interest rate option contracts and equity variance swaps.

• Minimum Interest Rate Guarantees — For certain Company liability contracts, the Company provides the contractholder a guaranteed

minimum interest rate. These contracts include certain fixed annuities and other insurance liabilities. The Company purchases interest

rate floors to reduce risk associated with these liability guarantees.

• Reinvestment Risk in Long Duration Liability Contracts — Derivatives are used to hedge interest rate risk related to certain long duration

liability contracts, such as long-term care. Hedges include zero coupon interest rate swaps and swaptions.

70 MetLife, Inc.