MetLife 2009 Annual Report Download - page 195

Download and view the complete annual report

Please find page 195 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

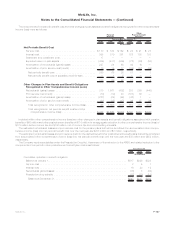

|

|

by the plan fiduciary. These Managers have portfolio management discretion over the purchasing and selling of securities and other

investment assets pursuant to the respective investment management agreements and guidelines established for each insurance separate

account. The assets of the qualified pension plans and postretirement medical plans (the “Invested Plans”) are well diversified across multiple

asset categories and across a number of different Managers, with the intent of minimizing risk concentrations within any given asset category

or with any given Manager.

The Invested Plans, other than those held in participant directed investment accounts, are managed in accordance with investment

policies consistent with the longer-term nature of related benefit obligations and within prudent risk parameters. Specifically, investment

policies are oriented toward (i) maximizing the Invested Plan’s funded status; (ii) minimizing the volatility of the Invested Plan’s funded status;

(iii) generating asset returns that exceed liability increases; and (iv) targeting rates of return in excess of a custom benchmark and industry

standards over appropriate reference time periods. These goals are expected to be met through identifying appropriate and diversified asset

classes and allocations, ensuring adequate liquidity to pay benefits and expenses when due and controlling the costs of administering and

managing the Invested Plan’s investments. Independent investment consultants are periodically used to evaluate the investment risk of

Invested Plan’s assets relative to liabilities, analyze the economic and portfolio impact of various asset allocations and management

strategies and to recommend asset allocations.

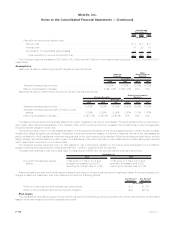

Certain international subsidiaries sponsor defined benefit plans that cover employees and sales representatives who meet specified

eligibility requirements. Pension benefits are provided utilizing either a traditional formula or cash balance formula, similar to the U.S. plans

discussed above. The investment objectives are also similar, subject to local regulations. Generally, these international pension plans invest

directly in high quality equity and fixed maturity securities.

Derivative contracts may be used to reduce investment risk, to manage duration and to replicate the risk/return profile of an asset or asset

class. Derivatives may not be used to leverage a portfolio in any manner, such as to magnify exposure to an asset, asset class, interest rates

or any other financial variable. Derivatives are also prohibited for use in creating exposures to securities, currencies, indices or any other

financial variable that are otherwise restricted.

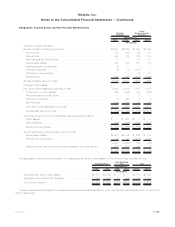

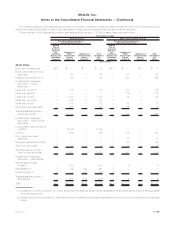

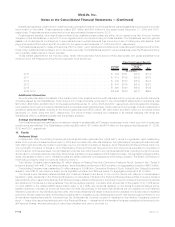

The following tables summarize the actual weighted average asset allocation by major asset class for the Invested Plans.

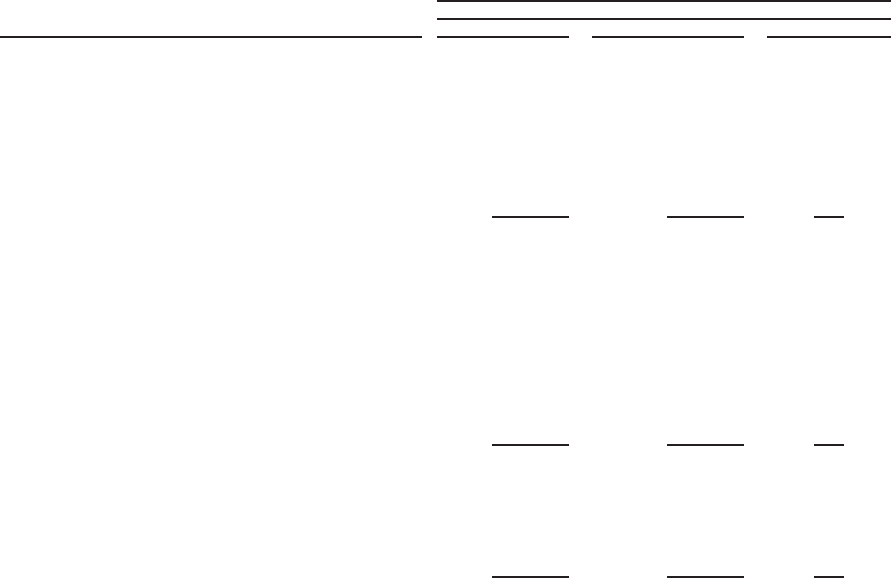

Asset Class Defined Benefit Plan Postretirement Medical Postretirement Life

December 31, 2009

Actual Asset Allocation

Equity (target range): 25% to 45% 50% to 80% —

Largecapgrowth ........................ 2% 10% —

Largecapvalue ......................... — 26 —

Largecapcore.......................... 23 4 —

Smallcapgrowth ........................ 3 — —

Smallcapcore.......................... 2 11 —

Developedinternational .................... 7 11 —

Totalequity........................... 37% 62% —

Fixed income (target range): 35% to 55% 10% to 40% —

Longduration(governmentandcredit)........... 37% —% —

Core................................. 6 18 —

U.S.governmentandagencies ............... — 3 —

Mortgage-backedsecurities ................. — 4 —

Directlyheldbonds ....................... 1 9 —

Insurancegeneralaccount .................. 2 — 100%

Short-termandcash ...................... 1 3 —

Totalfixedincome....................... 47% 37% 100%

Alternatives (target range): 10% to 25% 0% to 15% —

Multi-strategyhedgefunds .................. 4% 1% —

Realestate ............................ 5 — —

Privateequity........................... 7 — —

Totalalternatives ....................... 16% 1% —

Totalinvestments.......................... 100% 100% 100%

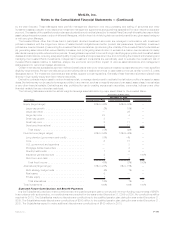

Expected Future Contributions and Benefit Payments

It is the Subsidiaries’ practice to make contributions to the qualified pension plan to comply with minimum funding requirements of ERISA.

In accordance with such practice, no contributions were required for the years ended December 31, 2009 or 2008. No contributions will be

required for 2010. The Subsidiaries made no discretionary contributions to the qualified pension plan during the year ended December 31,

2009. The Subsidiaries made discretionary contributions of $300 million to the qualified pension plan during the year ended December 31,

2008. The Subsidiaries expect to make additional discretionary contributions of $150 million in 2010.

F-111MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)