Wells Fargo 2009 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2009 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

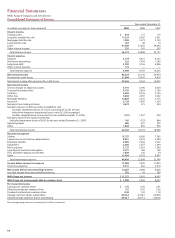

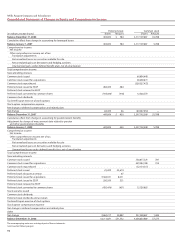

Note 1: Summary of Significant Accounting Policies (continued)

FASB ASC 825-10 (FSP FAS 107-1 and APB 28-1) states that

entities must disclose the fair value of financial instruments

in interim reporting periods as well as in annual financial

statements. Entities must also disclose the methods and

assumptions used to estimate fair value as well as any changes

in methods and assumptions that occurred during the reporting

period. We adopted this pronouncement in second quarter

2009. See Note 16 in this Report for additional information.

Because the new provisions in FASB ASC 825-10 amend only

the disclosure requirements related to the fair value of finan-

cial instruments, our adoption of this pronouncement did not

affect our consolidated financial statements.

ASU 2009-12 provides guidance for determining the fair

value of certain alternative investments, which include hedge

funds, private equity funds, and real estate funds. When

alternative investments do not have readily determinable fair

values, companies are permitted to use unadjusted net asset

values or an equivalent measure to estimate fair value. This

provision is only allowable for investments in entities that

calculate net asset value (NAV) per share or its equivalent in

accordance with accounting guidance for investment companies.

This Update also requires a company to consider its ability

to redeem an investment at NAV when determining the

appropriate classification of the related fair value measurement

within the fair value hierarchy. ASU 2009-12 was effective for

us in fourth quarter 2009 with prospective application. Our

adoption of this new guidance did not have a material impact

on our consolidated financial statements. See Note 16 in this

Report for disclosures related to certain alternative investments.

ASU 2009-5 describes the valuation techniques companies

should use to measure the fair value of liabilities for which

there is limited observable market data. If a quoted price in

an active market is not available for an identical liability, an

entity should use one of the following approaches: (1) the

quoted price of the identical liability when traded as an asset,

(2) quoted prices for similar liabilities or similar liabilities

when traded as an asset, or (3) another valuation technique

that is consistent with the principles of FASB ASC 820, Fair

Value Measurements and Disclosures. When measuring the

fair value of liabilities, this Update reiterates that companies

should apply valuation techniques that maximize the use of

relevant observable inputs, which is consistent with existing

accounting provisions for fair value measurement. In addi-

tion, this Update clarifies when an entity should adjust quoted

prices of identical or similar assets that are used to estimate

the fair value of liabilities. For example, an entity should not

include separate adjustments for contractual restrictions that

prevent the transfer of the liability because the restriction

would be factored into other inputs used in the fair value

measurement of the liability. However, separate adjustments

are needed in situations where the unit of account for the

asset is not the same as for the liability. This guidance was

effective for us in fourth quarter 2009 with adoption applied

prospectively. Our adoption of this standard did not have a

material impact on our consolidated financial statements.

FASB ASC 715-20 (FSP FAS 132 (R)-1) requires new disclo-

sures that are applicable to the plan assets of our Cash

Balance Plan and other postretirement benefit plans. The

objectives of the new disclosures are to provide an under-

standing of how investment allocation decisions are made,

the major categories of plan assets, the inputs and valuation

techniques used to measure fair value, the effect of fair value

measurements using significant unobservable inputs on the

changes in plan assets and significant concentrations of risk

within plan assets. We adopted this pronouncement prospec-

tively for year-end 2009 reporting. The guidance does not

affect the results of our consolidated financial statements

since it only amends the disclosure requirements for postre-

tirement benefits.

Consolidation

Our consolidated financial statements include the accounts of

the Parent and our majority-owned subsidiaries and variable

interest entities (VIEs) (defined below) in which we are the

primary beneficiary. Significant intercompany accounts and

transactions are eliminated in consolidation. If we own at

least 20% of an entity, we generally account for the investment

using the equity method. If we own less than 20% of an entity,

we generally carry the investment at cost, except marketable

equity securities, which we carry at fair value with changes in

fair value included in OCI. Investments accounted for under

the equity or cost method are included in other assets.

We are a variable interest holder in certain special-

purpose entities (SPEs) in which equity investors do not have

the characteristics of a controlling financial interest or where

the entity does not have enough equity at risk to finance its

activities without additional subordinated financial support

from other parties (referred to as VIEs). Our variable interest

arises from contractual, ownership or other monetary interests

in the entity, which change with fluctuations in the entity’s

NAV. We consolidate a VIE if we are the primary beneficiary,

defined as the entity that will absorb a majority of the entity’s

expected losses, receive a majority of the entity’s expected

residual returns, or both.

Trading Assets

Trading assets are primarily securities, including corporate

debt, U.S. government agency obligations and other securities

that we acquire for short-term appreciation or other trading

purposes, and the fair value of derivatives held for customer

accommodation purposes or proprietary trading. Interest-only

strips and other retained interests in securitizations that can

be contractually prepaid or otherwise settled in a way that the

holder would not recover substantially all of its recorded

investment are classified as trading assets. Trading assets are

carried at fair value, with realized and unrealized gains and

losses recorded in noninterest income.