Wells Fargo 2009 Annual Report Download - page 180

Download and view the complete annual report

Please find page 180 of the 2009 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

-

192

-

193

-

194

-

195

-

196

|

|

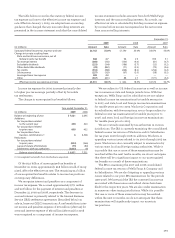

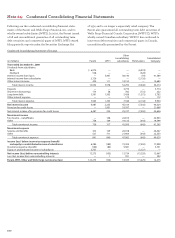

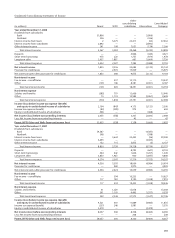

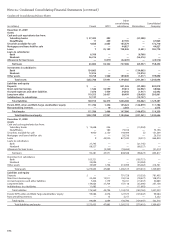

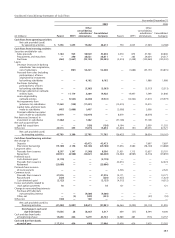

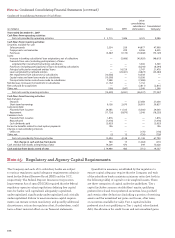

Note 23: Operating Segments

As a result of the combination of Wells Fargo and Wachovia,

in first quarter 2009, management realigned its segments

into the following three lines of business for management

reporting: Community Banking; Wholesale Banking; and

Wealth, Brokerage and Retirement. The results for these

lines of business are based on our management accounting

process, which assigns balance sheet and income statement

items to each responsible operating segment. This process is

dynamic and, unlike financial accounting, there is no compre-

hensive, authoritative guidance for management accounting

equivalent to GAAP. The management accounting process

measures the performance of the operating segments based

on our management structure and is not necessarily compara-

ble with similar information for other financial services

companies. We define our operating segments by product

type and customer segment. If the management structure

and/or the allocation process changes, allocations, transfers

and assignments may change. We revised prior period

information to reflect the first quarter 2009 realignment of

our operating segments; however, because the acquisition

was completed on December 31, 2008, Wachovia’s results are

not included in the income statement or in average balances

for periods prior to 2009.

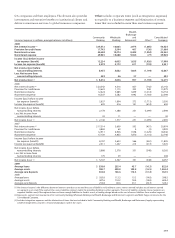

Community Banking offers a complete line of diversified

financial products and services to consumers and small

businesses with annual sales generally up to $20 million

in which the owner generally is the financial decision maker.

Community Banking also offers investment management and

other services to retail customers and securities brokerage

through affiliates. These products and services include the

Wells Fargo Advantage FundsSM, a family of mutual funds.

Loan products include lines of credit, equity lines and loans,

equipment and transportation (recreational vehicle and

marine) loans, education loans, origination and purchase

of residential mortgage loans and servicing of mortgage

loans and credit cards. Other credit products and financial

services available to small businesses and their owners

include receivables and inventory financing, equipment

leases, real estate financing, Small Business Administration

financing, venture capital financing, cash management,

payroll services, retirement plans, Health Savings Accounts

and merchant payment processing. Consumer and business

deposit products include checking accounts, savings deposits,

market rate accounts, Individual Retirement Accounts,

time deposits and debit cards.

Community Banking serves customers through a

complete range of channels, including traditional banking

stores, in-store banking centers, business centers, ATMs,

and Wells Fargo Customer Connection, a 24-hours a day,

seven days a week telephone service. Online banking

services include single sign-on to online banking, bill pay

and brokerage, as well as online banking for small business.

Community Banking also includes Wells Fargo Financial

consumer finance and auto finance operations. Consumer

finance operations make real estate loans to individuals in

the United States and the Pacific Rim, and also make direct

consumer loans to individuals and purchase sales finance

contracts from retail merchants from offices throughout

the United States, and in Canada and the Pacific Rim. Auto

finance operations specialize in purchasing sales finance

contracts directly from auto dealers in Puerto Rico and mak-

ing loans secured by autos in the United States and Puerto

Rico. Wells Fargo Financial also provides credit cards, lease

and other commercial financing.

Wholesale Banking provides financial solutions to businesses

across the United States with annual sales generally in excess

of $10 million and to financial institutions globally. Wholesale

Banking provides a complete line of commercial, corporate,

capital markets, cash management and real estate banking

products and services. These include traditional commercial

loans and lines of credit, letters of credit, asset-based lending,

equipment leasing, mezzanine financing, high-yield debt,

international trade facilities, trade financing, collection

services, foreign exchange services, treasury management,

investment management, institutional fixed-income sales,

interest rate, commodity and equity risk management,

online/electronic products such as the Commercial Electronic

Office® (CEO®) portal, insurance, corporate trust fiduciary

and agency services, and investment banking services.

Wholesale Banking also supports the CRE market with prod-

ucts and services such as construction loans for commercial

and residential development, land acquisition and development

loans, secured and unsecured lines of credit, interim financing

arrangements for completed structures, rehabilitation loans,

affordable housing loans and letters of credit, permanent

loans for securitization, CRE loan servicing and real estate

and mortgage brokerage services.

Wealth, Brokerage and Retirement provides a full range of

financial advisory, lending, fiduciary, and investment manage-

ment services to clients using a comprehensive planning

approach to meet each client’s needs. Wealth Management

uses an integrated model to provide affluent and high-net-

worth customers with a complete range of wealth management

solutions and services. Family Wealth meets the unique

needs of ultra-high-net-worth customers managing multi-

generational assets—those with at least $50 million in assets.

Retail Brokerage’s financial advisors serve customers’ advisory,

brokerage and financial needs, including investment manage-

ment, portfolio monitoring and estate planning as part of

one of the largest full-service brokerage firms in the United

States. They also offer access to banking products, insurance,

and investment banking services. First Clearing LLC, our

correspondent clearing firm, provides technology, product

and other business support to broker-dealers across the

United States. Retirement supports individual investors’

retirement needs and is a leader in 401(k) and pension record

keeping, investment services, trust and custody solutions for