MetLife 2009 Annual Report Download - page 190

Download and view the complete annual report

Please find page 190 of the 2009 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

|

|

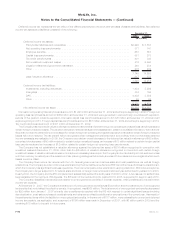

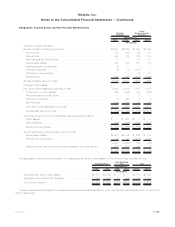

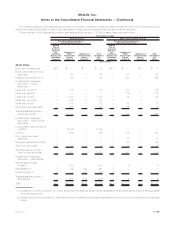

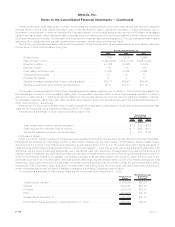

The aggregate pension accumulated benefit obligation and aggregate fair value of plan assets for pension plans with accumulated benefit

obligationsinexcessofplanassetsisasfollows:

2009 2008

December 31,

(In millions)

Projectedbenefitobligation................................................... $798 $708

Accumulatedbenefitobligation................................................. $714 $590

Fairvalueofplanassets..................................................... $ 1 $ —

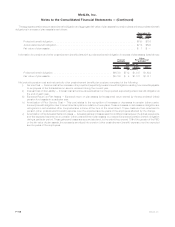

Information for pension and other postretirement benefit plans with a projected benefit obligation in excess of plan assets is as follows:

2009 2008 2009 2008

December 31,

Pension

Benefits

Other

Postretirement

Benefits

(In millions)

Projectedbenefitobligation .................................... $6,580 $712 $1,847 $1,632

Fairvalueofplanassets ...................................... $5,700 $ 4 $1,121 $1,011

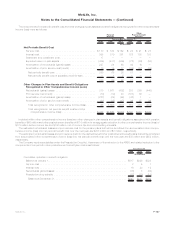

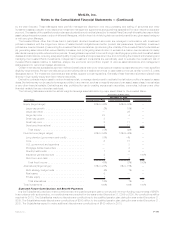

Net periodic pension cost and net periodic other postretirement benefit plan cost are comprised of the following:

i) Service Cost — Service cost is the increase in the projected (expected) pension benefit obligation resulting from benefits payable

to employees of the Subsidiaries on service rendered during the current year.

ii) Interest Cost on the Liability — Interest cost is the time value adjustment on the projected (expected) pension benefit obligation at

the end of each year.

iii) Expected Return on Plan Assets — Expected return on plan assets is the assumed return earned by the accumulated (other)

pension fund assets in a particular year.

iv) Amortization of Prior Service Cost — This cost relates to the recognition of increases or decreases in pension (other postre-

tirement) benefit obligation due to amendments in plans or initiation of new plans. These increases or decreases in obligation are

recognized in accumulated other comprehensive income at the time of the amendment. These costs are then amortized to

pension (other postretirement benefit) expense over the expected service years of the employees affected by the change.

v) Amortization of Net Actuarial Gains or Losses — Actuarial gains and losses result from differences between the actual experience

and the expected experience on pension (other postretirement) plan assets or projected (expected) pension benefit obligation

during a particular period. These gains and losses are accumulated and, to the extent they exceed 10% of the greater of the PBO

or the fair value of plan assets, the excess is amortized into pension (other postretirement benefit) expense over the expected

service years of the employees.

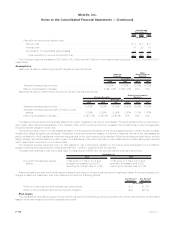

F-106 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)